Positions in Europe: Short EUR-USD (FXE)

Despite the significant bounce in European equity markets on 10/27 following announcements from the EU Summit, the market is increasingly (and again) pricing in downside as the “package” turned out to be more “trick” than “treat”, namely because the details on reinforcing the EFSF, the recapitalization of banks, and solutions for Greece’s persistent default issues were not provided.

One main cross-current that is developing is the dichotomy between Fitch ratings agency and ISDA on the implications of investors taking a “voluntary” haircut on their Greek holdings. ISDA’s letter of the law clearly states that so long as it’s a voluntary haircut, CDS will not be triggered to payout for default. However, Fitch clearly argues that a 50% reduction in debt payoff is default. This limbo leaves a lot of uncertainty for investors and should ultimately force the hand of Eurocrats to bring resolve to the issue. Should Eurocrats tip-toe around the issue (which is highly probable), expect investor appetite for European debt, particular for the periphery, to wane, which should put additional pressures on existing “temporary” facilities like the SMP to solve for demand of secondary sovereign issuance.

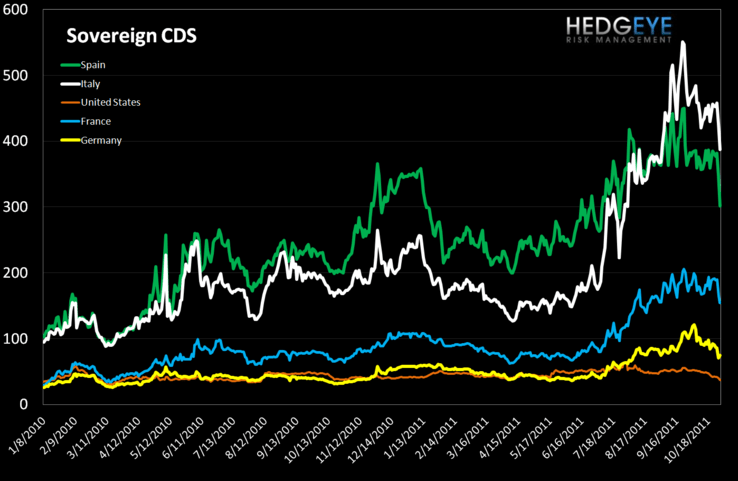

The outcome of this limbo would suggest we’re likely to see a new divergence that may drive swaps and yields in opposite directions at times, making yields the more appropriate risk benchmark. Here we’d point to Italy’s 10YR in particular, currently at 6.14%, and over the historically significant 6% that signaled a expeditious breakout line for Greece, Ireland, and Portugal requiring bailouts, as an important risk signal (see below).

European Sovereign CDS – European sovereign swaps tightened considerably last week on the heels of the Eurozone summit. French and German spreads tightened 10.6% and 8.5% respectively.

We remain short the EUR-USD via the etf FXE in the Hedgeye Virtual Portfolio. We’re still of the opinion that Europe’s road to a recovery is a long one, and ultimately growth expectations will have to come in lower as austerity erodes tax revenues, business and consumer confidence, and heightens joblessness. We think the EUR-USD cross is the relative loser over the near term as indecision on a policy to move the region beyond the sovereign and banking crisis persists and the ECB is more likely to cut its main rate over the intermediate term. We'd hope but don’t expect to see any clear smoke signals coming from this Thursday’s G20 meeting in Cannes on the aforementioned main topics of reinforcing the EFSF, bank recapitalizations or Greek haircuts. Expect rumors to float that the BRICs could ride in on a white horse.

European Financials CDS Monitor – Bank swaps were tighter in Europe last week for 38 of the 40 reference entities. The average tightening was 8.1% and the median tightening was 16.6%.

Matthew Hedrick

Senior Analyst