This note was originally published at 8am on October 28, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“High absolute return is much more recognizable and titillating than superior risk-adjusted performance.”

-Howard Marks (The Most Important Thing, page 57)

I wasn’t short the SP500 until 326PM EST (1290) yesterday. I’d sold all of my long-term Treasuries (TLT) on Wednesday. I wasn’t short anything Commodities and/or European Equities…

So, yesterday could have been worse.

Where I got killed was in my long US Dollar position. The US Dollar Index was down huge (-1.7%), making a fresh low for the month as US stocks completed their biggest 18 day short squeeze ever.

Ever is a long time.

Like my “Short Covering Opportunity” call on October 4th, my “Buy The US Dollar” call on October 21st has a Time Stamp. While there were plenty of risks building a US Financial Services and Media firm in the 2008-2011 period, for me at least, one of them wasn’t showing you every position I take, when I take it.

Time Stamps are cool on Wall St 2.0 because they save you from having to take my word for it.

Back to the Global Macro Grind…

Get the US Dollar right and you’ll get mostly everything else right – if that’s not obvious to someone who is confusing their “high absolute returns” yesterday (everyone nailed it, right?) with what we call beta, I don’t know what is…

Using our immediate-term TRADE duration to measure Correlation Risk, here’s a real-time update on the USD’s inverse correlations:

- SP500 = -0.97

- CRB Commodities Index = -0.88

- 10-year US Treasury Yields = -0.81

No matter where you go this morning, there it is. If you have been bearish on the US Dollar (and bullish on the Euro) for the last 3 weeks, you have absolutely crushed it.

If you’ve been levered-long beta since April’s YTD high in the SP500 of 1363, you’re still getting crushed. Over that time span, the US Dollar Index is up +2.7% and the SP500 is down -5.8%.

But today, all of what you’ve done for 2011 doesn’t matter to the market at all. Mr Macro Market doesn’t care about who is doing the crushing or who is getting crushed. She tends to inflict the most amount of pain on the most amount of players at the same time.

So, what do I do “right here, right now?”

I was asked that yesterday at a lunch meeting in Boston. My answer: “I finish our meeting then go to my next meeting. And if I see my immediate-term TRADE overbought level in the SP500, I’ll short it, for a trade.”

Then client then asked me, “at what price?”

I said, “I don’t know. I need to fire up my machine and remodel my volatility parameters for the draw down in the VIX and melt-up in the SP500’s price. I let my process tell me what to do, not my emotions.”

So, at 326PM, I hit the button, “shorting the SP500 (SPY) as it is immediate-term TRADE overbought.” Time Stamped.

What do I do with that position today?

Same answer. The risk management process will tell me what to do. All of my decisions are risk-adjusted to the market’s last price. In other words, Prices Rule my process. Period.

The SP500’s setup is now as follows:

- Immediate-term TRADE overbought = 1290

- Intermediate-term TREND support = 1257

- Long-term TAIL support = 1266

In other words, on any pullback towards 1257-1266, I’ll cover that short position and get longer of US Equity exposure. If 1266 doesn’t hold, I get shorter.

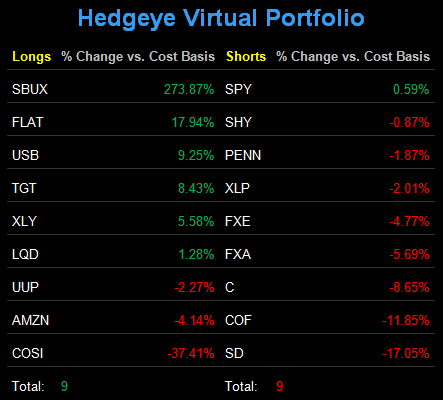

Currently, in the Hedgeye Asset Allocation Model, I have a 9% position in US Equities – that’s all in Consumer Discretionary (XLY). Obviously if I stay wrong on the US Dollar, US Consumption will be adversely affected by inflation. Strong Dollar = Strong America. So with Goldman telling you to chase beta this morning, remember what that implies longer-term – Debauched Dollar = Mad America.

If my long-term bullish case for the US Dollar doesn’t convince you of that – let The People. In the face of the biggest 4-week rally ever, Bloomberg’s weekly Consumer Confidence survey dropped to minus -51.1 versus -48.4 last week. Titillating.

My immediate-term support and resistance ranges for Gold (bullish TRADE and TREND again), Oil (bullish TRADE; bearish TAIL), German DAX (bullish TRADE and TREND; bearish TAIL), and the SP500 are now $1703-1756, $89.36-93.87, 6127-6428, and 1233-1290, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer