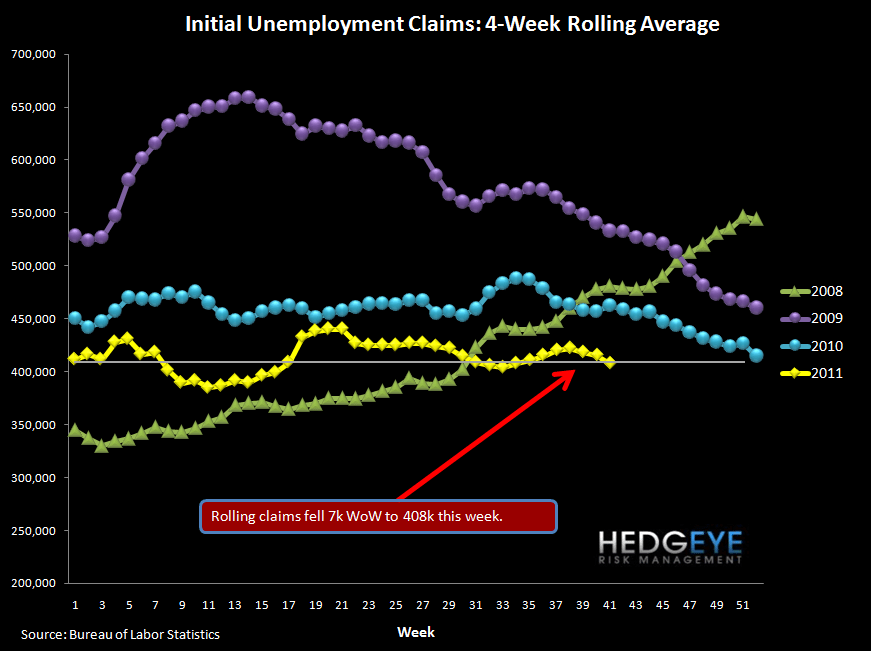

Jobless claims came in this week at 404k. Backing out the revision to last week's data, claims moved higher by 3k. Looking at the non-seasonally-adjusted series, there was an increase of 66k claims week over week - an apparently large number but not atypical for the week following quarter-end.

We are struck by the fact that the supposedly "technical" factors that caused the sudden decline in claims a month ago have not reversed. Distortions around quarter-end are typical, and the decrease didn't show up as an aberration in the non-seasonally-adjusted data. Meanwhile, the spread between claims and the S&P remains as wide as it's ever been in the last three years. If claims move to the level implied by the S&P, that would be roughly 475k. For reference, a 475k claims level would be consistent with 0% or lower GDP growth.

Bigger picture, monetary stimulus has had a tight correlation to improving initial claims. The lack of further easing from the Fed means that this tailwind is now gone. With further fiscal stimulus also off the table, we expect that initial claims will reflect growing weakness.

2-10 Spread

The 2-10 spread widened by 29 bps versus the prior week as the market rallied.

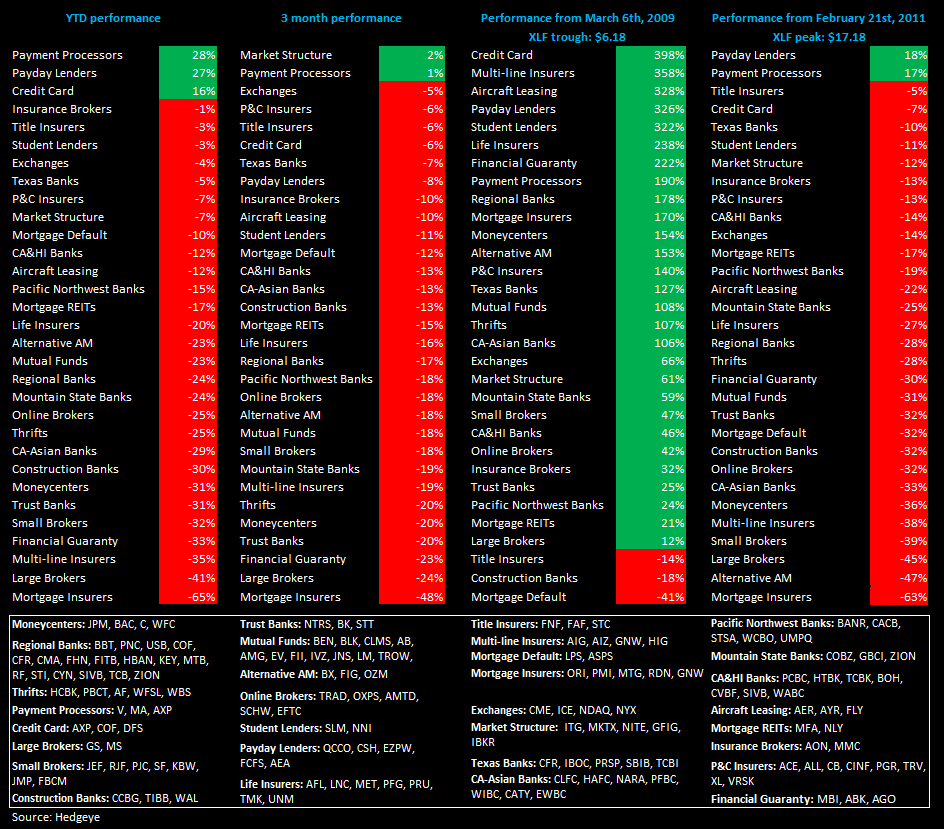

Subsector Performance

The table below shows the performance of financial subsectors over various durations.

Joshua Steiner, CFA

Allison Kaptur

Having trouble viewing the charts in this email? Please click the link below to view in your browser.