THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP - October 20, 2011

Exotic TAILS notwithstanding (18 tigers and 8 bears on the loose in Ohio yesterday), we know this market’s long-term TAIL is broken (1266) – so, all we have to do now is continue to manage risk around the immediate (TRADE) to intermediate-term (TREND) range. As we look at today’s set up for the S&P 500, the range is 20 points or -0.73% downside to 1201 and 0.92% upside to 1221.

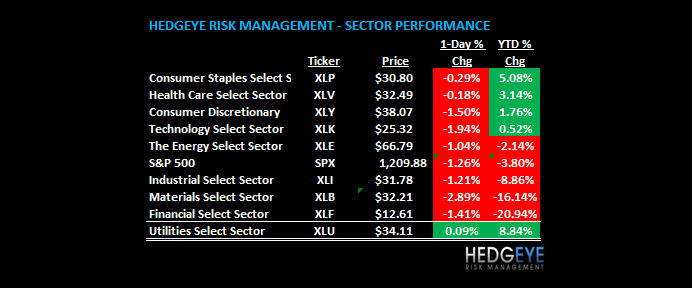

SECTOR AND GLOBAL PERFORMANCE

From an immediate-term TRADE perspective, today’s selloff doesn’t change the fact that all 9 sectors (and the SP500 itself) remain bullish. This is healthy until it isn’t. A close below 1201 tomorrow would change this setup. Holding above it would be bullish.

Another improving TREND (intermediate-term) is that 4 of 9 Sectors are now bullish on that duration: Consumer Discretionary (XLY), Utilities (XLK), Tech (XLK), and Consumer Staples (XLP). We like those Sectors in that order. Consumer Discretionary will be the most direct beneficiary of a Strong Dollar as it will continue to “Deflate The Inflation.”

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -1354 (-3428)

- VOLUME: NYSE 964.04 (-11.17%)

- VIX: 34.44 +9.13% YTD PERFORMANCE: +94.03%

- SPX PUT/CALL RATIO: 1.78 from 1.64 (+8.80%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 39.13

- 3-MONTH T-BILL YIELD: 0.03%

- 10-Year: 2.18 from 2.19

- YIELD CURVE: 1.90 from 1.91

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30 a.m.: Jobless claims, est. 400k, prior 404k

- 9:45 a.m.: Bloomberg Consumer Comfort, prior (-50.8)

- 10 a.m.: Leading indicators, est. 0.2%, prior (-17.5)

- 10 a.m.: Existing home sales, est. 4.91m, down 2.5%

- 10 a.m.: Freddie Mac mortgage rates

- 10:15 a.m.: Fed’s Bullard speaks in St. Louis

- 10:30 a.m.: EIA Natural Gas storage

- Noon: Fed’s Lockhart moderates panel on economy in Atlanta

- 12:50 p.m.: Fed’s Pianalto speaks in Toledo, Ohio

- 1 p.m.: U.S. to sell $7b 30-yr TIPS (reopen)

- 2 p.m.: Treasury’s Brainard testifies to U.S. Senate committee

- 6 p.m.: Fed’s Tarullo speaks at Columbia in NYC

- 7:45 p.m.: Fed’s Kocherlakota speaks on economic education in Minneapolis

WHAT TO WATCH:

- Yahoo! isn’t necessarily up for sale, co-founder Jerry Yang said; Alibaba CEO reiterates he’s interested in buying the company

- Groupon said to be in talks to sell shares in IPO valuing co. at ~$12b

- Sales of existing U.S. homes probably declined 2.5% to 4.91m annual rate in Sept., economists’ forecast ahead of today’s report

- SEC said to be trying to determine if SAC Capital used insider information to profit from J&J’s 2009 takeover of Cougar Biotechnology, WSJ says

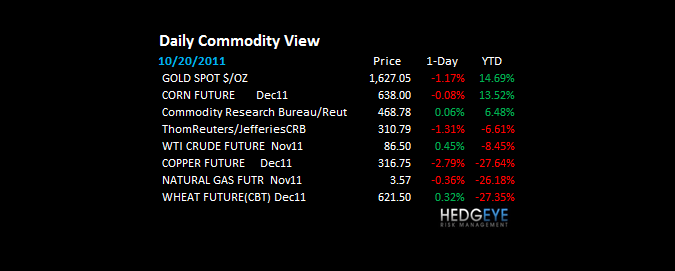

COMMODITY/GROWTH EXPECTATION

COMMODITIES – we’ve called for the Correlation Crash to continue and that’s plainly obvious now with Gold chasing Copper (albeit with a lower beta); both remain broken; Copper down -2.9% this morning is immediate-term TRADE oversold, but has moved back into the down -30% since July zone; not good – neither is Gold’s TREND resistance ($1685) fortifying itself

