Conclusion: We’ve had HBI as one of our key short ideas, and after this call we like it even more. This was the weirdest print/call we’ve heard since YHOO’s Carol Bartz let loose on the investor community in ’09. HBI is shaking out to be a decelerating top line growth model with financial and operational leverage that is about to lap acquisitions, channel restocking, pricing, and now is showing signs of erosion in unit growth in the core business. Next year’s numbers hinge on continued success with pricing at a time when Wal-Mart just unexpectedly cut a major program (Just My Size) in favor of private label, which cost HBI 7 points of growth out of its core. The Street has valued HBI at egregious levels given its ‘pseudo’ growth profile over the past two years. But in the end, this quarter should give better visibility as to what the company actually is; a good, but slow and volatile grower on a heavy operating asset base with too much debt. There’s no reason why companies like GES should trade at less than 8x earnings and 5x EBITDA with HBI going out today at 10x and 8x, respectively. Even at the after-hours price of $25, it’s still 9x and 7.8x.

We’ve had HBI as one of our top three shorts for the past six months, and expected 3Q to be a bad event (see our 10/24 note “We Don’t Like It”), but what we did not expect is for the conference call to be an all out gong-show. It was simply a mess.

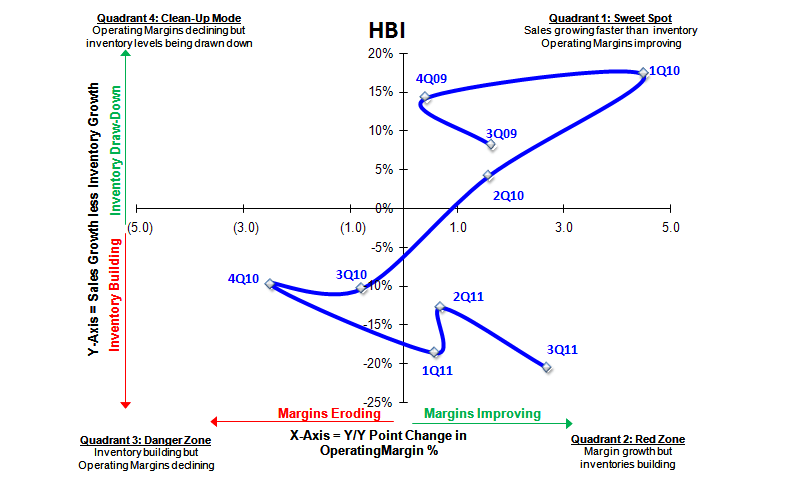

- First off, lets give credit where it’s due. HBI beat the quarter. They missed revenue, but completely made up for it on the gross margin line. Keep in mind that $2/lb+ cotton costs start to hit HBI in 4Q, but they’ve already taken several price increases this year. It’s been in that special place where the customer pays you without HBI having to pass it through to the back-end of its supply chain. In other words, if there was ever a quarter for HBI to crush margins, this was it. In fairness, they did. +360bps vs. last year. Congratulations.

- Organically, sales were down -2%.

- Sales missed in the quarter by ~10%, and HBI guided down the top line (and EPS) in 4Q due to weak unit demand ‘across all channels of distribution.’ Let me get this straight…

- Down in ‘all channels’ means that the channel, in aggregate, is now fully restocked. Retailers might be telling Hanes salespeople that they are simply ‘managing inventories’ but they’re probably not going to say “I loaded up six months ago before price increases went into effect.”

- If we’re right in that regard, it also suggests that the pricing discussion in 2012 is certainly not a slam dunk by any means.

- Management said that there is minimal elasticity in demand for Hanesbrands product, yet prices went up and demand went down. Huh? They noted that this is not due to elasticity, but rather inaccurate forecasting at the beginning of the year. So if we give them credit on the elasticity issue (which I won’t) then I argue that at least we need to ding the company’s forecast accuracy.

