THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP - October 28, 2011

We’ve just seen the biggest 4 week rip in US stocks in 40 years and that’s a long time. As we look at today’s set up for the S&P 500, the range is 24 points or -1.45% downside to 1226 and 0.42% upside to 1290.

SECTOR AND GLOBAL PERFORMANCE

Keith traded SPY as well as he could have this week (short Monday at 1258, covered Wednesday 1227, re-shorted Thursday 1290) but got killed in the long US Dollar position:

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: +2321 (+482)

- VOLUME: NYSE 1430.62 (+28.99%)

- VIX: 25.46 -14.74% YTD PERFORMANCE: +43.44%

- SPX PUT/CALL RATIO: 1.60 from 1.63 (-16.23%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 41.79

- 3-MONTH T-BILL YIELD: 0.02%

- 10-Year: 2.42 from 2.23

- YIELD CURVE: 2.11 from 1.95

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30 a.m.: Employment Cost Index: est. 0.6%, prior 0.7%

- 8:30 a.m.: Personal income, est. 0.3%, prior -0.1%

- 8:30 a.m.: Personal spending, est. 0.6%, prior 0.2%

- 9:55 a.m.: UMich Confidence, est. 58.0, prior 57.5

- 1 p.m.: Baker Hughes rig count

WHAT TO WATCH:

- MF Global said to draw down its revolving credit lines this week

- European officials are studying the potential for an IMF channel for money for their enlarged rescue fund, as China considers contributing

- Sprint Nextel, Clearwire said to be near agreement to extend their existing network-sharing agreement for 3-5 yrs

- HP CEO Meg Whitman abandoned Leo Apotheker’s proposal to spin off the personal computer unit

COMMODITY/GROWTH EXPECTATION

COMMODITIES - with USD down hard, I’m happy I wasn’t short anything Commodities yesterday, but looking at the short side again today as the core 3 lines of resistance (CRB Index TREND = 327, Oil’s TAIL of $93.87, and Copper’s TREND of 3.91 remain intact).

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- Thai Floods Swamp Grand Palace as Bangkok River Reaches Record

- Copper Traders See Rally Ending as China Use Slows: Commodities

- S&P 500 Extends Best Month Since ’74, Euro Rises on Debt Accord

- Cheapest Gas Spurs Canadian LNG Boom for Asia: Energy Markets

- Oil Drops on Japan Output, Pares Biggest Weekly Gain Since March

- Gold Heads for Best Week Since August After European Debt Accord

- Thai Floods ‘Underestimated’ as Stocks Rally: Chart of the Day

- Hello Kitty Coin Is New Weapon in Swiss Refiners’ Currency War

- Copper Pares Biggest Weekly Advance Since 1986 on Japan Data

- Vale Ready to Sell Iron Ore on Spot Market as Prices Slump

- China’s Pork Imports May Rise to Record on Low U.S. Prices

- COMMODITIES DAYBOOK: Crude Oil Declines After Japan Output Data

- Wheat Drops on Higher Global Reserve Estimates, Corn Declines

- Copper Falls in London After Japan’s Factory Output: LME Preview

- Zinc May Rebound 30% on TD Buy Signal: Technical Analysis

- China’s Hu Will Focus on EU Debt, Commodity Prices at G20: Cui

- Palm Oil Drops as Investors Sell After Rally to One-Month High

- Oil Drops, Paring Biggest Gain Since March on Japanese Output

- Oil Rises to 3-Month High on U.S. Economy, European Debt Deal

- Rubber Caps Best Week Since November as Growth Outlook Improves

CURRENCIES

US DOLLAR – closing below my 75.37 TREND line of support on a meltdown day for the US Dollar Index (squeeze in the Euro) is the #1 factor in all of my Global Macro model (the USD has a -0.95 and -0.97 inverse correlation to US and European stocks, respectively = one way risk that works both ways). If the USD can’t recover by TREND line in the next 3 weeks, I’m out.

EUROPEAN MARKETS

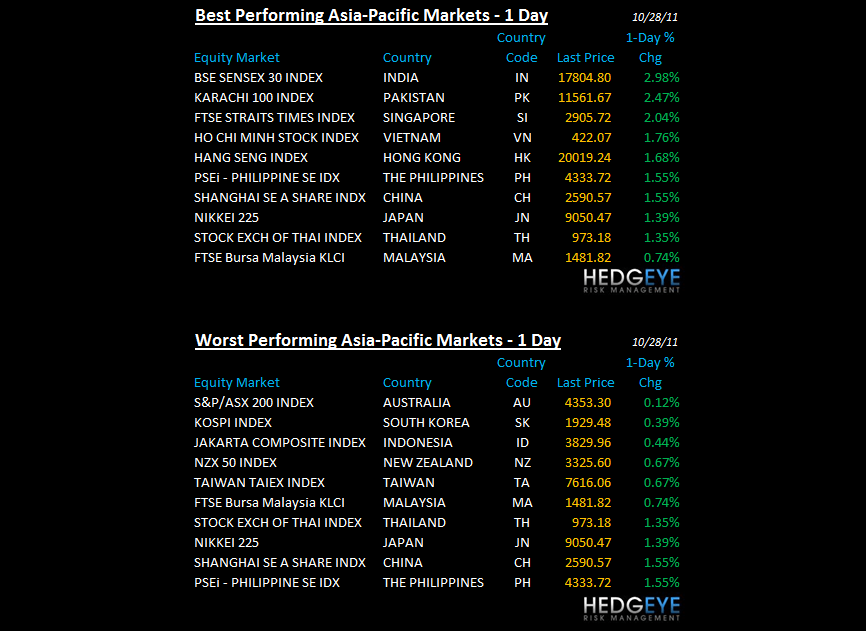

ASIAN MARKETS

ASIA – after closing down -4.7% last week, China closed up every day this week… having fun w/ the China is going away thesis yet? We have not been in that camp, but we do think Chinese GDP doesn’t bottom sequentially until Q1 of 2012, so watch the Shanghai Comp closely now that it has recovered it’s TRADE support line of 2411 (still bearish TREND up at 2563.

MIDDLE EAST

The Hedgeye Macro Team

Howard Penney

Managing Director