For once, we’ve turned positive on JNY. On its path of value destruction, it’s likely to give the ultimate head-fake of $2.00 in earnings power. Even if JNY is holding a balloon underwater, people won’t care – until they have to. The stock should work in the interim.

Conclusion: I’ve turned positive on JNY. Let’s be clear – that’s JNY the stock, not Jones the company. On the path of value-destruction, JNY will likely do the wrong things to the P&L and balance sheet that could take up EPS to the $2+ range before reverting to something closer to a buck. I won’t be the guy who nails the negative TAIL call – which is clearer than ever -- but was too early in the research to avoid being steamrolled on a short by positive TREND and TRADE.

INVESTMENT SUMMARY

This is the strangest note I have ever written on JNY. I started writing it as a bear, and by the time I finished, I found out that I was really bullish.

I am utterly convinced that this company is destroying shareholder value. This is one of the names I’ve gotten right way more often than not over the years -- ALWAYS on the short side. This quarter’s results confirmed how fundamentally flawed JNY’s positioning is, at least to me, in many ways. I initially wrote my thoughts down in that regard.

But when I translated the path of value-destruction to our earnings model (as I always do) the numbers were just staring me in the face. I realized pretty quickly that before people realize that a clean ongoing EPS number is probably closer to a buck, the opacity behind GAAP reporting will give them a reason to once again believe that $2+ is doable. With the stock at $11, not only does that NOT make a good short case, but it makes a pretty good long one.

So…why is this the strangest note I’ve written on JNY? I’m not re-writing the initial part of my note despite my little ‘revelation’ later on. The reality is that the process whereby a perennial bear turned positive on the margin is probably more important to emphasize than the conclusion itself given that duration is so key to this stock.

So in advance, here’s a warning that this note is all over the place – but ends in the right spot nonetheless.

Bottom line. I like this name – for once. Keith’s levels will be critical, as a dip into the single digits could send it the way of LIZ (i.e. from $10 to $5 in a flash if JNY fails to deliver). We can’t take the risk off the table of price wars between JCP and anyone that competes with or sells into JCP. So yeah, that scares me. But if JNY prints $1.75 next year (with the consensus at $1.42) and there’s visibility into $2+ in 2013, will anyone really care that it’s coming from a ‘kick the can down the road’ strategy, and JNY will need to meet its maker and fess up to a $1-$1.25 EPS level? Heck no.

I won’t be the guy who nails the negative TAIL call – which is clearer than ever -- but was too early in the research to avoid being steamrolled on a short by positive TREND and TRADE.

HERE’S WHAT I WROTE TO MYSELF BEFORE SEEING WHERE THE STREET’S ESTIMATES SHOOK OUT…

There was nothing in this JNY print that caused us to change our view on the name. I keep getting the ‘but it’s so cheap’ argument. Those are the same people that are telling me that other names like Nike, Bed Bath, Ralph Lauren, and Under Armour are too expensive. I’ll never say that valuation doesn’t matter, but I will say that other things matter more – like showing that a given company is in control of driving its destiny, while others continue to get steamrolled by not having a proactive process to create value (and avoid mass destruction of value). In addition, with JNY, history shows us that valuation does not matter as much as earnings revisions.

To be clear, over the past ten years, JNY has eroded its profit base down from $605mm in EBIT to $198mm. That’s 67%. It’s enterprise value? Down 68%. Let’s say that the market has properly recognized management’s lack of success.

I think it was Cheryl Crow who said “It’s not having what you want. It’s wanting what you’ve got.” I’m totally killing the spirit of her message by bringing it down to this level, but there are not a whole lot of examples in retail where this applies more.

