Commodities rebounded over the last week, with a few exceptions, as the dollar declined.

STOCK TAKEAWAYS

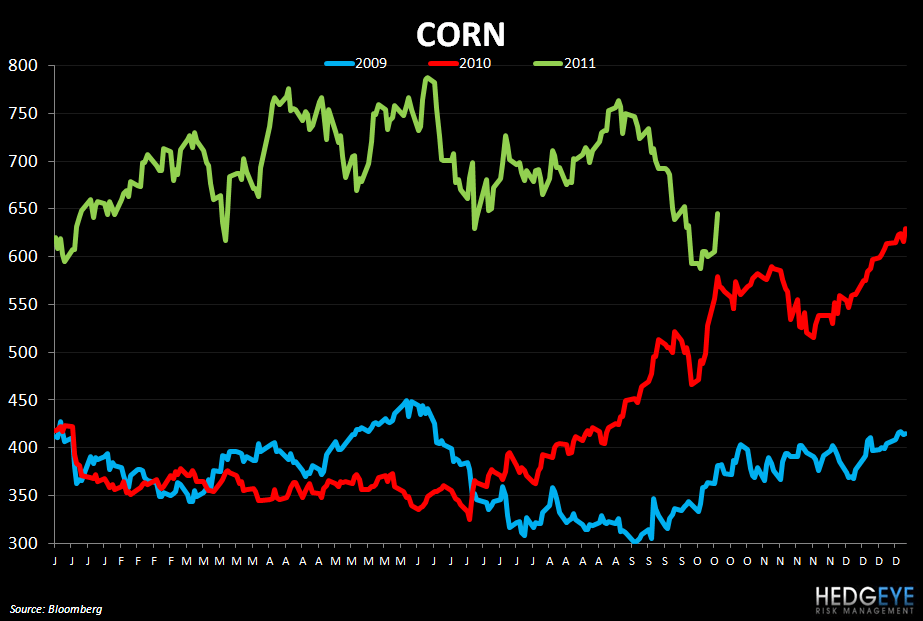

Corn prices gained over the last week but are again falling today as news emerged from the government that stockpiles of the grain before the 2012 harvest will total $866 million bushels, up from 672 million forecast in September. While the dollar decline last week helped drive grain prices higher over the same period, the supply and demand metrics for corn are pointing to continuing declines. Our macro team’s view is also dollar-bullish (for now). The decline in corn/wheat prices is a positive for food processors such as TSN and SAFM in particular, particularly as beef prices continue higher. Rising beef prices are a concern for WEN, TXRH and many others in the restaurant industry.

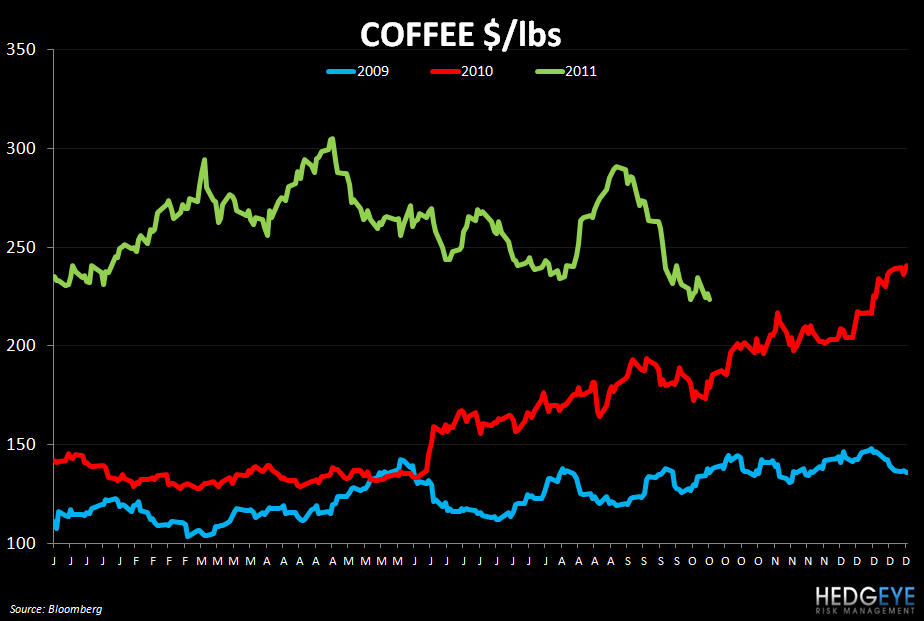

Coffee prices have continued to slide, making it less likely that additional price raises from coffee retailers such as SBUX, DNKN, PEET, GMCR, CBOU and THI are imminent. We would expect high retail prices to persist for some time as inventory bought at elevated prices is worked through.

