THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

Consumer Data

Personal Income growth in September came in at +0.1% versus expectations of +0.3% while Personal Spending came in at +0.6%, in line with Street expectations. PCE Core came in at +1.6% y/y in September versus +1.7% expectations. Consumers are decreasing their savings rate to spend. This is not sustainable but, as we have seen in the past, stimuli can come via many different levers. Nevertheless, the slow quarter-over-quarter personal income growth – worst since 2009 – is a looming cloud over the economic data this morning.

Inflation

One of the top stories on Bloomberg this morning is titled “Restaurants Lift Prices to Catch Food-at Home Inflation”. As we have been highlighting for some time, restaurants have some room to raise prices given the much bolder price hikes being taken in the grocery aisle. The article is an interesting read, highlighting the “low cost entertainment” that eating out represents.

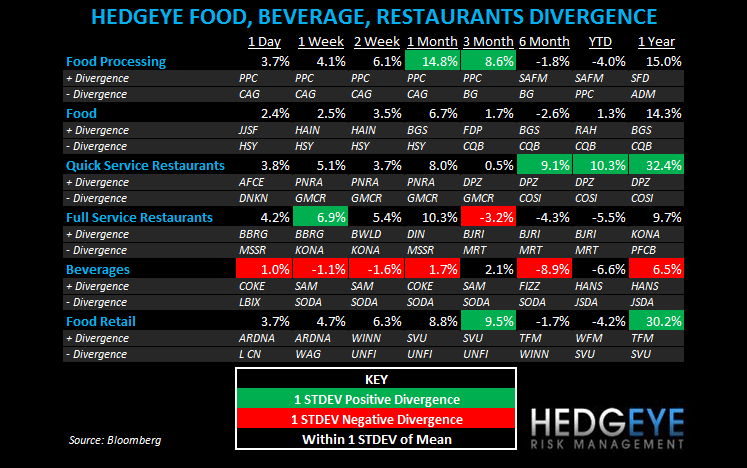

SUBSECTOR PERFORMANCE

QUICK SERVICE

ARCO: Arcos Dorados reported third quarter earnings and cut its revenue and EBITDA growth ranges. Company sees full-year revenue growth 21-23% and adjusted EBITDA growth of 14-16%.

CASUAL DINING

EAT: Brinker was the target of many skeptics over the past 24 or 36 hours. Sterne Agee’s take on the stock was known yesterday but republished in Barron’s subsequently. As we had suspected before seeing the details, caution on “Brinker’s ability to grow top line on a sustainable basis” is the reason behind the downgrade. We take the other side of that bet, see our post from yesterday.

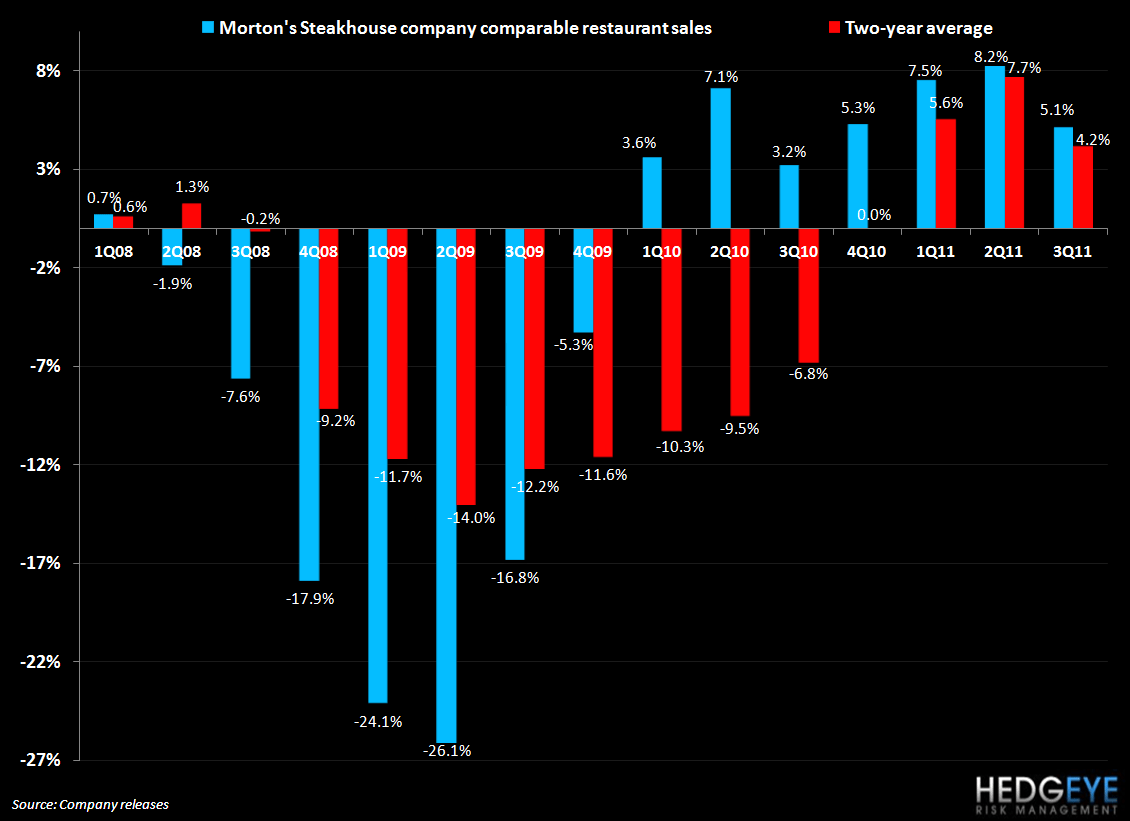

MRT: Morton’s Restaurant Group reported a 3Q loss of -$0.11 versus expectations of -$0.112. Comps came in at +5.1% which, as the chart below illustrates, implies a decline in two-year average trends. On beef prices, Morton’s sees 5-10% inflation in 2012 but “have no real basis” for that number yet other than the bullishness they perceive from the beef processors on their pricing power. Even as beef prices continue to go higher, MRT has 70% of beef needs for 2011 on a floating basis. 70% of 4Q needs are contracted, however. In terms of demand and/or mix, Morton’s has not seen any substitution to seafood or other substitutes. Of course, the consumer profile at Morton’s is not analogous to the general U.S. consumer but it is an interesting data point nonetheless that could indicate further pricing power for the brand. Wall Street and Corporate America layoffs may be changing this however.

CPKI: Golden Gate Capital has closed its latest fund at $3.5 billion, according to the NYT. The fund had purchased a wide range of companies over the last twelve months, including California Pizza Kitchen.

Howard Penney

Managing Director

Rory Green

Analyst