Trouble viewing the charts in this email? Please click the link at the bottom of the note to view in your browser.

* The TED spread made a new YTD high at 42.9 bps, indicating that credit markets remain skeptical of the EU "bailout".

* Credit default swaps for Eurozone countries tightened, but Italian bond yields hit new highs. This may be reflecting a new divergence between yields and swaps due to the counterintuitive ISDA conclusion that a 50% Greek debt haircut is not a default. The ramifications are that this may drive swaps and yields in opposite directions at times, making yields the more appropriate risk benchmark.

* Credit markets are signing a different tune than equity markets. Greek 10-yr bond yields came in just 80 bps to 23.24%, suggesting that the credit market is far less impressed by the summit’s results than the equity market was.

* Mortgage insurer CDS increased even further, indicating a still growing probability of default for RDN and MTG.

* The short term (TRADE) downside/upside setup in the XLF is currently 5 to 1 (6.3% downside vs. 1.2% upside).

Margin Debt Falls in September

We publish NYSE Margin Debt every month when it’s released.

NYSE Margin debt hit its post-2007 peak in April of this year at $320.7 billion. The chart below shows the S&P 500 overlaid against NYSE margin debt going back to 1997. In this chart both the S&P 500 and margin debt have been inflation adjusted (back to 1990 dollar levels), and we’re showing margin debt levels in standard deviations relative to the mean covering the period 1. While this may sound complicated, the message is really quite simple. First, when margin debt gets to 1.5 standard deviations or greater, as it did this past April, that has historically been a signal of extreme risk in the equity market - the last two times it did this the equity market lost half its value in the ensuing period. We flagged this for the first time back in May of this year.

The second point is that margin debt trends tend to exhibit high degrees of autocorrelation. In other words, the last few months’ change in margin debt is the best predictor of the change we’ll see in the next few months. This is important because it means that margin debt, which has retraced back to +0.43 standard deviations as of September, still has a long way to go. We would need to see it approach -0.5 to -1.0 standard deviations before the trend reversed. There’s plenty of room for short/intermediate term reversals within this broader secular move, but overall this setup represents a material headwind for the market.

One limitation of this series is that it is reported on a lag. The chart shows data through September.

Financial Risk Monitor Summary (Across 3 Durations):

- Short-term (WoW): Positive / 8 of 11 improved / 2 out of 11 worsened / 1 of 11 unchanged

- Intermediate-term (MoM): Positive / 8 of 11 improved / 1 of 11 worsened / 2 of 11 unchanged

- Long-term (150 DMA): Negative / 1 of 11 improved / 8 of 11 worsened / 2 of 11 unchanged

1. US Financials CDS Monitor – Swaps tightened across every major domestic financial company last week except the three mortgage insurers. Swaps widened at MTG and RDN as PMI swaps tripled.

Tightened the most vs last week: LNC, PRU, HIG

Widened the most vs last week: PMI, MTG, RDN

Tightened the most vs last month: C, MS, HIG

Tightened the least/widened the most vs last month: PMI, RDN, AGO

2. European Financials CDS Monitor – Bank swaps were tighter in Europe last week for 38 of the 40 reference entities. The average tightening was 8.1% and the median tightening was 16.6%.

3. European Sovereign CDS – European sovereign swaps tightened considerably last week on the heels of the Eurozone summit. French and German spreads tightened 10.6% and 8.5% respectively.

4. High Yield (YTM) Monitor – High Yield rates fell 30 bps last week, ending the week at 7.83 versus 8.13 the prior week.

