Conclusions: Broadly speaking cash on corporate balance sheet is up, though not meaningfully since 2008. Moreover, with low risk-free rate of return, cash balances are actually a drag on earnings growth.

Commonly, the health of corporate balance sheets is cited as a reason to be supportive of higher stock prices. The theory is that as corporations build cash on their balance sheets it is both a sign of operational health and also provides ammunition to make acquisitions. Therefore as balance sheets get healthier, there should be an underlying bid to equities due to increased M&A prospects.

We spent the weekend looking at the progression of corporate balance sheets for the 50 largest market capitalized companies in the SP500 as a proxy for the health of corporate balance sheets more generally. Collectively, this group of companies is just over 50% of the total market capitalization of the SP500, so clearly a reasonable proxy for corporate America.

In this analysis, we also removed the financials, which for the largest 50 companies in the SP500 includes Citigroup, Goldman Sachs, Wells Fargo, J.P. Morgan and Bank of America. The point is obviously not to understate the relevance of the balance sheets of banks, but rather to simplify the analysis and focus on operational cash and debt versus trying to decipher the balance sheets of the major banks and the nature of their cash and debt obligations.

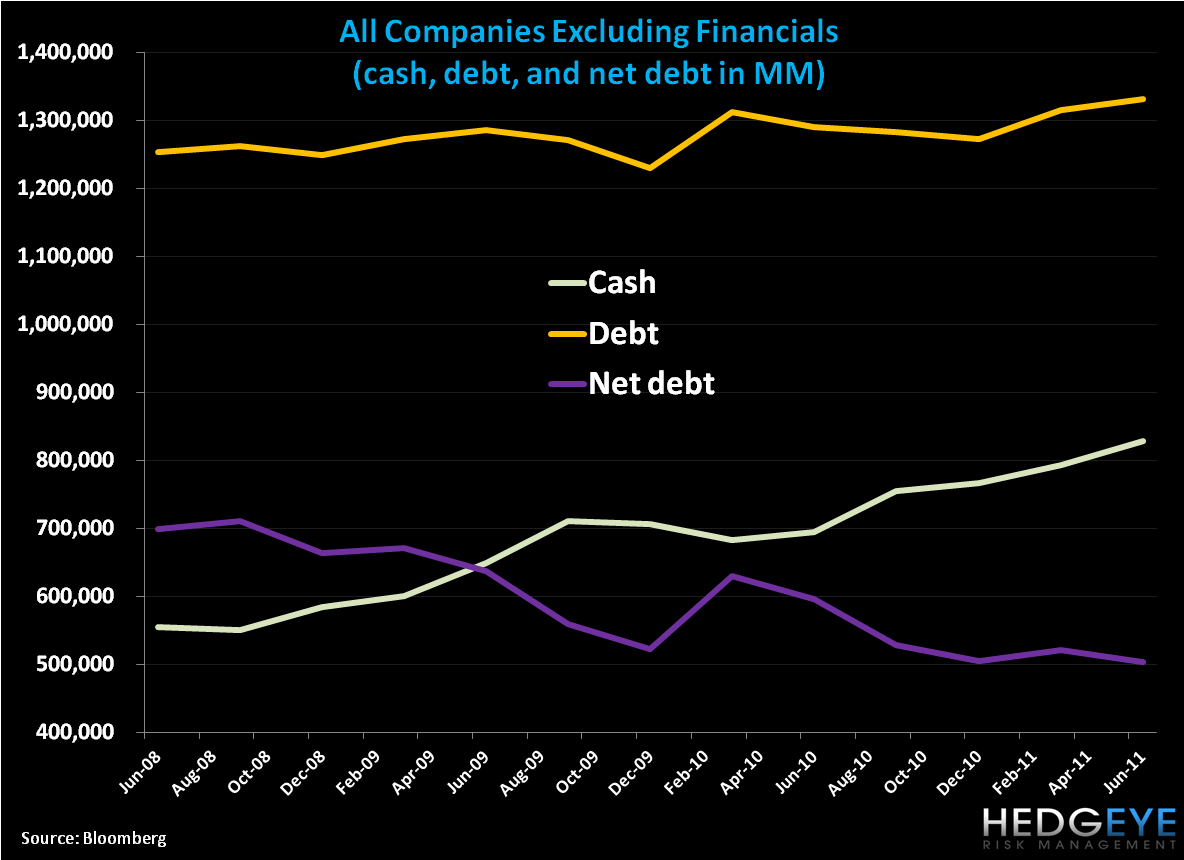

In the chart below, we show the quarterly cash (short term investments and cash equivalents), debt (short and long term), and net debt balances of the largest 50 companies in the SP500 by market capitalization going back quarterly from June 30th2011 to June 30th, 2008. In that time period, cash has grown by $273 billion, or +49%. Over the same period, debt grew by +$78 billion. In aggregate, corporate balance sheets, on this basis, have seen meaningful improvement since June 30th, 2008 as net debt has declined by almost -$200 billion over the period.