Chicken wing prices declined on the week, which is a positive for BWLD. However, wing prices have been trending higher for much of the last month and if the upward momentum recommences, BWLD could see some shift in sentiment. BWLD is a favorite of ours on the short side.

CORRELATION TABLE

SUMMARY

Grains shooting higher last week on the declining dollar and “improving economic prospects” impacted food processor stocks like TSN and SAFM. Today, following an upward revision of inventory estimates, corn is declining and the Food Processing name are outperforming.

As we have been writing of late, declining commodity costs are generally a positive for restaurants but it is worth noting that much of the softness in commodity demand is related to softening economic conditions and this implicitly means a drop in demand for consumer goods and services. We believe the dollar impacted trends over the last week but, as with corn, much of the incremental supply and demand data hitting the tape is bearish for prices.

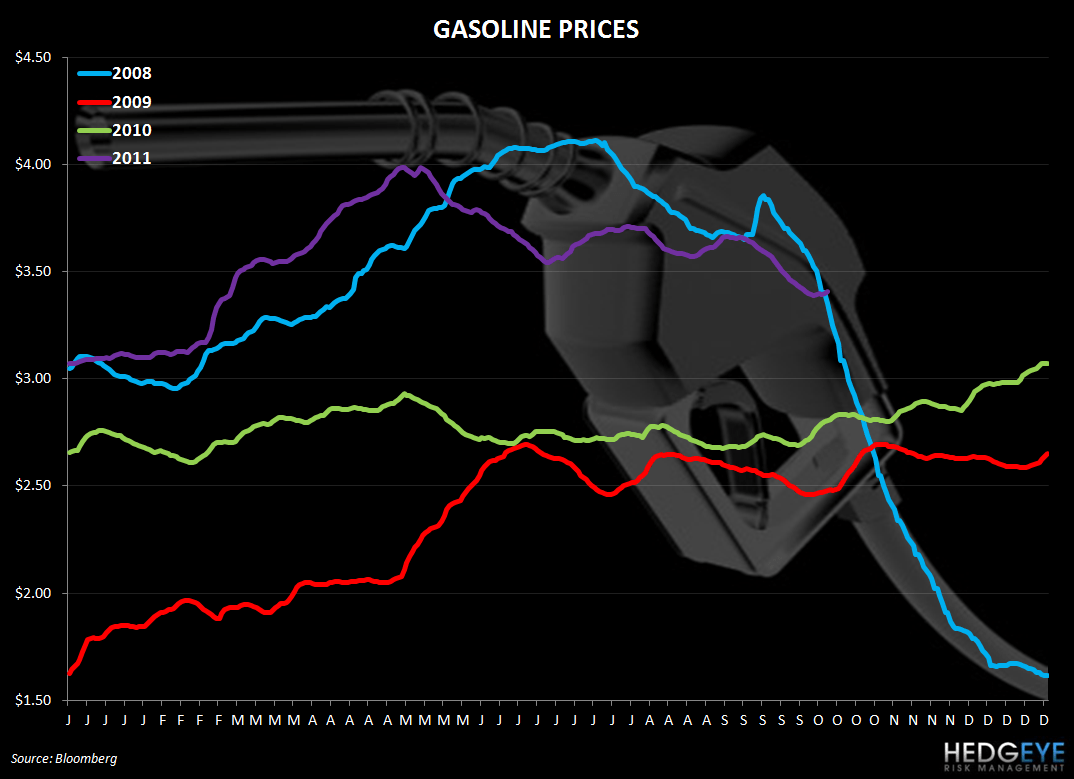

Gasoline prices continue to toe the 2008 line but the weaker dollar supported price over the last week.

CORN

Corn has been trending lower but popped up almost 10% last week. The declining dollar most likely had an impact (see correlation table). It seems that the data points emerging today regarding stockpile estimates in the U.S. could be triggering a resumption of the downward trajectory in corn prices. If this is the case, this is a positive for protein producers that can enjoy much needed relief as feed prices decline. Supply and demand concerns (rising inventories and slowing economic growth) seem to be attracting investor attention in today’s trading.

Below is a selection of comments from management teams pertaining to grain prices from recent earnings calls.

PNRA (7/27/11): “Just to note on the cost of wheat, in 2011 overall, the per-bushel cost will be about the same as 2010 due to our laddering purchasing strategy.”

“We are going to take price in the fourth quarter. This price will offset dollar for dollar the per-bushel inflation of wheat of approximately $3 a quarter that we're going to see in the fourth quarter of this year and then across next year”

“We do continue to expect significant inflationary pressures in 2012, 4% to 5% food inflation, $10 million of unfavorability on wheat costs, which means that we don't expect operating margin much better than flat to full-year 2011 in 2012.”