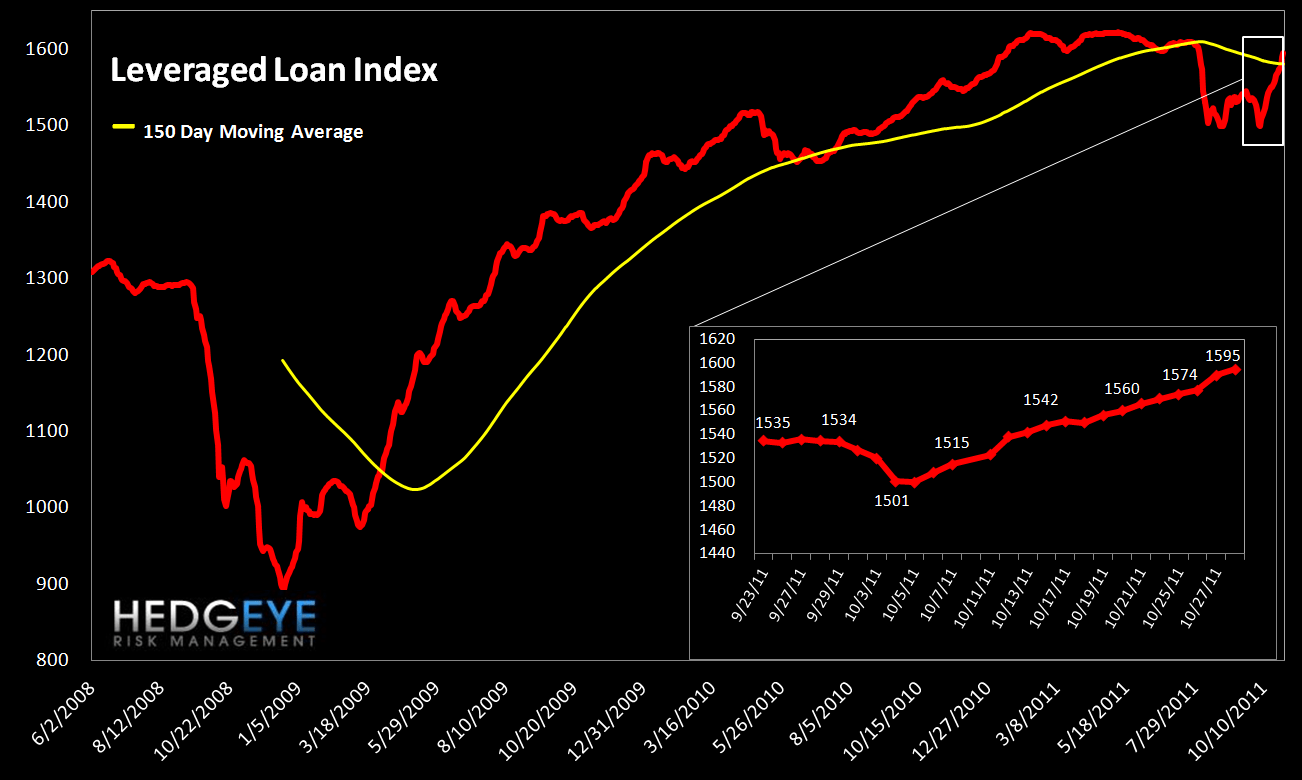

5. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 29 points last week, ending at 1595.

