THE HEDGEYE BREAKFAST MONITOR

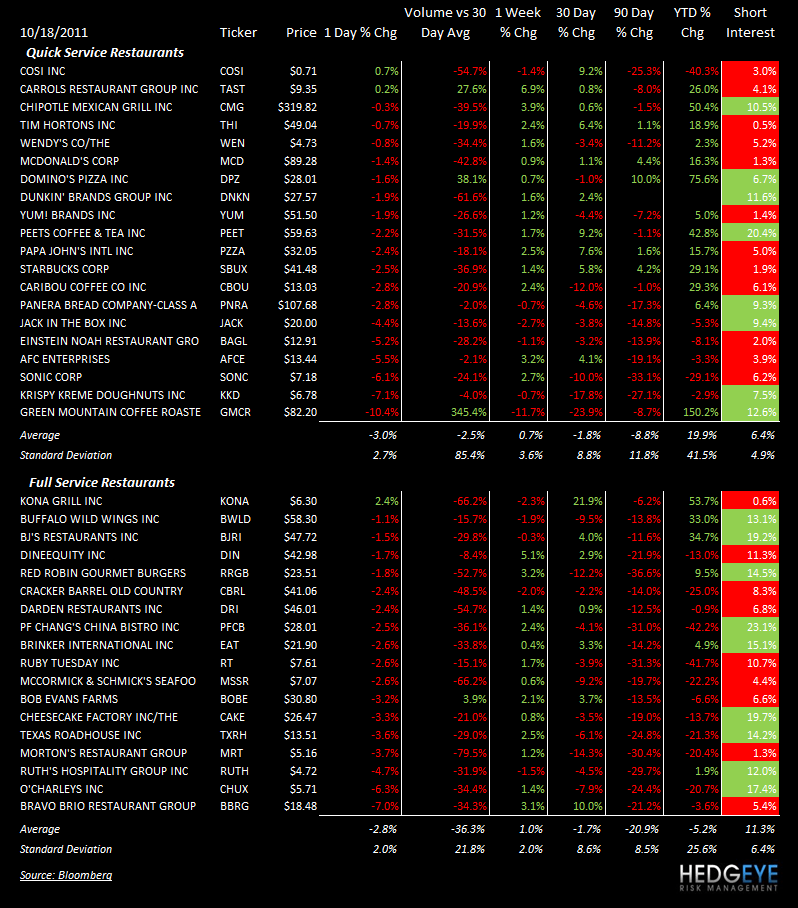

GENERAL CALLOUT – IS DNKN NEXT? CMG?

GMCR’s valuation bubble has been deflating since we made the “coffee bubble” call in our DNKN Black Book in July. Is DNKN next? We estimate that the company needs to sell just under two boxes of K-Cups per day per store (point of distribution) to add 1% to the comp. We stopped by a store on 6thavenue yesterday and were disappointed to see no K-Cups on sale! CMG is the other obvious candidate for correction from a valuation perspective. The company’s unit economics have remained strong with unit and comp growth offsetting commodity and labor headwinds. The new concept, as it grows, could become a distraction, however.

MACRO NOTES

Commodities

Coffee is falling for the second straight day in New York after the top cooperative in Brazil predicted a “great” crop quality in the country. Brazil is the world’s largest coffee grower.

SUBSECTOR PERFORMANCE

QUICK SERVICE

GMCR: Green Mountain Coffee Roasters traded down yesterday after Greenlight Capital’s David Einhorn made negative comments about the business at a conference. Einhorn took issue with the “looming” patent issue on K-Cups (expiration of the patent) and the resulting loss of the “monopoly price”. All in all, we saw nothing new in Einhorn’s comments but the impact on the stock was obviously severe.

DPZ: Domino’s Pizza reported 3Q Adjusted EPS of $0.35 versus the street at $0.33. Domestic same-store sales were +3% versus StreetAccount consensus of +2.7%. Company same-store sales were 4.2% versus 2.2% expectations.

CASUAL DINING

PFCB: P.F. Chang’s Bistro was downgraded to “Underweight” from “Neutral” at Piper Jaffray.

PFCB: P.F. Chang’s Bistro announced that it has signed an exclusive development and licensing agreement with Alsea, S.A.B de C.V., the leading quick service restaurant restaurant, coffee shop and casual dining operator in Latin America, to develop Pei Wei Asian Diner throughout Mexico.

CAKE: Cheesecake Factory was upgraded to “Overweight” from “Neutral” at Piper Jaffray.

Howard Penney

Managing Director

Rory Green

Analyst