“Hope is nature’s veil for hiding truth’s nakedness.”

-Alfred Nobel

In one of the more ironic moments of 2011, Professor Tom Sargent from New York University won the Nobel Prize of Economics. Sargent was awarded the Nobel Prize for his work on rational expectations. In effect, this is the theory that postulates that policy makers cannot systematically influence the economy via predictable policy changes.

This idea, of course, flies in the face of the current philosophy of the leading central bankers around the world and, in particular, Chairman Bernanke. In the guise of transparency, not only does Chairman Bernanke foreshadow most of his moves, but he now also holds a quarterly press conference to further alert the market as to his future intentions. Undoubtedly, wherever he is now, Alfred Nobel is finding this moment in economic history somewhat ironic.

The concept of “too big to fail” has now wholly pervaded the economic landscape. Sargent, as the key proponent of rational expectations, has some interesting thoughts related to failure. His views likely do not reflect “the conscience of a liberal”, like those of his Nobel Laureate counterpart Paul Krugman, but they do offer some interesting counterpoints to the current debates in economic policy circles. In a June 2010 interview with the Minnesota Fed, Sargent made a number of noteworthy comments relating to the European debt situation, specifically:

“Remember that under the gold standard, there was no law that restricted your debt-GDP ratio or deficit-GDP ratio. Feasibility and credit markets did the job.

Here is what went haywire. In the 2000s, France and Germany, the two key countries at the center of the Union, violated the fiscal rules year after year.

So, a number of countries at the European Union economic periphery—Greece, in particular—violated the rules convincingly enough to unleash the threat of unpleasant arithmetic in those countries. The telltale signs were persistently rising debt-GDP ratios in those countries.

The banks located in the center of the euro area, France and Germany, hold Greek-denominated debt, so a threat of default on Greek government debt threatens the portfolios of those banks in other European countries. Because it is the lender of last resort, now it is the ECB’s business.

France and Germany stay “holier than thou” from beginning to end, and always respect the fiscal limits imposed by the Maastricht Treaty. They thereby acquire the moral authority to lead by example, and the central core of euro-area countries are running budgets that without doubt are balanced in a present-value sense. Therefore, the euro is strong. The banks of the core countries, so the banks in France and Germany are not holding any dodgy bonds issued by governments of dubious peripheral countries that have adopted the euro but that flirt with violating the Maastricht Treaty rules.

In this virtual history, the ECB could play tough and let the Greek government default on its creditors by renegotiating terms of the debt. For the euro, letting the Greek bondholders suffer would actually be therapeutic; it would strengthen the euro by teaching peripheral countries that the ECB means business.”

In Sargent’s models the threat of failure is critical, whether it be for institutions, countries, or individuals, because it is exactly this threat that will shape future behavior and reform.

Relate to Sargent’s comments, one of the more surprising global macro moves since the start of October has been the sharp rally in the EUR-USD going from a low of 1.31 in early October to 1.39 this morning. This is an expedited move of more than 6% in about three weeks. In the highly correlated world of global markets, this expedited move has had an impact. In the same period,

- Brent Crude Oil is up +11.9%;

- West Texas Intermediate Crude Oil is up +21%;

- Copper is up +14.1%;

- SP500 is up +14.1%; and

- Euro Stoxx 50 is up +12.1%

One of our key three themes for Q4 is Correlation Crash. So far, on the expedited move up in the Euro, and down move in the dollar, the crash has been to the upside this quarter. The more accelerated the move to the upside, though, the more increased the risk for an eventual correction to the downside. A risk that heightens every day in our notebooks.

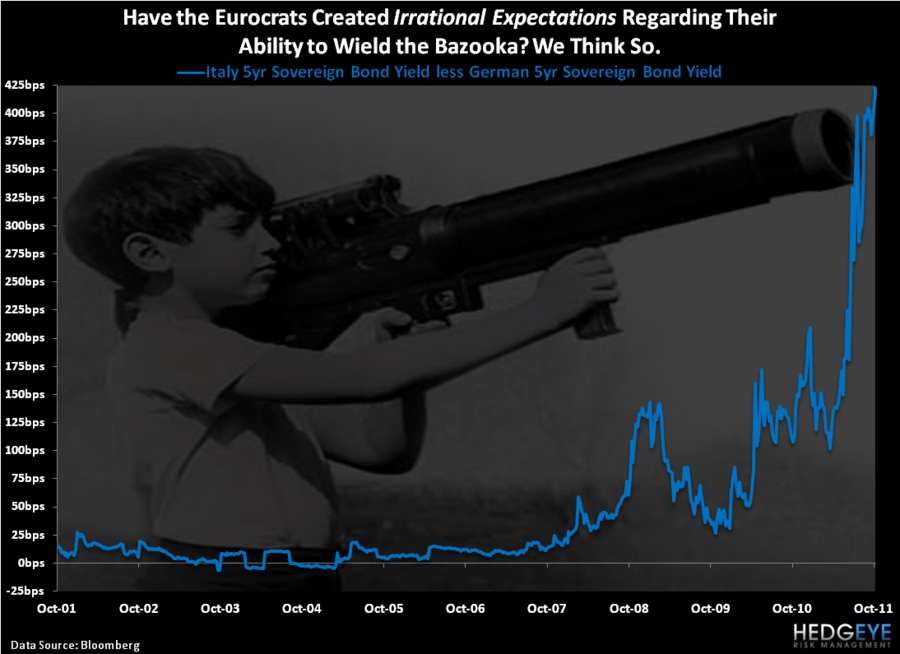

Our view has been that the recent surge in the EUR-USD is a function of both short covering, which obviously builds upon itself, and also Irrational Expectations as it relates to outcomes in Europe. The best fundamental support we can point for our views is in comparing yields on Italian 5-year government bonds versus the comparable duration German bunds. Given this spread is at its widest point in the last decade, the read-through, despite some recent manic moves in global markets, is that the European situation is far from solved.

The theory of rational expectations would suggest that by bailing out Europe in ever-growing increments, market participants will begin to expect ever-growing bailouts, which, over time, should negatively impact the EUR-USD. Further, the continued safety net created by European officials won’t adequately underscore the fiscal sobriety that is ultimately required in Europe for a truly healthy currency. It is akin to bringing a drunk friend water and comfort food every morning after his drinking binge. In doing so, you are not exactly encouraging his or her sobriety.

In the short term, market prices can bring us hope, but they are often “hiding truth’s nakedness.”

Daryl G. Jones

Director of Research