Conclusion: We continue to think that there’s a big duration mismatch here. When the short-term investment factors come to roost just as 40% sales growth numbers are incrementally slowing (still stellar, but what matters is on the margin), we think there will be a much better shot to buy UA lower.

TRADE (3-Weeks or Less):

We expect Q3 results to be in-line with expectations ($0.83E) when the company reports before the open tomorrow, but as we’ve made clear in recent weeks, we’re growing increasingly concerned that the Q4 outlook and initial 2012 commentary could be more cautious than expected. If it’s not, then we’ll be even more concerned, because based on all of our work, it should be.

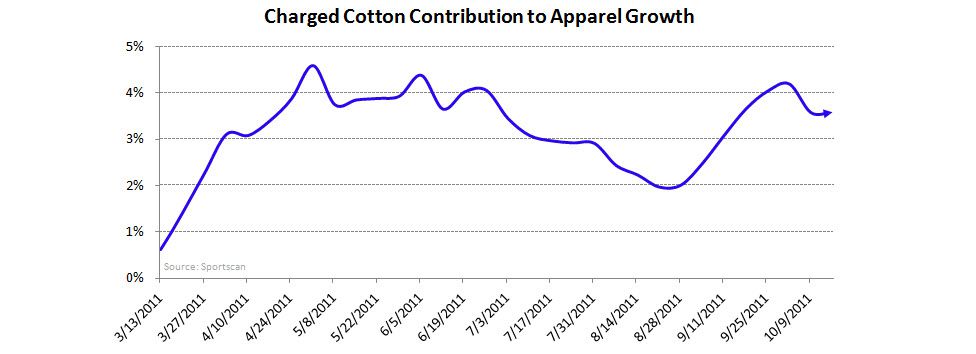

Since 2Q when inventories were up 74% and UA initially discussed ‘fulfillment issues,’ we’ve seen a material management shake-up on the Operations side of the house and ASP growth in the channel that has tracked below peers based on POS data and our research. In fact, based on Sportscan data, UA ASPs have recently declining while the rest of the industry is strongly positive. Coupled with our growing concern that Charged Cotton sales are tracking below expectations, earnings could be headed lower near-term. Footwear has pierced the 1% market share mark recently, which is positive. But we need to see that double before it really starts to matter. UA is a long ways off.

TREND (3-Months or More):

Relative to the +24% revenue growth UA comped last quarter, Q3 is up against a +22% compare after which comps get progressively tougher over the next three quarters. Core apparel growth appears to remain healthy and even footwear is starting to pick up on the margin, but we have been getting increasingly concerned with sales of charged cotton relative to expectations.

Based on an incremental $60mm in sales expected from this new line it should account for roughly 7-8% growth in apparel – industry data suggests its running closer to 3-4%. Before we start citing any trends relative to industry data, we first have to highlight the fact that UA’s DTC, DKS, and TSA account for over 50% of UA’s distribution, which should also be its most productive. That said, we’d have to assume that sales of charged cotton has to be running at ~3x in those channels to be keeping pace with expectations – possible, but greater disparity between the channels then we’d like to see. In addition, ASPs for charged cotton have declined by ~10% over the past month perhaps indicating softer than anticipated sales. For perspective, if the category is tracking at adding an incremental ~6% growth to apparel it is likely to come in closer to $50mm in revs for the year vs. $60-$70mm suggested. That could equate to as much as a 2-4pt deceleration in top-line sales growth expectations in Q4 (consensus at +33%).

If the top-line is indeed starting to slow as we suspect, inventories could take longer to clear and margin pressures will prove to be greater than the company’s original margin adjustment in Q2. Now UA could feasibly pull back on SG&A – like it has in each of the past two quarters – to help hit earnings, but that would increasingly jeopardize the company’s ability to drive top-line growth in 2012. That’s not a trade off we’d like to see. In fact, given the money UA has spent on endorsements over the last year (Michael Phelps, Tom Brady, Lindsay Vonn, Kemba Walker, Derrick Williams (#2 NBA draft – ahead of Kemba at #9) along with retail store growth – it’s not a trade off we’re likely to see.

The punchline is that we’re willing to front UA the benefit of sales growth, OR margin. But certainly not both. Our sense is that the consensus will prove too bullish on one or the other. The Street might give the stock a pass so long as revenue comes in – even though it’s more expensive. For what it’s worth, the biggest pushback we get on a UA short is “I believe that they’ll ultimately grow, and if margins get hurt now, I can live with that. There’s just not much else out there I can own.”

TAIL (3-Years or Less):

We continue to like UA a lot using our TAIL duration – even though we would not buy at current prices. The reality is that this is a great brand, and the company behind it is going through puberty – and is handling the change quite well. But that does not mean that there won’t be operational snafus while the company finds it way in exploring new consumers (women), channels of distribution (DTC), products (footwear), and regions (anything non-US). It’s currently in the midst of a big snafu that will take several quarters to resolve at a minimum.

In addition, a new subtle long-term concern has crept into the equation for us. The reality is that Plank supercharged the footwear organization about 28 months ago, and we’ve really seen nada since then. This is simply taking too long. There are other power brands we’ve seen perennially fail over time in key categories (Columbia, Reebok, Adidas, Timberland). From where we sit, a perennial opportunity either means that a company is mis-executing, or is simply not spending enough money to get it done.

The reality with UA is that Kevin Plank will make the footwear business a real player. We’re pretty convinced there. But the question is whether he’ll have to invest more money in order to do that.

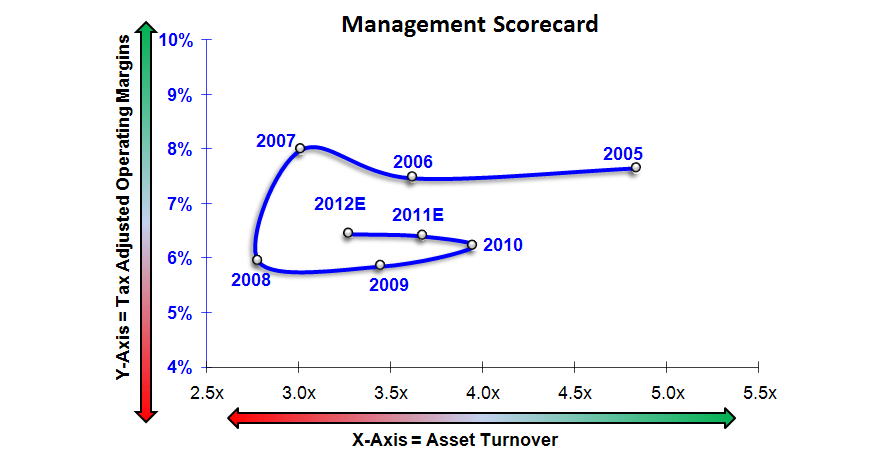

In people’s models, they have sales of 25%+ and margins of 10% that are creeping higher over time. I won’t debate the top line opportunity. But perhaps we should consider if the appropriate margin target here is closer to 8%. That’d definitely put a name trading at 40x+ earnings into a new perspective.

Key Issues re Earnings:

- Top-line trajectory – especially in charged cotton, women’s and footwear

- How much margin UA is giving up to clear inventories

- Is current level of SG&A/Capex spend enough to build a real Footwear business

- Initial 2012 Outlook

Earnings: While we’re in-line with estimates in Q3 ($0.83E), we are coming in below revenue expectations for Q4 at +28.6% vs. +33%E and earnings of $0.56 vs. $0.62E.

Brian McGough & Casey Flavin