Here are some considerations headed into sales day tomorrow…

Let’s review the setup from a Macro level:

- While consumer confidence now starts with a 3-handle amongst a myriad of other reasons for concern from a Macro perspective, the consumer still appears willing to spend due in part to a notable drawdown in the collective savings rate to 3.6% in September from 4.5% in August. (positive near-term, negative long-term)

- Gross Personal Income compares are tough this month – as we’re going up against +4.0% compared to a previous run rate of about +3.3%. (negative point)

- The two main levers that account for the delta between Gross Income and Personal Consumption have offset each other for the most part.

- The consolidated personal tax rate is now at 10.9% vs. 9.5% this time last year. (negative point)

- The personal savings rate is now down to +3.6% compared to +5.4%.

-

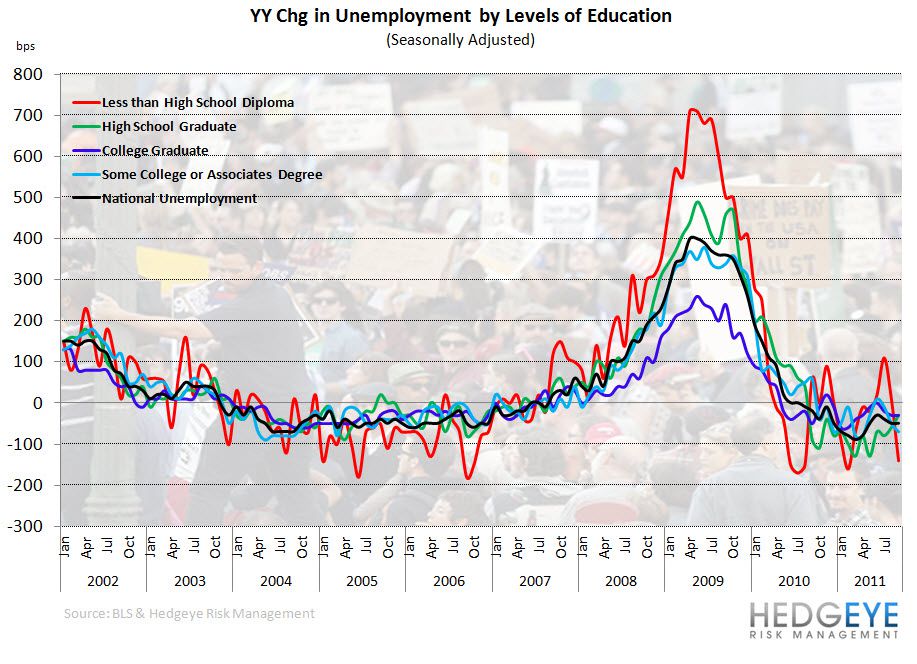

While both the absolute and yy change in unemployment has remained relatively stable at 9.1%, real wage growth has declined at a faster rate over the last two months through September down nearly 2%. (negative point)

-

In looking at ‘Essential Spending’ (food, energy, healthcare), since decelerating to +2.9% in June it has increased every month since to +4.1%. (negative point)

- The balance of spending goes into the ‘Discretionary Spending’ line, which stood at +6.4% this time last year compared to +4.9% in September.

- In addition, consumer confidence is now at 39.8 compared to 49.9 last year.

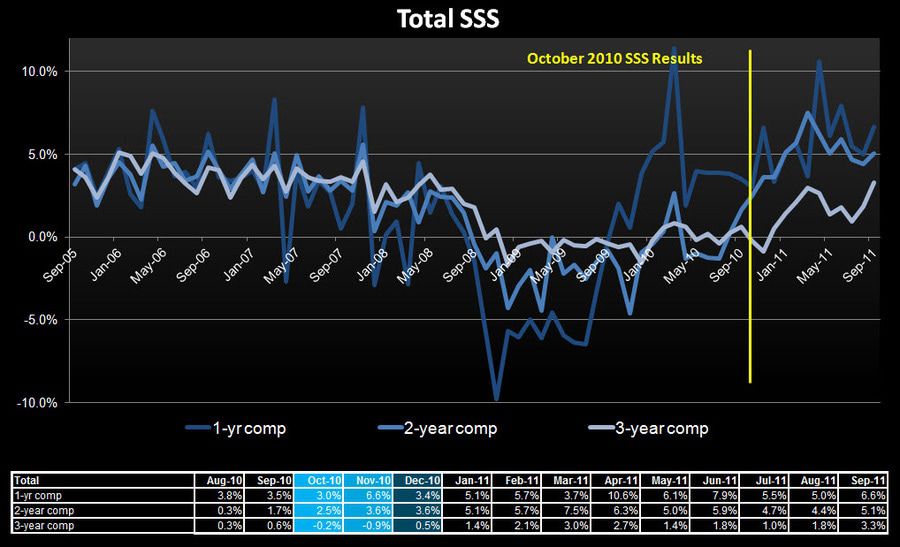

- Based on our read out of POS data (NPD & SportScan), sales in October have increased sequentially from September in the department channel while weekly ICSC retail sales have held steady – one of the few positive deltas in the month. Though hardly representative of retail in aggregate, both athletic footwear and apparel decelerated sequentially as the month progressed.

The bottom-line is that we still think that there will be an increased bifurcation between upward and downward revisions in retail over the next quarter, and throughout 2012. During the month, we saw a few more retailers (CROX and CWTR) pre-announce lower while better positioned companies and retailers at the higher end continue to post strong results. While spending particularly at the higher end continues to remain healthy, the reduction in the personal savings rate remains one of the few levers left for the consumer to pull placing us in an increasingly precarious position heading into the 1H of F12. With prices at low-to-mid tier retailers not sticking, we would avoid exposure to what is becoming an increasingly more competitive battlefront in the domestic mid-tier market.

Casey Flavin

Director