6. TED Spread Monitor – Last week the TED spread hit another new YTD high, ending the week at 42.9 bps.

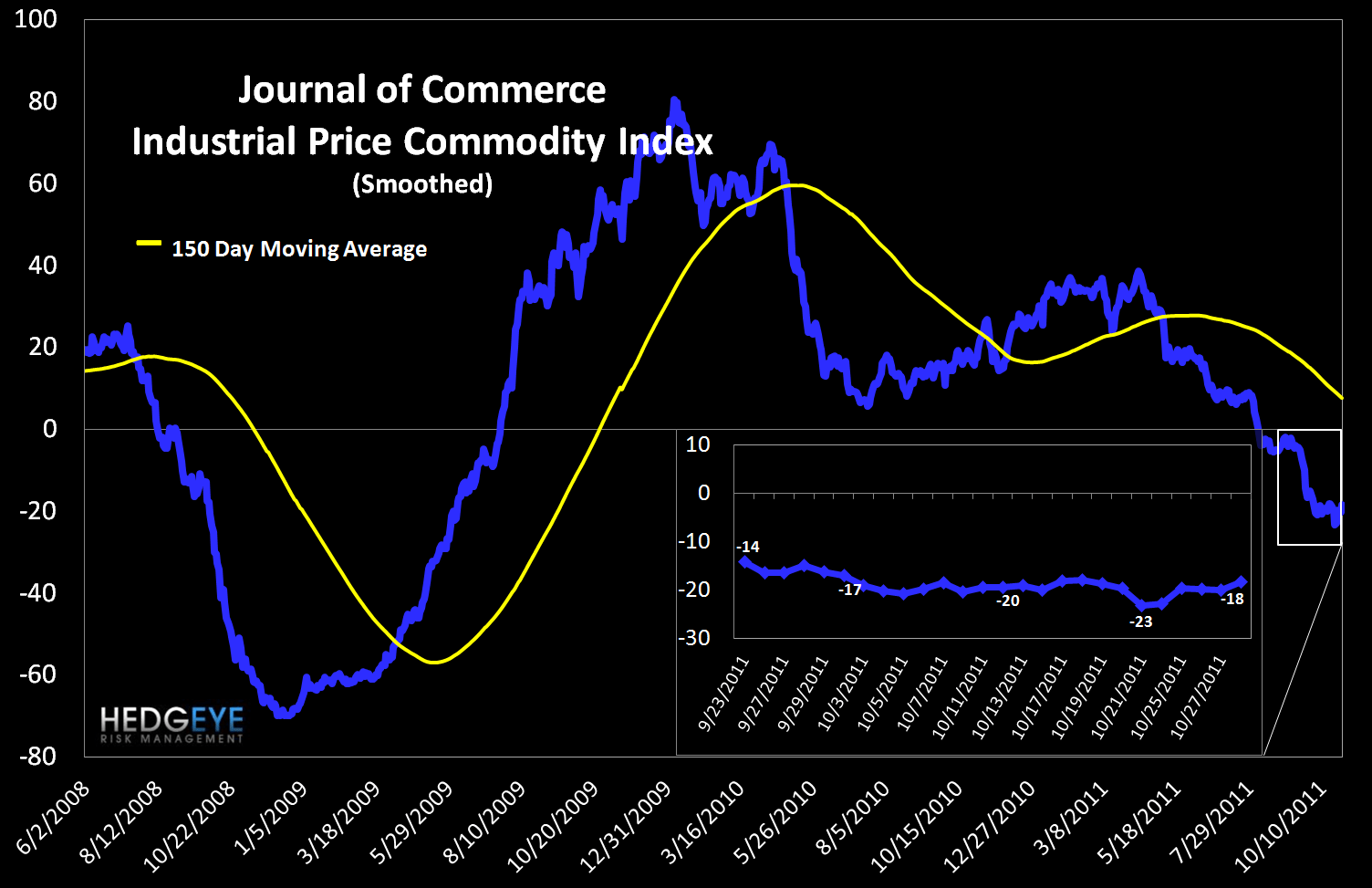

7. Journal of Commerce Commodity Price Index – The JOC index rose 4.9 points, ending the week at -18.5 versus -23.3 the prior week.

8. Greek Yield Monitor – The 10-year yield on Greek debt fell just 80 bps last week, ending the week at 2324 bps. Bond market investors were largely unimpressed by the results of the Eurozone summit, standing in contrast to equity market investors.

9. Markit MCDX Index Monitor – The Markit MCDX is a measure of municipal credit default swaps. We believe this index is a useful indicator of pressure in state and local governments. Markit publishes index values daily on six 5-year tenor baskets including 50 reference entities each. Each basket includes a diversified pool of revenue and GO bonds from a broad array of states. We track the 14-V1. Last week spreads tightened sharply, ending the week at 151 bps versus 174 the prior week.

10. Baltic Dry Index – The Baltic Dry Index measures international shipping rates of dry bulk cargo, mostly commodities used for industrial production. Higher demand for such goods, as manifested in higher shipping rates, indicates economic expansion. Last week the index fell 135 points, ending the week at 2018 versus 2153 the prior week.

11. 2-10 Spread – We track the 2-10 spread as an indicator of bank margin pressure. Last week the 10-year yield rose to 2.32, pushing the 2-10 spread to 203 bps, 8 bps wider than a week ago.

12. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 1.2% upside to TRADE resistance and 6.3% downside to TRADE support. The downside/upside setup is currently 5 to 1.

Joshua Steiner, CFA

Allison Kaptur

Having trouble viewing the charts in this email? Please click the link below to view in your browser.