This note was originally published at 8am on October 24, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“We should not deceive ourselves into thinking that when we die we shall be remembered intensively for more than a limited number of days.”

-Siegmund Warburg, 1974

Last week I started reading Niall Ferguson’s “High Financier – The Lives and Time of Siegmund Warburg.” Interestingly, but not surprisingly, Ferguson chooses to preface the 19th century history of the Rothschild and Warburg families by giving you a hint about how it all ended for central bankers in the 1970s (it didn’t end well).

If you re-read the aforementioned quote and think about it within the context of what is going on in the world of banking today (either central banking or bailout banking, or both), this is the root of the problem. These people don’t appreciate the lessons of history. They live in the now and react to whatever fire they need to put out next. There is no such thing as being proactively prepared for the long-term.

In the long-run, Keynes excused himself (and the responsibility in the recommendation of his policies) by reminding politicians that “we are all dead.” That’s a sad and pathetic way to think about leadership and legacy. It’s also one that the Western World had enough of come 1978.

Back to the Global Macro Grind…

Regardless of how I continue to think the biggest man-made money printing bazooka in world history is going to end (structurally impaired long-term growth), our risk management task this morning also needs to consider dealing with the right here and now.

In the last 3 weeks I have dropped my Cash position in the Hedgeye Asset Allocation Model from 73% to 58%, and here’s how I’m thinking of positioning into and out of what should be a disappointing European Summit “catalyst” on Wednesday:

- Cash = 58% (down from 61% last week)

- International Currency = 18% (US Dollar – UUP)

- Fixed Income = 18% (US Treasury Flattener, Long-term Treasuries, and Corporate Bonds – FLAT, TLT, and LQD)

- US Equities = 6% (Consumer Discretionary – XLY)

- International Equities = 0%

- Commodities = 0%

Looking at these positions in the order that they appear:

1. US Dollar – the US Dollar Index was down -0.3% last week, closing down for the 2nd consecutive week, but remains up +4.7% since Ben Bernanke’s beginning of the end of QE2. Despite Obama and his politicized Fed whispering everything they can about stimulus and housing bailouts last week, I think the political inertia remains at the US Dollar’s back.

2. Fixed Income – the Growth Slowing TREND we’ve been calling for throughout all of 2011 has manifested in the US Treasury Curve flattening. While the market is telling me that growth is slowing at a slower pace (bullish for the immediate-term TRADE in stocks and bearish for bonds), the intermediate-term TREND levels for both the Flattener and long-term Bonds remain bullish.

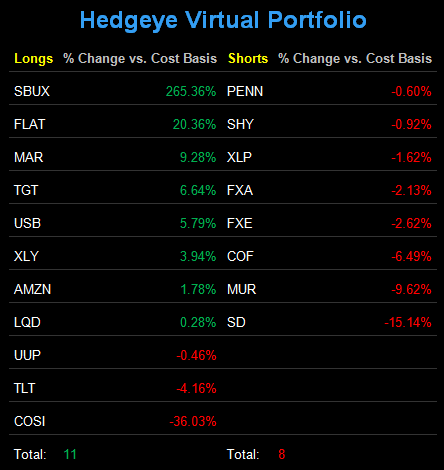

3. US Equities – my two favorite S&P Sectors (Utilities and Consumer Discretionary) are now up +11.3% and +5.1% for 2011 YTD, respectively. With Utilities finally achieving immediate-term TRADE overbought last week, I sold our XLU and stayed with the Strong Dollar = Strong America trade (US Consumption). Most of the domestic consumption stocks we like fit this same theme (MAR, TGT, etc…).

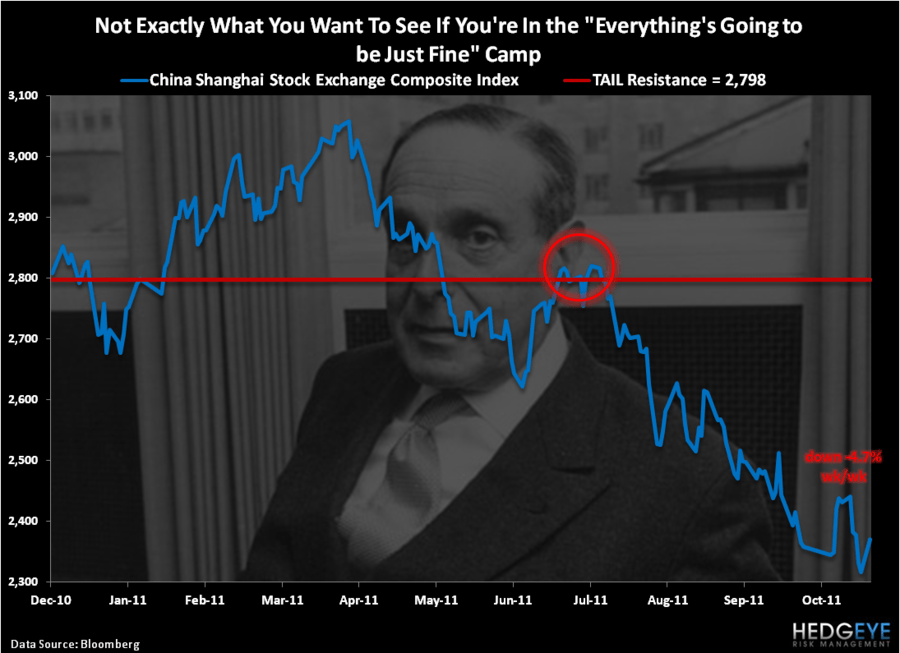

4. International Equities – not being long most things Asian Equities last week was a good call. Asian equity markets closed down another -1.2% wk/wk. Losses were led by China (-4.7%) and Thailand (-4.1%), as both struggled with heightening domestic risks associated with Growth Slowing. I’m not touching anything European Equities at these lower-highs with a 1,000 foot Keynesian pole.

5. Commodities – not here, not now. The US Dollar’s 2 weeks of weakness does not a TREND make. Inclusive of this morning’s +3.2% mean reversion bounce in the price of Copper, the Doctor remains in what we call a Bearish Formation (bearish TRADE, TREND, and TAIL). The CRB Commodities Index and Gold were both down another -1.9% and -2.8% last week. That’s good for consumers, not commodity long positions – which just saw their long “bets” (CFTC options contracts) rise +12% last week with hedge funds chasing.

On weakness (earlier in the week), I covered our short positions in US Housing (ITB), Oil (OIL), and the Financials (MS and C), so we actually had a pretty good week. No one ever went to the poor-house booking gains on the short side.

Where could I be wrong from here?

That answer obviously resides where it has for all of 2011 – led by the direction of the US Dollar Index versus the Euro.

Get the US Dollar right and you’ll get a lot of other things right. This is something our political and academic elite should think long and hard about as they try to fix their long-term policy mistakes with more short-term policies.

Sadly, in the short-term, I have no reason to believe that these people won’t continue to Deceive Themselves into thinking whatever it is that they think as the rest of us commoners are thinking about meeting payrolls.

In the short and long-run, I am fairly certain that if I do not succeed, both my family and firm will remember my mistakes intensively for plenty more than “a limited number of days.”

My immediate-term support and resistance ranges for Gold, Oil, the German DAX, and the SP500 are now $1622-1659, $86.34-88.98, 5761-6116, and 1220-1239, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer