Positions in Europe: Short EUR-USD (FXE)

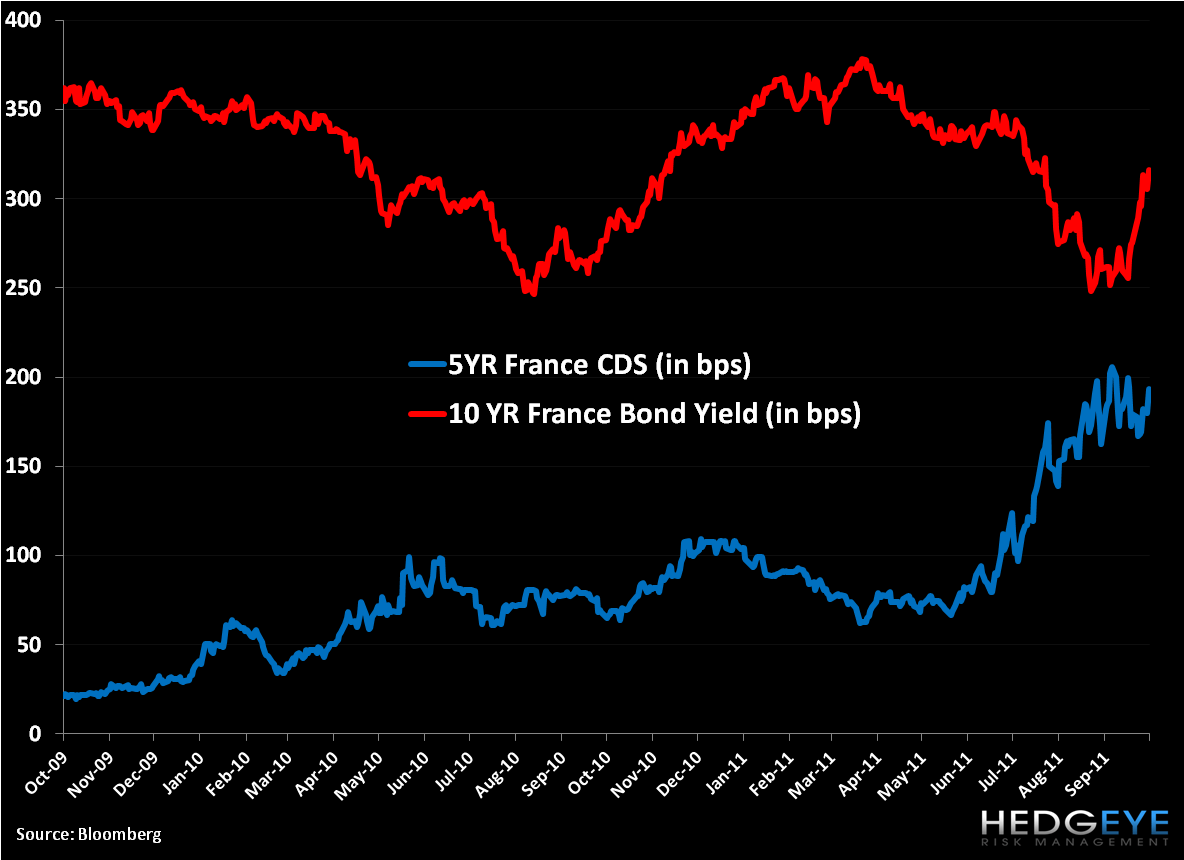

France’s credit rating is going to get downgraded – now the question is when, and what becomes of the EFSF? The three main ratings agencies (Moody’s, S&P, and Fitch) are classic lagging indicators, however Moody’s announcement to downgrade France’s AAA credit outlook from stable to negative is having significant follow-through market implications. In the charts below we show the spread between German bunds and 10YR French bond yields, which is hitting an all-time wide (since the Euro was introduced) of 110bps today. Additionally, French CDS is trending up and to the right (currently at 193bps) and the French 10YR bond yield has gained 57bps in October alone.

The rise in yields and risk increases France’s debt servicing costs at a juncture in which its outstanding sovereign debt is elevated and its banks look to require more funding. On the French sovereign side, €122 Billion in debt (Principal and Interest) is due into year-end and €259 Billion will be due in 2012 on a €1.9 Trillion economy. That compares to year-end maturing debt figures of €64 Billion in Germany (on a €2.5 Trillion economy) and Italy at €68B on a €1.6 Trillion economy.

On the banking side, the European Banking Authority is considering increasing the core Tier 1 capital ratio level to 9% in a third round of tests (from 5%). If this is the case, Credit Suisse estimates that France’s four largest banks will need to raise €43 Billion, or 2.2% of France’s GDP. If state recapitalization was mandated this would likely push France’s 2011 estimated Debt as a % of GDP to 88.4% from 86.2%, and add to that the upward pressures from the government’s guarantees of Dexia’s losses. As Reinhart and Rogoff outline in their book “This Time is Different” a 90% level of debt (as a % of GDP) is prohibitive to economic expansion. In our work in conjunction with our Financials Team we’ve also shown the exposure risks of European banks to the PIIGS. As it relates to French banks, we’ve noted in particular BNP Paribas’ massive Core Tier 1 capital exposure to sovereign debt and commercial loans of 194%.

Politically, Sarkozy continues to lose support, as high unemployment, at 9.2%, or 22.8% among youth, create dissent and the country remains more hostage to domestic demand (unlike Germany) to grow.

Should a ratings agency cut France’s credit rating, which we think is highly probably—although we wouldn’t rule out Eurocrat measures to prevent such a move (through influence) or to act to create its own ratings agency—it would throw a wrench into the EFSF, 20% of the collateral for which France is on the hook for, the second largest contributor behind Germany at 27%. Essentially, the EFSF would be back at square one with the likely outcome that the ECB would be forced to take on a big role to bailout/provide the bazooka for Europe.

Europe’s sovereign and banking crisis seems to live one day at a time. However, we hope you can get ahead of the risk that France’s credit rating deteriorates from here.

Matthew Hedrick

Senior Analyst