Coming into the quarter our thesis on BWLD was based on accelerating inflation and slowing sales trends. In part we were right to be concerned, but our checks did not suggest that lunch was strong as it was.

That being said, BWLD’s incremental traffic is coming in at lower margins as it is associated with increased discounting. So what is the right answer? Was it a great quarter that the sales headlines suggest or should we raise the red flag on trends that are unsustainable? Headlines are important, but BWLD is now going to experience what the rest of the industry has become so accustomed to: significant inflation. For me, there is enough here from an inflation stand point to merit concern about the sustainability of current trends.

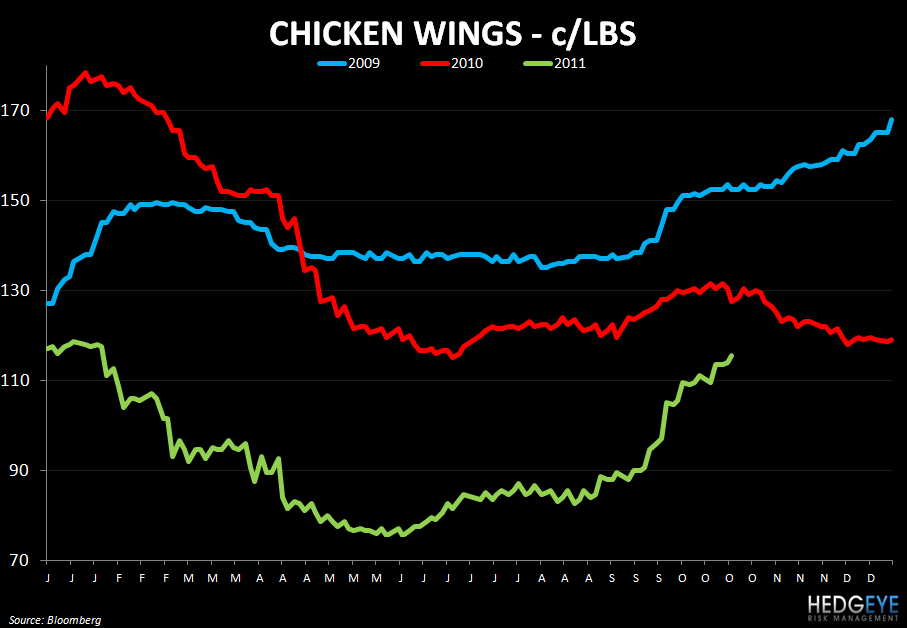

At the very least, the endless wing promotion will never be replicated given the trends in wing prices. The company was right to “give something back to the consumer” given the significant decline in wing prices. What happen to margins in the next six months when wing prices could be up 10-20%? The $3.00 appetizer that is a different story and is a permanent reduction in margin that they can’t get back, unless they raise the price, but then the traffic goes away.

Here are our Top Takeaways from the quarter:

- Food inflation accelerating and discounting adding to COGS. Traffic was driven by $3.00 appetizers and drinks during Happy Hour and the unlimited wings lunch promotion. The appetizers are generating significant traffic at the happy hour time (not sustainable over the long term).

- Unlimited Wings added to cost pressures, but it did end in September so it won't be around for 4Q11. Wing prices are headed higher!

- Same store sales were strong at 5.7% in 3Q compared to 2.6% last year; menu priced increases about 1.4%. Average weekly sales increased by 11.4%, exceeding same store sales percentage by 570 basis points.

- The NBA does not drive customer traffic.

- Menu pricing is running at about 1.5% and most of that would roll off in 1Q12. BWLD is looking at a 2% menu price increase in 2012; they will make a decision on that in November and roll it out with the menu update in the first quarter.

- Tax rate significantly lower in Q3, was 28.1% vs. 32.8% seq.

- Balance sheet and cash flow generation remain strong

- 4Q11 guidance - for the first three weeks of 4Q11 same store sales are strong at 8.3% at company-owned restaurants and 6.7% at franchise locations as compared to same store sales trends for the first four weeks in the prior year of -0.7% 'at company-owned restaurants and -1.7% at franchise locations. If the trends persist for the quarter, it would suggest a significant pick up in 2-year trends. One-time items in the quarter make that unlikely.

- The price of chicken wings for the first two months of the fourth quarter is averaging about $1.39 per pound. This compares to last year's average price of $1.49.

- BWLD boneless wings contract which was due to expire on March of 2012 has been extended through March of 2013 with a very small price increase beginning in April of 2012; the remainder of the commodity basket in 4Q11 is contracted at an increase of about 3.5% YoY.

- In 4Q11 BWLD expects to leverage labor costs and operating expenses with higher same-store sales trends.

- The 19 new store openings will be the highest pre-opening cost quarter of the year.

- Wing prices are moving up.

Howard Penney

Managing Director

Rory Green

Analyst