We are reminded every day how humbling this business can be. For me, PNRA is the latest example.

Consistent with the trends reported to date this earnings season, PNRA 3Q11 results and forward looking commentary are better-than-expected and driven by strong top line momentum. The strong sales momentum is allowing the company to fight off accelerating inflation trends, leading to higher EPS guidance for both FY2011 and FY2012. PNRA reported 3Q EPS of $0.97, exceeding guidance of $0.92-$0.94 and our $0.94 estimate that matched consensus.

Panera is the sixth concept within the domestic QSR space to have reported same-store sales results for the third (calendar) quarter. Of those, three (YUM) have reported negative comps and three have reported sequential decelerations in two-year average trends. Company-operated café same store sales at Panera increased 6% in the third quarter including a strong 7.8% figure in the month of September. The 3Q11 two-year number declined from 7.0% to 5.8%.

The Company-owned comparable net bakery-cafe sales increase in 3Q11 was comprised of transaction growth of 2.6% and average check growth of 3.4%. Importantly, the average check growth was comprised of price increases of approximately 2.5% and positive mix impact of approximately 0.9%. The improvement in mix comes after two consecutive quarterly declines.

Restaurant level margins were up about 160 bps year-over-year despite food costs that were up 160 bps as PNRA gained leverage in nearly every other line item. We see this trend ending in 4Q11, but that will also be functions of sales trends which seem to have strong momentum; for the first twenty-seven days of the fourth quarter, comparable bakery-café sales growth was +6.7% (shown in first chart, below). Additionally, despite 50-100 basis points in anticipated operating margin deleveraging, the company raised its EPS target for 2011 to $4.63-$4.65. The company also initiated FY12 EPS growth of between 16% and 18% versus the midpoint of the FY11 range.

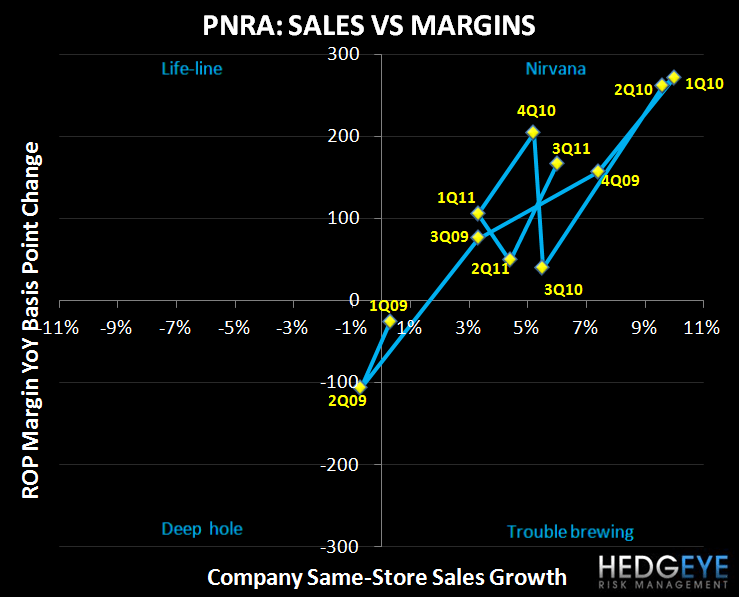

Putting it all together, PNRA continue to post results that are in the “Nirvana” quadrant of our sales versus margin chart. Not many operators are posting positive same-store sales and expanding margins. Our research has indicated that companies that do typically see their stock awarded a higher multiple by the street. The earnings call is later this morning but we doubt there will be any significant news or data point that would lead to concern about the company’s performance in the near-term.

Howard Penney

Managing Director

Rory Green

Analyst