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- Pamela Anderson Champions Palladium as Gold Prices Soar: Retail

- Iron’s Worst Rout in 15 Months May Deepen as China Slows

- Silver Bear Market Seen Ending on Europe Crisis: Commodities

- China Love of U.S. Cherries Fuels Cool-Cargo Boom: Freight

- Gold Falls to Two-Week Low as Gains in the Dollar Curb Demand

- EU Targets Commodities, High-Frequency Trading in Market Law

- Coal Gridlock Heralds Two-Year High Asia Premium: Energy Markets

- Zambia Investors Say Copper Boom to Extend as Sata No Castro

- Copper Drops for a Fourth Day on European Debt-Crisis Concern

- Chinese Aluminum Supply Jump 30% in 3 Weeks, Signaling Slump

- Oil Drops a Second Day on Europe Outlook; Brent Premium Widens

- Rio Tinto Makes $567 Million Offer for Hathor to Trump Cameco

- Gold Prices May Extend Losses on Bear Flag: Technical Analysis

- EU Seeks Curbs on Commodity Derivatives, High-Frequency Trading

- Freeport Says Grasberg Mine Operating at Two-Thirds Capacity

- Agnico Plunges After Halting Canadian Gold Mine on Flooding

- Commodities trading suffers as French banks curb credit

- Thailand, Indonesia ‘Closely Monitoring’ Rubber Decline

- Oil Rebounds on Speculation EU Agreement Will Help Fight Crisis

CURRENCIES

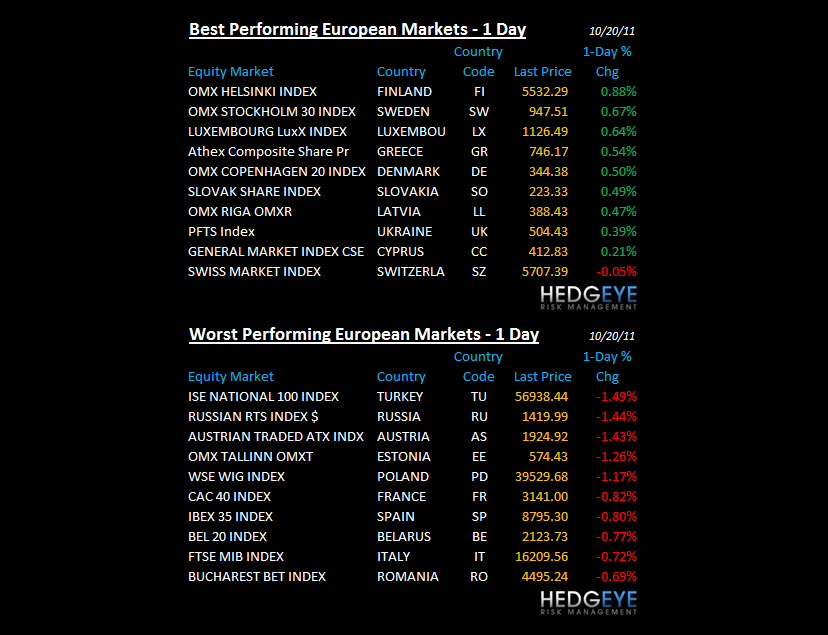

EUROPEAN MARKETS

RUSSIA – consistently flashing negative divergences vs the focus European markets (DAX, CAC, Greece, etc) this week; this tells me that A) I’m right on the USD TREND and B) right on Oil remaining a bearish TAIL/TREND; Petrodollars drive the RTSI and its crashing – down -34% since May.

ASIAN MARKETS

ASIA – the Hang Seng was down -1.8% again last night (China down -1.9% testing new lows) and the move was consequential as the only remaining line of support (18215) was snapped again on the downside. As the world focuses on 1 thing (Europe) you tend to get paid to focus on everything else that doesn’t cease to exist – Asian Growth Slowing is a big one.

MIDDLE EAST

The Hedgeye Macro Team

Howard Penney

Managing Director