This note was originally published at 8am on October 19, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Bullfighting is the only art in which the artist is in danger of death and in which the degree of brilliance in the performance is left to the fighter's honor.”

-Ernest Hemingway

Keith and a few other members of our senior management team are up at the Pop Tech Conference in Camden, Maine, and as a result I’ve been handed the proverbial hockey stick on the Early Look this morning. Given that one of the last major Republican primary debates occurred last night, I wanted to touch upon a topic that we all have an opinion or view on: politics.

The most noteworthy news in the Republican political arena in the last few weeks has been the startling decline of Texas Governor Rick Perry. According to the Real Clear Politics poll aggregate, on September 13th, Perry was at 31.8% in a poll of the major candidates, while Romney was at a distant second with 19.8%. As of yesterday, Perry’s support had declined dramatically to 12.9%. As the public has seen more and more of Perry in televised debates, they have seemingly become less and less comfortable with his ability to be President of the United States.

Last night appears to have been Perry’s best debate showing, though this largely came on the back of a more personal attack on former Massachusetts Governor Mitt Romney related to hiring illegal aliens in his home. Specifically, Perry stated:

“Mitt, you lose all of your standing from my perspective because you hired illegals in your home. And you knew for — about it for a year.”

Perry has actually been effective at raising money in this race and according to recent reports currently has more money on hand than Romney. Money aside, though, Perry appears to have outworn his welcome on the national stage and attacks like the one above are starting to reek of desperation.

Alongside Rick Perry’s rapid decline, the other key surprise in Republican circles has been the rapid ascent of Herman Cain. In the aforementioned poll aggregate from Real Clear Politics, Herman Cain has gone from barely registering, at 4.2%, to now running a close second to Romney with 23.4% support amongst the Republican field. As we wrote about Herman Cain a few weeks ago to our Macro Subscribers in a post titled, “This Isn’t Herman Cain’s First Rodeo (Though It Could Be Rick Perry’s Last):

“In the current race for the Republican nomination, Cain has quickly gone from being a long shot candidate to being considered a serious candidate. This has occurred on the back of a number of straw poll victories, including Illinois, Florida, and at the National Federation of Republican Women.”

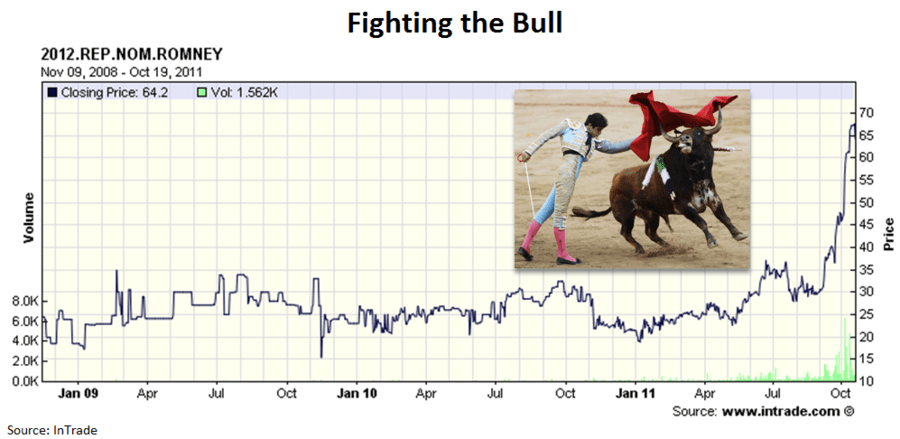

Unfortunately for Cain, it all seems like too little too late. Currently Romney has the fundraising and organizational advantage, as well as the advantage of being a known entity, for better or worse, to voters, so his potential of imploding has limited. The InTrade market for political futures, which we flagged in the Chart of the Day today, reflects as much about Romney in a 65% probability that he will be the nominee.

On the Democratic side, of course, stands the incumbent, President Barack Obama. To say Obama is in a world of hurt, currently, would be an understatement. According to the Real Clear Politics Aggregate, Obama’s approval rating is 43.6% and his disapproval rating 52.0%. His re-election chances are further thwarted by the fact that unemployment stands at north of 9%. No incumbent in the history of the U.S. Presidency has been re-elected with approval and economic numbers this abysmal.

On the positive, President Obama still seems to be moderately well-liked. In fact, despite the extremely negative numbers outlined above, Obama still outpolls all of his potential Republican challengers on a head-to-head basis. Romney is by far the closest, but still trails by 0.6%. So, while Obama is down, he is far from out.

That said, the key missing factor in head-to-head polls is a measure of enthusiasm to vote. According to a recent CNN poll, some 64% of Republicans say they are extremely enthusiastic to vote compared to only 43% of Democrats. If this trend sustains, it will be the Republican nominee by a landslide.

The emerging wild card in this race appears to be the Occupy Wall Street movement. I’ve spent a fair amount of time both researching the movement and visiting their headquarters in Zuccotti Park. The mainstream media, especially CNBC, has certainly been validating this group with exposure, but so far, to me at least, it is very unclear that this group has the organizational skills or money needed to make an impact.

As well, even if the group does appear, so far, to represent largely leftist interests, they do represent a broad discontent with American elites both on Wall Street and in Washington. Despite a lack of real leadership, Occupy Wall Street has flourished geographically. Occupy Wall Street, ultimately, may be a leading indicator that the door remains open for a truly tenable independent candidate to run for President. Who the candidate would be and where he or she would come from, though, remains to be seen.

I do have a recommended skill set for any third party candidate that enters the Presidential ring, which is that of bullfighting. Ironically, a good friend of mine from home, Jason Hale, is taking on the political establishment in Alberta in a race for the Provincial legislature and, as you can see from his bio - http://www.jasonhale.ca/bio - he has 10 years of professional bull fighting experience. Not a bad skill set to have with all the bull in politics these days.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research