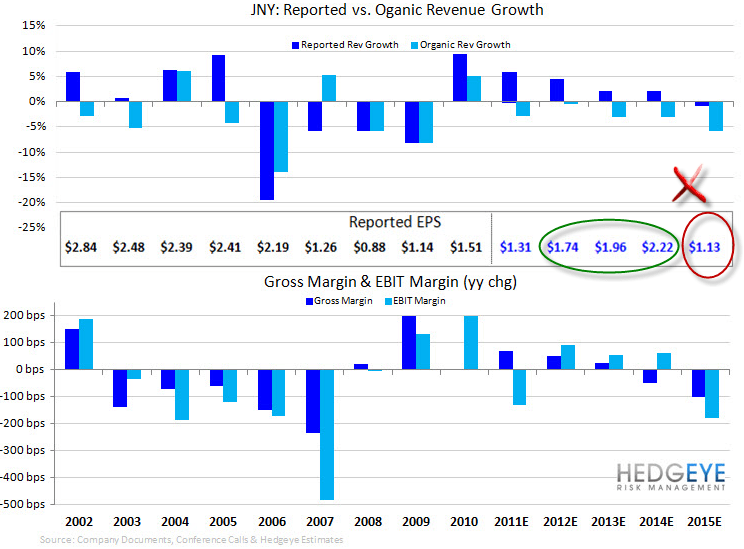

Simply put, the company buys things to mask attrition in previously acquired brands. That’s the model – its as simple as that. This chart tells us so much about JNY over the years. Organic growth is rare, and when they get it, they usually have to buy it on the Gross Margin line. EPS has been a volatile annuity of around $1.50.

But that’s history. We don’t buy stocks using a hindsight model – at least not if we want to be sitting in our chairs in a year’s time.

The intellectually honest questions from here are 1) Has the strategy/business model changed? If so, then 2) Does JNY have the talent to execute change, and 3) Is there enough cumulative investment spend/infrastructure to sustain a healthy organic top line growth rate? Then, the ultimate question revolves around timing for realization of success/failure vs. expectations.

The reality is that the answer to question 1 is ‘No’. Here are some points from the quarter as to why this is the case. Then I’ll move to duration.

Wholesale Sportswear

Management: “At wholesale the Jones New York Easy Care program experienced another great quarter of double-digit sales growth, while our Replenishment Suiting sales volume increased 56% versus last year.”

Hedgeye Retail: Then why was that category down 10.7%?

Wholesale Jeanswear was down 18.1%. Do you believe that? This is the same quarter where JNY confirmed that it was in talk to sell the division. I wonder if Delta Galil Industries knew about these numbers when the talks began.

Domestic Wholesale Footwear and Accessories: Really solid performance here. Sales were up 5.2%, which was driven by a new partnership with Brian Atwood, which had what appears to be a successful sell-in to super-high end channels like Saks and Neiman (also Nordstrom and Bloomies).

While I give ‘em all the credit they deserve in my model, I sit back and ask myself “What value did Jones add here that others CANNOT? Ultimately, is there someone closer to the source that could take out JNY as middleman and get the product to consumers at a more accessible price OR at a higher margin to Atwood and the actual manufacturer? The answer is Yes. That’s the problem when you rely on licensing in other brands to grow.

JNY’s total top line growth in the quarter? Not the anemic 2.2% reported, but rather the horrible -5.4% organic when you back out deals.

SG&A in the quarter when you exclude deals? Flat. How can you expect core content to grow when you don’t invest in it?

Internally, they don’t. That’s why they need to add on Stuart Weitzman. That’s why they need Atwood. That’s why they need Kurt Geiger (the only reason why International sales doubled.)

What next?

1) Benefit initially from momentum of new content.

2) Then financially/operationally engineer the new brands and acquisitions to keep margins high.

3) Kick the can down the road as much as they can before lowering growth outlook.

4) Write off asset values and/or lose license agreements as JNY misses performance targets.

5) Do more deals to keep the hope alive.

One key consideration? With LT Debt to Capital sitting at 42%, JNY doesn’t quite have the balance sheet that it used to. I’m not suggesting that it has liquidity or counterparty risk. That’s not the case by any means.

