This note was originally published at 8am on October 11, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Psychologist Irving Janis coined the term groupthink to describe ‘expert’ behavior.”

-Dan Gardner (“Future Babble”, page 109)

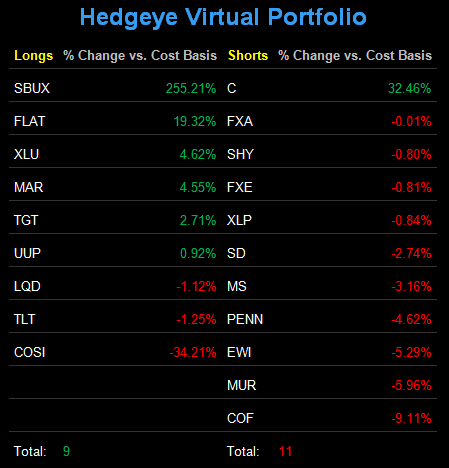

When our head of Healthcare Research, Tom Tobin, and I were working at what used to be called Dawson-Samberg (long-time hedge fund that split up) over a decade ago, we were learning what Wall Street “consensus” was by doing. Today, we continue to develop processes to quantify it. This, like any good process, takes flexibility, testing, and time.

Within the context of a long time, “groupthink” is a relatively new phenomena. Irving Janis’ original groupthink research at Yale University didn’t occur until the early 1970s. Since then, it’s been very helpful in analyzing both the military and economic policy mistakes of central planners.

Groupthink can also be applied to analyzing the behavior of short sellers – as in hedge funds – and how and when they make decisions. To be, or not to be hedged – remains the question. With the most obvious of groupthink occurring at the most painful ends of what we call the immediate-term TRADE range.

While it’s hard to believe that Old Wall Street missed making the 2011 Growth Slowing call (after having had the opportunity to review their 2008 forecasting mistakes), it’s even harder to believe that the SP500 can put on a 116 point (+10.7%) move in less than a week and still have so many hedge fund guys trafficking in the same high-short interest hedges.

Believe both.

I remember listening to a friend explain to me that John Paulson was “reducing his exposure to 62% net long” (with leverage) sometime back in early Q3 of 2011 and thinking to myself, that’s not a hedge fund – hedge funds hedge.

But that was just silly young me saying what any prudent Risk Manager should have said about Paulson’s positioning, given my bearish intermediate-term Global Macro view.

After I said it publically on CNBC again in July, I had people do the proactively predictable and tell me I was being whatever they call someone when they are confident in their view. After all, John Paulson is smart. But, then again, so is my team. Market opinions aren’t personal. Neither are the tail risks associated with redemptions and liquidations. It’s all part of the game.

Back to the Global Macro Grind…

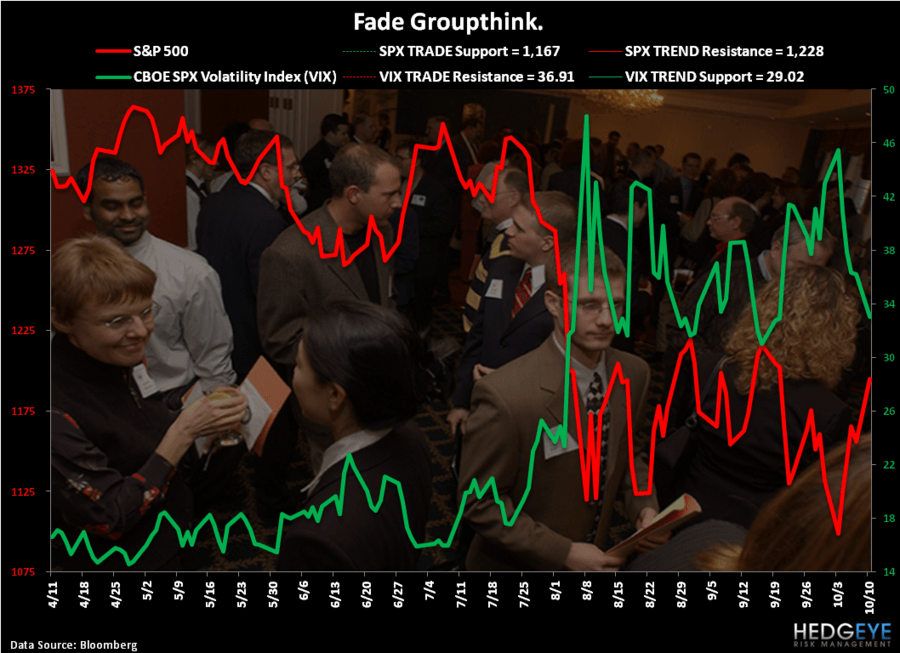

With the Short Covering Opportunity and the Eurocrat Bazooka Squeezes out of the way, now we can get back to managing risk around newly developed ranges. In the last week, a very important signal has developed on my immediate-term TRADE duration that supports that claim – the SP500 and Volatility have recovered their respective TRADE lines of support and resistance.

What does that mean? First, let’s look at the levels.

- SP500 TRADE line support = 1167 and TREND line resistance = 1228

- Volatility (VIX) TRADE line resistance = 36.91 and TREND line support = 29.02

Did I just confuse the matter by throwing in another duration (the intermediate-term TREND)? Yes, I did. And that’s the risk management point that we continue to beat the drums on within our process – you have to be able to be Duration Agnostic.

What that means is that bullish is as bullish does for US Equities provided that the TRADE line of 1167 holds. But only to a point (the TREND line of 1228). And with a deep respect for that point, we also have to wake up every morning Embracing Uncertainty – because the minute that 1167 breaks again, we’ll need to be focused on putting our crash helmets back on.

This Globally Interconnected Game of Risk can get even more confusing if you don’t blow out your model to absorbing the uncertainty associated with correlation risks across global markets. Whether they be countries, currencies, or commodities, they’re all there – and they affect Groupthink’s Behavior, big time.

We call that being Multi-Factor in our risk management approach.

So, with a multi-factor (countries, currencies, commodities, etc.), multi-duration (TRADE, TREND, and TAIL) Global Macro model in hand, what do I see going on out there this morning?

Here’s my Top 6:

- SP500 bullish TRADE; bearish TREND

- VIX bearish TRADE; bullish TREND

- Hang Seng in a Bearish Formation (bearish across all 3 durations, TRADE/TREND/TAIL)

- Copper and Oil in Bearish Formations

- Euro/USD cross in a Bearish Formation with TRADE and TAIL lines of resistance at $1.36 and $1.39, respectively

- German DAX bullish TRADE; bearish TREND

I have a lot more than 6 factors in my model – but these are the ones ringing with the most Correlation Risk right here and now. These are my front-runners for managing Global Macro risk.

I have a tremendous amount of confidence in both my risk management model and the 41 people on my team that support its inputs. This confidence is a culture – we are not too proud to change the model’s parameters or throw away the wrong assumptions when they are not working. As prices, volatilities, and volumes change, we do.

Embracing Uncertainty is the furthest thing from what Old Wall Street wants right now. The only certainty I have about that is that Groupthink’s Behavior is going to continue to have performance problems as these markets churn.

My immediate-term support and resistance ranges for Gold, Oil, the German DAX, and the SP500 are now $1640-1679, $80.90-86.41, 5571-5921, and 1167-1198, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer