THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

Commodities

Upwardly revised grain stockpiles estimates in the US are driving corn and wheat prices lower this morning.

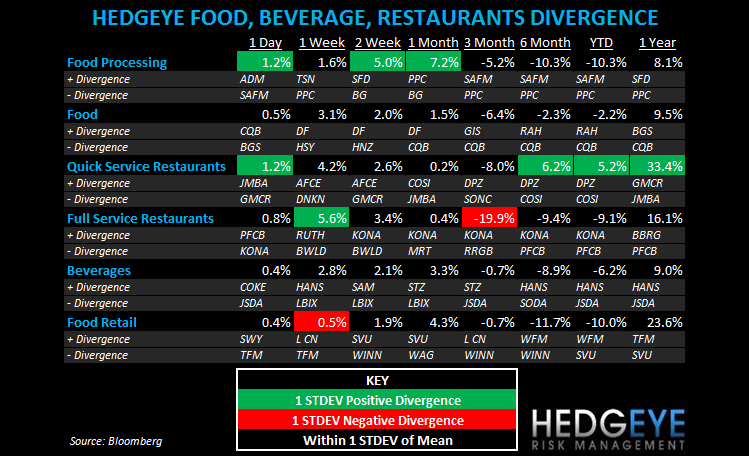

SUBSECTOR PERFORMANCE

Food processor stocks were boosted by corn’s slide yesterday with TSN the biggest beneficiary.

QUICK SERVICE

SBUX: Starbucks announced yesterday the availability of its Via Ready Brew in House Blend and Breakfast Blend at select grocery stores across the US.

SBUX: According to the blog “Starbucks Gossip”, “The super big announcement that is going down is about whole bean coffee and how the categories are going to change. Starbucks is going to offer three different categories -- "blonde," mild and dark roasts. There will now be two new coffees offered that are milder than Breakfast Blend. I believe the new category system and new coffee offerings are going to start late this year with an official launch in January 2012.”

HEDGEYE - While this may be gossip, it makes sense now that SBUX controls its distribution channel for the company to continue with new product innovation.

SBUX: In an interview yesterday, CEO Howard Schultz says Brazil and China are emerging markets where Starbucks has too few stores.

PZZA: GE Capital, Franchise Finance recently completed a $9.5 million transaction with BAJCO Group, a Papa John’s Pizza franchisee, for the refinancing of existing debt. Funding was provided through GE Capital’s bank affiliate, GE Capital Financial Inc.

GMCR traded down on significantly higher volume during yesterday’s trading.

CASUAL DINING

DIN: Dine Equity has announced the sale of 17 Applebee’s from which it expects net proceeds of $15.9m. DIN has sold 259 restaurants since buying Applebee’s in November 2007.

DRI: Darden is to add Eddie V’s Prime Seafood and Wildfish Seafood Grille to its specialty restaurant group, according to the WSJ. The acquisition of 11 locations cost Darden $59M in cash and the deal will, according to the company, be neutral to its fiscal earnings.

BWLD: Buffalo Wild Wings was cut to “Neutral” at Dougherty & Co. The twelve-month price target is $63.

MRT traded higher yesterday on strong volume.

Howard Penney

Managing Director

Rory Green

Analyst