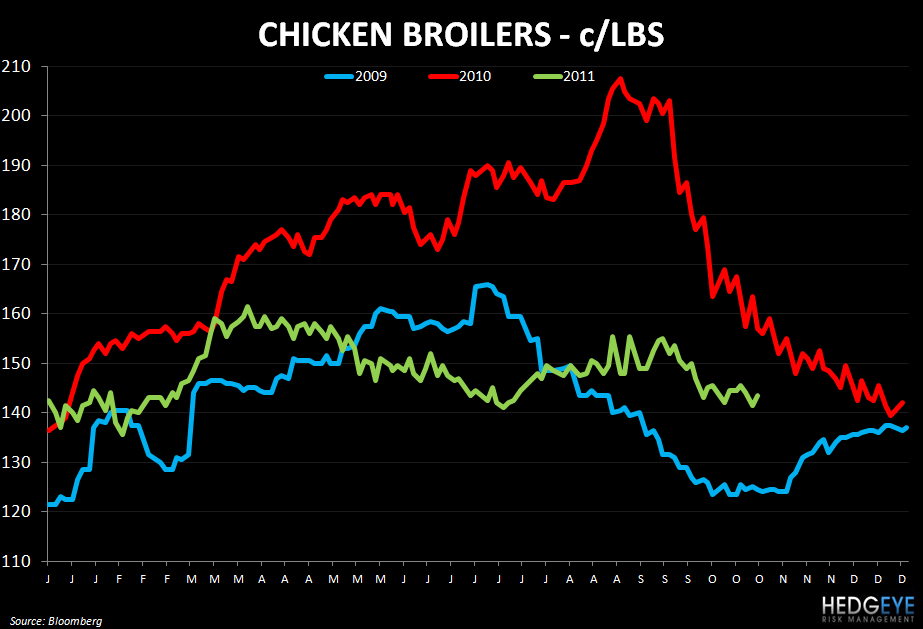

Commodities were mixed over the last week; as the dollar moved lower, grains, dairy and proteins were varied in their respective reactions. Corn, wheat, coffee, beef, milk and chicken wings all went higher while broilers, cheese, soybeans and pork all declined.

STOCK THOUGHTS

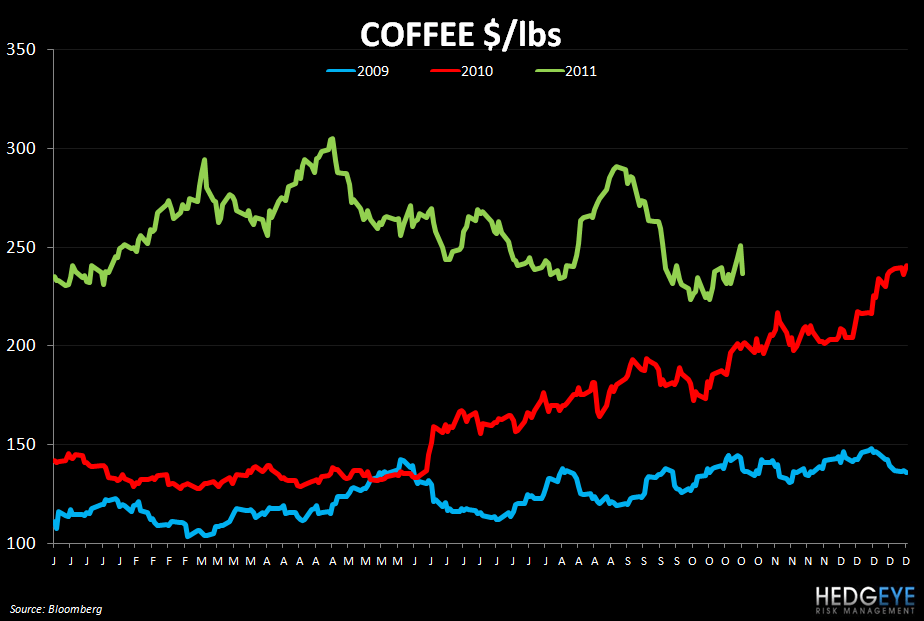

Coffee prices gained over the last week but have largely been coming down quarter-to-date which has improved investor sentiment for coffee retailers like SBUX, PEET, DNKN, THI, and MCD. While prices are down almost 20% quarter-to-date, coffee retailers are going to take some time to work through inventory purchased at higher prices so in-store prices will likely remain high for consumers.

Wheat and corn prices going higher is a negative for companies exposed to protein costs – particularly beef as other supply/demand dynamics continue to support price. In particular, WEN, TXRH and RUTH continue to experience pressure from elevated beef prices. The trend could last for at last another year, according to some analysts (see “summary” below).

SAFM and TSN, and the broader food processing space, would benefit greatly from a prolonged step-down in grain prices. We know from the SAFM Investor Conference last week that the company purchased 30-50% of their corn and soybean meal needs through March 2012 during the recent dip.

Chicken Wing prices resumed their move higher and, per our note published on Monday, we expect significant inflation in wing prices starting in 1Q for BWLD.

CORRELATION TABLE

SUMMARY

- Coffee has risen over the last week as speculation mounts that rains in producing regions of Central America and also Vietnam will impact exports. Rain in Vietnam has pushed back the schedule for the crop while downpours in Central America may result in crop losses of as much as 1 million bags, according to Archer Consulting, a Brazil-based firm.

- The gain last week in wheat prices was partially driven by the dry weather in the most drought-affected areas of Texas and Oklahoma that some believe will lessen the prospects of newly planted U.S. crops before winter. At the same time, Russian competition and concerns over the global economy are weighing on prices today.

- Corn traded lower over the week as positive reports from the harvest in Illinois came back positive. Across the growing regions of the U.S., though, yields are highly variable and demand has been reacting to recent dips quite quickly. Finally, data from the CFTC shows that speculators increased their net-long positions during the week ended 10/18.

- Cattle herds are likely to continue to shrink for at least another year, according to Cattle-fax analyst Kevin Good, cited on cattlenetwork.com. This year’s drought has exacerbated the declined and, should this trend continue next year it would be bullish for beef prices.

CHARTS

Coffee

Corn

Wheat

Beef

Chicken (Broilers)

Chicken Wings

Cheese

Milk

Howard Penney

Managing Director

Rory Green

Analyst