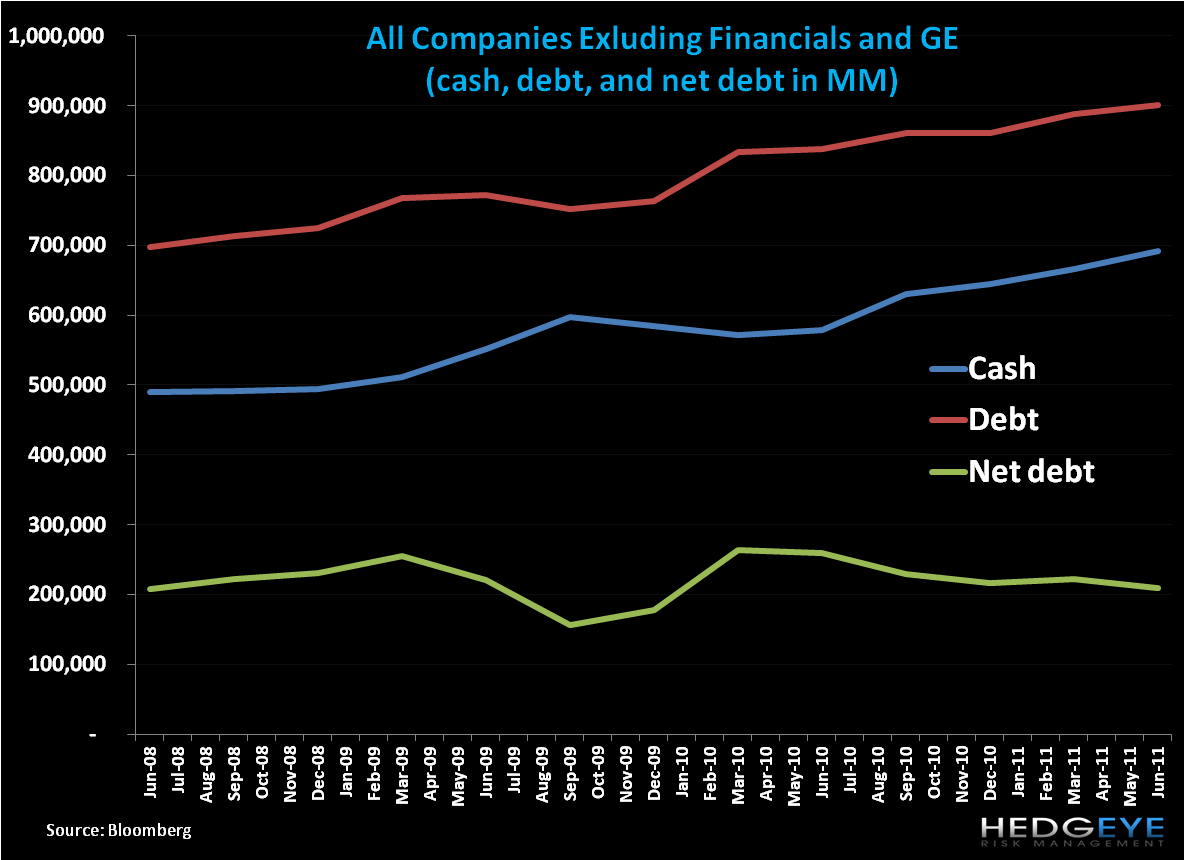

Interestingly, if we back out General Electric from this analysis, the growth of cash on corporate balance is less positive. As the chart below shows, after removing GE, cash grew by over +$200BN from Q2 2008 to Q3 2011. At the same time, debt grew by a comparable amount. So on the basis of net debt as a proxy for health of the balance sheet, the largest 50 companies in the SP500, excluding the banks and GE, look almost exactly the same today as they did three years ago.

None of this is to say that corporate balance sheets are in poor health. In fact, based on longer term historical studies, corporate balance sheets are quite healthy. A recent study by the Wall Street Journal highlighted that:

“Cash accounted for 7.1% of all company assets, everything from buildings to bonds, the highest level since 1963.”

That said, it is just not clear, that cash on balance sheets should be considered a positive catalyst for stock prices.

Conversely, it is somewhat disconcerting that cash is growing and not being invested, especially given the low interest rates that cash and short term investments are earning. In Q3 2008, the 90-day money market rate was roughly 3% versus roughly 0.4% now. As a result of declining rates, the change in interest income on an annualized basis from Q2 2008 to Q2 2011 was a decline more than -$13 billion from $16 billion to just over $3 billion. So, while cash balances growing are a positive, the decline in the return on cash has more than offset that positive.

Finally, in the two charts below we show the most improved balance sheet over the last three years and the worst performing balance sheet, all on the basis of growth of net debt. As mentioned above, GE appears to have a dramatically improved balance sheet from (disclaimer: we have not done a deep dive on GE) three years ago, while on the negative side, Exxon Mobil has seen its balance sheet decline over that period going from $30.1BN in net cast to $6.5BN in net debt.

Clearly, corporate balance sheets in the U.S. are in decent shape, but we would caution against using that as a market catalyst. Arguably, as well, it is actually a drag on earnings growth as long as cash sits on the balance sheet unproductively earning low rates of return. In fact, by letting cash sit and earn low rates of return, corporations are actually signaling that they do not see meaningful growth opportunities in the future.

Cash is king . . . if it earns a return.

Daryl G. Jones

Director of Research