The issues with employment, housing and policy-induced stock market volatility continue to weigh on economic growth and our overall prosperity. Consumer confidence also is a problem, as current levels of confidence indices are more supportive of a recessionary environment than of recovery. Retail sales figures released today certainly imply a healthier consumer in September than the confidence numbers do. If more credence is lent to the sentiment picture, it would seem appropriate to assume that a slowing in spending from here is likely, which would support our bearish view on the economy. If expectations are what drives consumer spending, the negative trends in consumer expectations do not bode well.

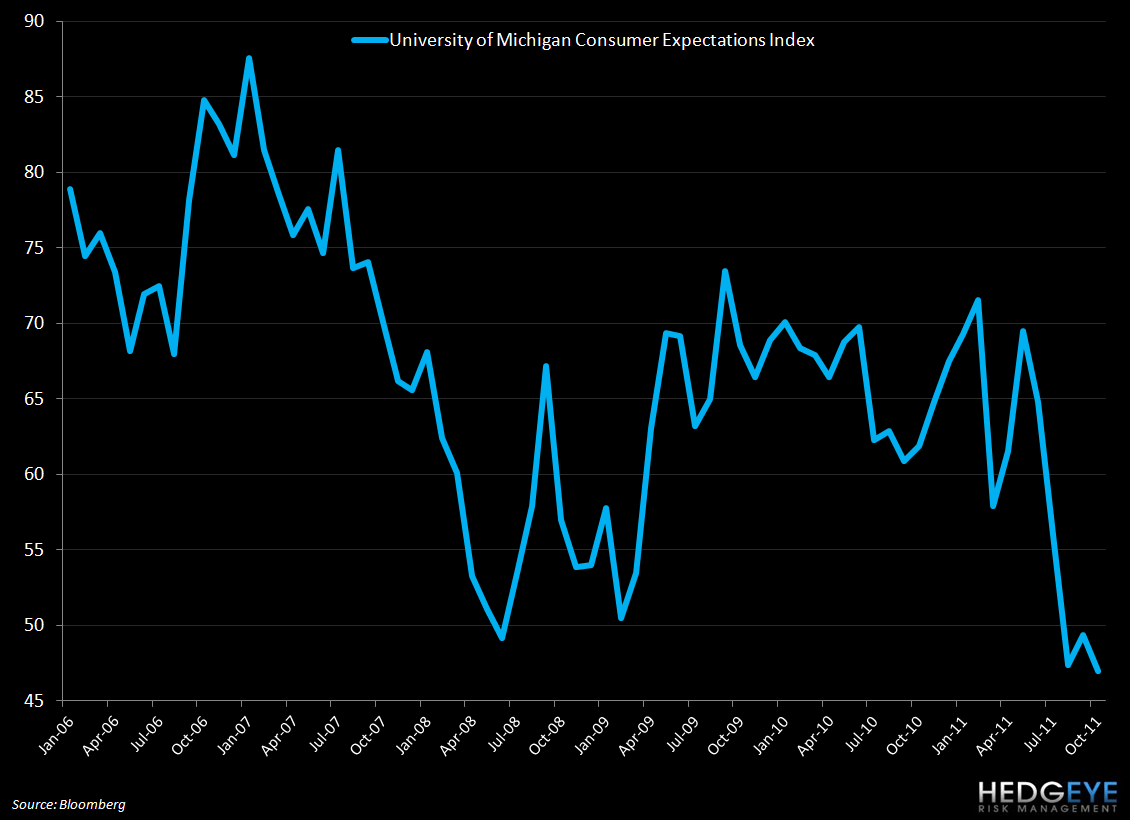

Today, the preliminary University of Michigan consumer sentiment index declined 1.9 points, with consumer expectations leading the way day (although both components declined). The index came in at 57.5, compared with September’s 59.4.

As we have said repeatedly, the economic drivers of confidence remain very mixed, and we do not expect significant improvement any time soon. The most pressing concern is continued labor market weakness, specifically the large number of discouraged workers that remain out of the labor force. This is evident in the chart below, showing the labor force participation rate declining precipitously throughout recent years. This week, jobless claims came in this at 404K (backing out the revision to last week's data, claims moved higher by 3K).

Our Financials Team continues to point out that the spread between claims and the S&P remains as wide as it's ever been in the last three years. If claims move to the level implied by the S&P that would be roughly 475k. Our Financials Team’s model indicates that a 475k claims level would be consistent with 0% GDP growth.

On the positive side, debt levels have been reduced substantially over the past two years and there are small signs that credit is very gradually becoming more available. This, along with the help of the federal government, is helping the outlook for spending on the margin.

It appears from the data that consumer spending finished 3Q11 on a positive note. The Commerce Department reported that retail sales rose 1.1% in September, its largest monthly gain since February 2011. While autos provided a boost to the overall figure, there was strength across the board, as the increase beat the Bloomberg consensus by 0.4%. Non-auto retail sales rose 0.6%, a modest acceleration from August’s 0.5% (was revised up from 0.1% last month).

Despite the disappointing consumer confidence levels, retail sales data suggests that consumers are finding a way to finance consumption despite the weak job and income headwinds. If savings are being sacrificed and this is a significant reason behind the strong numbers this month that clearly doesn’t bode well for the continuation of the improving consumption picture that we saw last month. In the end, the data is prolonging an environment of uncertainty.

On the earnings front, it’s been mixed thus far. Two companies that we paid close attention to from a consumer standpoint were PEP and SWY. Pepsico reported a low quality quarter and left its full-year EPS guidance unchanged although its expected FX benefit was lowered from 2% to 1%. SWY reported better-than-expected Q3 results vs low expectations. Industry volumes are under pressure, however, and the outlook is cautious due to the secular headwinds facing the industry. Grocers have been pricing aggressively to protect margins in the face of high inflation.

All in all, expectations are mounting for a “bazooka” bailout from Europe which, if less substantial than the market is hoping for, could be a catalyst to the downside. Hope is not, after all, an investment process.

Howard Penney

Managing Director