HEDGEYE: This past week aside, weak global demand and a stronger dollar are currently trumping the adverse impact on supply due to weather and fires in the U.S. In fact, corn and wheat stockpile estimates have risen globally, which is leading grain prices lower today. While this is a positive in terms of costs, slowing demand may also mean lower sales for PNRA, so it remains to be seen if margins improve from this effect, even if high wheat costs come down.

DPZ (7/26/11): “We're fairly locked in on our chicken, locked in on our wheat into – partway into next year.”

PZZA (8/4/11): “We're actually covered through Q1 from a contract standpoint. So from a supply chain disruption or even significant price impact we don't anticipate anything between now and the end of the year.”

CHEESE

Cheese prices declined -1.2% on the week. Prices have been extremely volatile this year but, for companies that have exposure to cheese prices (like DPZ, PZZA, TXRH, YUM and others), the recent leg down in dairy prices is encouraging.

Below is a selection of comments from management teams pertaining to cheese prices from recent earnings calls.

DPZ (7.26.11): “Given higher than originally anticipated cheese prices, we currently expect our overall market basket for 2011 will increase by 4.5% to 6% over 2010 levels. This was up from our previously communicated range of 3% to 5%.”

HEDGEYE: We recently highlighted the fact that DPZ’s last earnings call took place during a trough in cheese prices and we expected a change in tone from the commentary in early May. It remains to be seen if cheese prices will remain above 2010 levels for the remainder of the year but CAKE’s guidance for inflation in 2011 recently became much more realistic, although not a sure thing.

TXHR (5.2.11): “We've also got a lot of flow in the dairy markets, in cheese, so there's other things beyond produce that do move around throughout the year.”

HEDGEYE: In 1Q09, TXRH called out favorable beef and cheese prices as being primary drivers of cost of sales being down 126 bps in the quarter. Cheese was a contributor to a cost of sales increase in 2Q11, as we predicted. For the remainder of the year, barring another (possible) spike in prices, TXRH could see some margin relief from lower dairy costs.

CMG (4.20.11): “As we move into 2011, we're expanding our use of cheese and sour cream made with milk from cows that are raised on open pastures rather than spending much of their time in confinement, as most dairy cattle do.”

HEDGEYE: For CMG, the lower levels of dairy costs, if they persist, will offer some food costs relief on the company’s P&L.

COFFEE

Coffee prices declined over the last week even as the dollar weakened. Despite the recent drop, coffee prices remain up 26% on a year-over-year basis. Coffee is trading higher today as optimism grows that Europe will control the region’s debt crisis, boosting the outlook for commodity demand.

Below is a selection of comments from management teams pertaining to coffee prices from recent earnings calls.

PEET (8/2/11): “As we indicated, in our first quarter call, we had to buy a small amount of our calendar 2011 coffee beans at significantly higher prices and this coffee will roll into our P&L during the third and fourth quarter.”

“Higher priced coffee resulted in gross margins this quarter being 290 basis points below prior year. In our first quarter conference call, we indicated that in addition to the overall higher price coffee market, we had to buy a small amount of coffee this year at significantly higher prices. And as a result, we expected our coffee cost to be 40% higher in fiscal 2011.”

HEDGEYE: Peet’s is a company with a very competent management team that manages coffee costs extremely well. Its higher-end, loyal customer base makes the price elasticity of demand more inelastic than for other coffee concepts’ products.

SBUX (7/28/11): “As I mentioned earlier, are absolutely a headwind for us in the full business and that's most acutely impactful on margins in CPG as it's a much more coffee intensive cost structure, as you know. I can tell you that the decline as I spoke about it earlier from about 30% operating margin in CPG this year down to the target 25% next year is really all explained by commodities. Absent commodity inflation we'd be at or improving our margin in the coming year.”

“As we had anticipated, in recent weeks, coffee prices have retreated significantly from a high of more than $3 per pound just a couple of months ago to levels now near $2.40 per pound. As prices have been falling we continue locking up our needs for fiscal '12 and now have virtually the full year price protected.”

HEDGEYE: Starbucks is aligning itself with the right partners to gain more control of its coffee costs to provide investors with more certainty going forward and to protect its margins as global coffee demand continues to rise.

GMCR (7/27/2011): “However, what we've said is that should coffee prices or other material costs spike, we will certainly consider price increases as necessary. We certainly hope that we do not have to cover one again next year. But our objective long-term is attempting to maintain our gross margin as we would see input costs come along.”

HEDGEYE: GMCR hedges out 6-9 months in advance. Strength in the dollar has helped bring coffee prices lower but whether or not dollar strength will continue or not will be a significant factor in future price action in coffee. Growing demand, globally, is bullish for coffee prices over the long term.

Howard Penney

Managing Director

Rory Green

Analyst