- Management noted that cotton costs are the worst in 4Q through 2Q12 – which is true. But that they’ll benefit in 2H. “The retailers want inflation next year.” Yeah…The retailers want the kind of inflation that the consumer genuinely wants to step up and pay for. Not the kind that is forced by higher costs in the supply chain. If costs ease in 2H, which they probably will, how can we have any degree of confidence that HBI will actually be able to keep that savings and flow it through as higher margins?

- How does this sound? HBI is shaking out to be a decelerating top line growth model with financial and operational leverage that is about to lap acquisitions, channel restocking, pricing, and now is showing signs of erosion in unit growth in the core business. Next year’s numbers hinge on continued success with pricing at a time when Wal-Mart just cut a major program ‘Just My Size’ in favor of private label…How does that setup sound?

- The fact that Rich Knoll ‘lost it’ in the conference call because people were not giving him and his team credit for putting up solid Gross Margins and focusing too much on elasticity and unit demand did not help one iota. If that’s how he acts when challenged on a conference call, you gotta wonder what it’s like working inside the company as one of his lieutenants.

- This might be petty but it was a bit odd when he quoted JP Morgan’s Jamie Dimon as validation that the operating environment is tough and business should be managed appropriately.

Here are our key modeling assumptions:

Revenues: We’re shaking out at +4% growth in Q4 resulting in revenues just below the lower end of the company’s guidance of $1.2-$1.3Bn with growth of +3.6% and +4.2% in F12 and F13 respectively.

Innerwear: We don’t expect weak unit demand from its department store partners that bought inventory ahead in the 1H to change near-term. In addition, while the company is getting price increases in this segment of roughly 5-8% in aggregate, units remain down just as intimates is experiencing considerable weakness resulting in anemic growth. We expect a slight sequential acceleration as September price increases take hold in addition to modest shelf space gains. While the company suggests that it’s “working with retailers to formulate a plan” as it relates to inventories and pricing, we expect a modest 1% benefit from pricing in 2012 with another 2-3% from space gains.

Outerwear: In looking at Q3 results, which were impacted by a 7point hit from WMT cutting back its Just My Size program while benefitting from a ~20% boost from incremental Gear For Sports revs, core Outerwear was actually down MSD-HSD. With GFS adding another ~6% to top-line in Q4, we are modeling no growth in core outerwear sales. In F12, Q1 will be toughest compare against the first round of pricing driving core sales up 18% in the prior year. The following three quarters we expect modest LSD-MSD growth driven primarily by GFS coupled with modest core growth resulting in a +1.5% increase in F12 revenues.

Hosiery: This segment contracts at a HSD rate perennially. We see no reason for that to change in this environment. Coming off -5% growth in F11, we expect -10% in F12.

International: HBI’s international sales base is similar in size across Canada, Europe, Mexico, Brazil and Japan with China and India much smaller. In Q3, Canada and Europe weakened slowing high double-digit growth in its other markets. With this segment about to face tough compares for the next three quarters, we expect sales to continue to decelerate in Q4 and shake out at +11% in F12.

DTC: Representing less than 10% of total sales, this segment has grown at a LSD rate over the last few years. It should be growing at a rate closer to MSD, which is where we have it next year at +4%.

Gross Margins: The highest cost cotton is about to flow through the P&L for the next three quarters at the same time other commodity costs (primarily oil) have increased as well, which will quickly reverse the benefit HBI realized in Q3. With a continued supply chain benefit of ~90bps and additional albeit more modest pricing to contribute ~700bps partially offset by higher priced cotton (-460bps) and other commodity costs (-300bps), we expect gross margins to be up slightly in Q4 before turning sharply lower in the 1H and continuing through to Q3 before improving in Q4.

SG&A: Incremental GFS costs will be a modest $5mm in Q4. In addition, we expect a slight reduction of core expenses to be offset by international investments of $8-$10mm per quarter resulting in continued expense leverage on SG&A growth of 3% in Q4 and +3% in F12.

EPS: This equates to earnings of $0.45 in Q4; $2.73 in F12 and $3.07 in 13 reflecting earnings growth of +40%, +0%, and +12% in F11, F12, and F13 respectively.