THE HEDGEYE BREAKFAST MENU

Notable MACRO data points, news items, and price action pertaining to the restaurant space.

HEDGEYE ALPHA - RESTAURANTS

With all six companies reporting on the Hedgeye Alpha - Restaurant list we can report a 50-66% success rate depending on how you want to account for EAT. The notable issues we had were on the short-side with bets against PNRA and BWLD. We are going to be making changes to the ALPHA list in the coming days. While we have not finalized the list yet, we still believe in BWLD on the short side despite having been early. Although PNRA has significant challenges from a comparison stand point in 4Q, we’re not sure that is enough to cause a significant revaluation of the company given the momentum shown in the third quarter. The other name on the short side was DNKN and we still hold a negative view of the company from a TRADE, TREND and TAIL stand point. The implication of the announcement of the secondary offering is that Private Equity firms holding the stock are looking to book their gains.

On the long side, I still think MCD and YUM are going to perform ahead of expectations.

MACRO NOTES

For the week ending October 28, 2011, the MBA purchased app index inched up 0.2% driven by an uptick in purchase applications. The purchase index increased 1.8% WoW; still well below year-ago levels. The refinance index slipped 0.2%, but its upward trend is unchanged because of attractive mortgage rates.

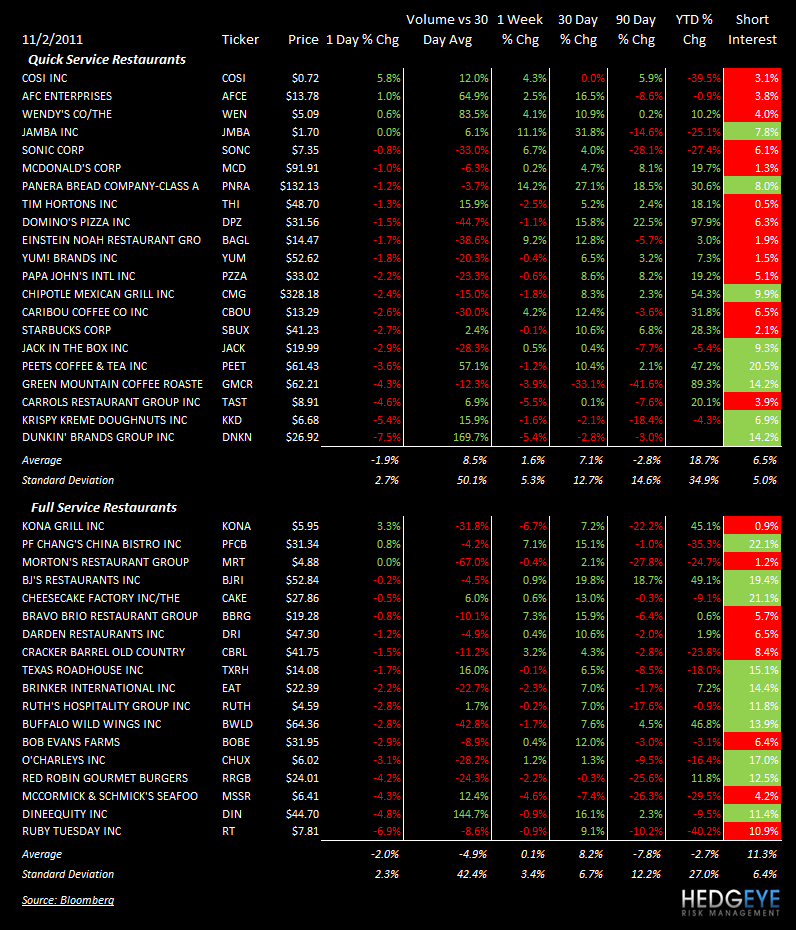

SUB-SECTOR PERFORMANCE

QUICK SERVICE

The coffee sector was down on significant higher volume yesterday

PEET: Peet’s Coffee reported another strong quarter, reporting adjusted EPS of $0.28 versus $0.27 consensus on the back of 14% revenue growth and flat EPS growth which was impacted by coffee costs which were up 53% year-over-year in 3Q versus up 26% year-over-year in 1H11. The company is still on target to meet the higher end of the $1.43-$1.50 guidance range that it reaffirmed.

SBUX: Starbucks is launching K-Cups this week.

DNKN: Dunkin’ Brands dropped Goldman Sachs as an underwriter for its secondary because of a research note GS published today.

FULL SERVICE

TXRH: Texas Roadhous is a name we have thought was a short and this was confirmed by the quarter they reported last night. The company guided to 7% to 9% in food inflation for 2012. The stock was downgraded to Neutral from Outperform at Credit Suisse.

RRGB: Red Robin Gourmet Burgers is the latest casual dining chain to try its hand at a simplified, lower-price, limited-service concept via the crowded gourmet burger business. The company plans to open a fast-casual concept with burgers, beer and wine called Burger Works. We don’t see how this is good for the core business

CBRL: Cracker Barrel is fighting back against Biglari, the activist shareholder in their stock, with gusto. Read the story here.

Howard Penney

Managing Director

Rory Green

Analyst