A pick up in table revenues last week from the prior week gives us more confidence in the higher end of our HK$24.5-25.5 billion (34-39% YoY growth) forecast for the full month of October. Average daily table revenue increased HK$554 million last week to HK$664 million this past week. The current rate should be considered normal since there were no holidays. The previous week was right after Golden Week which is usually very slow.

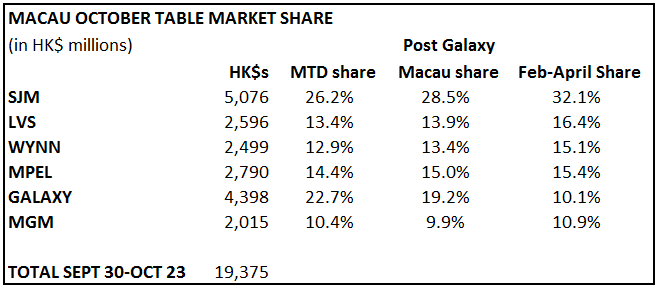

Compared to the previous week, LVS market share took a noticeable dip down to 13.4% which is also below its post Golden Week average. SJM and Galaxy were the sequential market share gainers although SJM (likely hold related) continues to track below its recent monthly trend here in October. MPEL held very well the last few months so its recent average is skewed to the high end. We believe the company is holding normal here in October and a market share around 14.5% is probably a good run rate.

Here are the numbers.