Until the company shows me that it’s going to do what it needs to do to either a) be committed to developing its existing bench, or b) sending half the team to the minors and compete with a smaller and more focused group (a la LIZ), then JNY simply is not worth it for me unless I can find glaring holes in expectations.

[NOTE TO READER: THIS IS WHERE I CLICKED PAUSE FOR THREE DAYS TO SEE WHERE ESTIMATES SHOOK OUT, AND THE BULL EMERGED FROM ITS CAVE].

- I found glaring holes in expectations.

- The more I thought about it, points 1 through 5 above realistically take 2-3 years to play out. That’s like an eternity to Wall Street.

- For many reasons – almost every one of them related to an acquisition – we’re coming up with an EPS estimate of $1.74 next year. The street is at $1.43. Does a 22% upwards revision matter for a small volatile name like JNY? Yes.

- This business – as below average as it might be – still throws off cash, and is not capex intensive. Based on our model, JNY could buy back 10% of the company per year at the current rate. Will it? No way. As noted it’s much more interested in buying brands and stock in other entities as opposed to its own. But as long as folks can pull out their HPs and run these numbers – even on a more beared-up model – the argument will be there.

- This company has proven to be VERY good at holding balloons under water. It can do it for a fairly long time – much longer than most people (including me) think. When the balloon is released, however, it not only deflates, but it flat-out explodes and gets torn to shreds. So how can I be positive on the stock when I think this will happen again? As noted above, even though I have EPS by 2015 BELOW current levels, it will be driven by unhealthy actions along the way that should allow the company to not only beat, but give the Street reasons to think that it is sustainable.

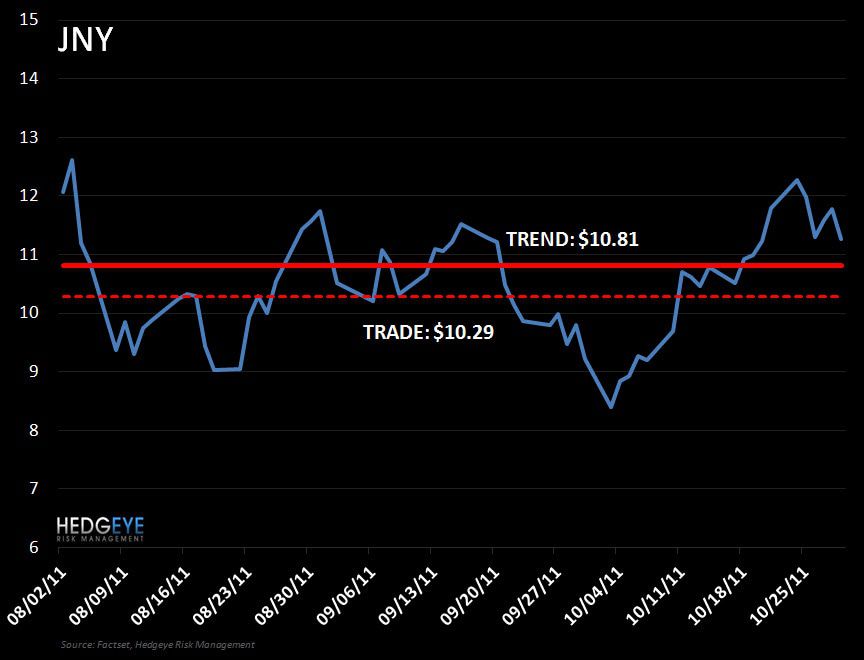

In Hedgeye speak, this name is still very negative TAIL (3-years or less), but as negative as it is on a TAIL duration, it is positive on TREND (3 months or more). As it relates to TRADE (3-weeks or less), we definitely want to be careful on this one. Right now, we’re looking at bullish TRADE and TREND lines converging b/t 10.29-10.81.

Brian P. McGough

Managing Director