TODAY’S S&P 500 SET-UP - November 1, 2011

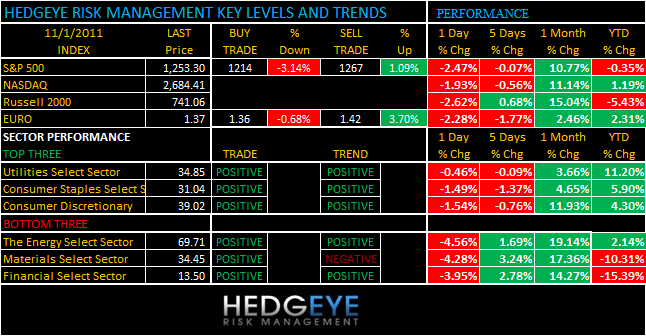

As we look at today’s set up for the S&P 500, the range is 53 points or -3.14% downside to 1214 and 1.09% upside to 1267.

SECTOR AND GLOBAL PERFORMANCE

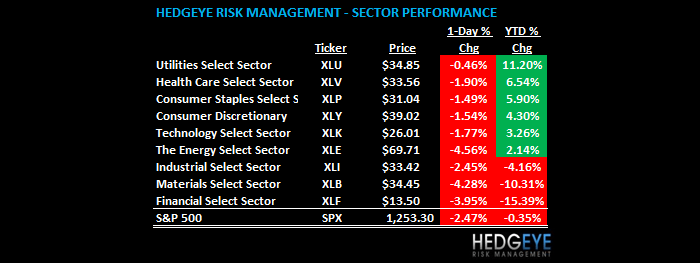

From a TRADE and TREND perspective, today’s selloff didn’t do much to the Sector Studies. The only Sector to break its intermediate-term TREND line today was the one that’s most negatively correlated to a rising US Dollar – Basic Materials (XLB).

That’s the good news. The bad news is that 4 of 9 Sectors failed to succeed in recovering their long-term TAIL lines of support – Financials (down -15.4% YTD), Basic Materials (down -10.3% YTD), Industrials (down -4.3% YTD) and Energy (up +2.1% YTD). Again, these Sectors all have 1 thing in common – they do not like a rising US Dollar like most Americans do. The SP500’s long-term TAIL (1267) broke again today too.

The Hedgeye asset allocation has moved from 0% US Equities this summer to 9% currently and embraces the Bullish Formation (bullish on all 3 risk mgt durations – TRADE/TREND/TAIL) in Consumer Discretionary (XLY) which, in terms of upside from here, looks more attractive to me than Utilities (XLU). We like both, but XLY better; especially if Strong Dollar Deflates The Inflation (= bullish for US Consumption and economic growth in 2012).

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -1908 (-1851)

- VOLUME: NYSE 1143.02 (+13.27%)

- VIX: 29.96 +22.14% YTD PERFORMANCE: +68.79%

- SPX PUT/CALL RATIO: 3.02 from 1.54 (+95.59%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 42.94

- 3-MONTH T-BILL YIELD: 0.01%

- 10-Year: 2.17 from 2.34

- YIELD CURVE: 1.92 from 2.06

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am/8:55am: ICSC/Redbook weekly sales

- 10am: Construction spending, est. 0.3%, prior 1.4%

- 10am: ISM, est. 52.0, prior 51.6

- 11:30am: U.S. to sell $35b 4-wk bills

- 4:30pm: API inventories

WHAT TO WATCH:

- Greek’s PM Papandreou called referendum and parliamentary confidence vote, raising the prospect of derailing European bailout effort and pushing Greece into default.

- Higher output from Honda and Toyota, combined with growing demand for full-size trucks by Ford, GM probably accelerated the SAAR to 13.2m vehicles.

- Mario Draghi to succeed Jean-Claude Trichet as ECB President today

- Congressional supercommittee meets on “Overview of Previous Debt Proposals,” 1pm

- Senate is scheduled to resume consideration of amendments on spending bills

COMMODITY/GROWTH EXPECTATION

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- China Mobile Skirts Apple to Add 5 Million IPhone Users: Tech

- Gisele, Gwyneth, Demi Pose for Testino; Kapoor’s Scary Tunnel

- Record Coal Premium Turning Into Bargain as Deals Sour: Real M&A

- Esprit Drops as Europe Sales Slide on Weaker Demand

- IPhone China Rival Focuses on Software for Half-Price Device

- Sony Revamps TV Business After Seven Straight Annual Losses

- Toshiba, Nippon Yusen Call for More Government Action on Yen

- Mideast Dining Means Darden-Led U.S. Chains Follow Money: Retail

- Amazon Boosts Cloud Computing Sales, Seizing on U.S. Budget Cuts

- Indonesia’s October Consumer Prices: Summary (Table)

- Colonel Sanders Devouring Little Sheep Means 69% Gain: Real M&A

- United Breweries Falls in Mumbai After Quarterly Net Drops 11%

- Thailand Oct. Consumer Prices Rise 4.19% From Yr Ago; Est. +4.5%

- Drinking My Way Through 1,000 Belgian Craft Beers: John Mariani

- Louis Vuitton Store, Offices in London Sold for $28 Million

- *INDONESIA'S OCT. CONSUMER PRICES FALL 0.12% FROM MONTH AGO

- Panasonic Forecasts Biggest Loss in Decade on Strong Yen, TV

- Esprit First-Quarter Sales Rise 0.6% as European Demand Slows

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

Chinese authorities rhetorically signaled that it will be neither a source of “dumb money” for the EFSF, nor will it be pressured into easing too soon.

2007-08 Similarities Watch: Hong Kong Money Supply (M3) turned negative on a YoY basis in Sep like it die in 2Q08

Australia cuts key rate to 4.5% in first reduction since 2009.

MIDDLE EAST

The Hedgeye Macro Team

Howard Penney

Managing Director