Golden Week daily table revs surpass HK$1 billion

No sign of a Macau slowdown through Golden Week. Macau table revenues were HK$10.85 billion through the first 10 days of the month, equating to HK$1,085 million per day. Last year, Golden Week produced average table revenues of HK$780 million per day so we saw a 39% increase in that metric this year. Our preliminary full month estimate for October, including slots, is HK$25-26 billion which would equate to a 36-42% YoY increase. Obviously, October should be a monthly record. We would note that our full month projection assumes a sharp deceleration in GGR per day following the end of Golden Week.

We are hearing that hold percentage was a little higher than normal. The one negative may be that the numbers seem to be fueled by VIP. Mass, particularly on the low end, was a little disappointing to the operators.

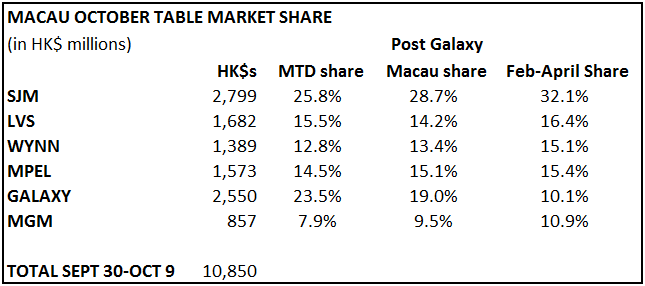

For market share, Galaxy was the clear standout while MGM and SJM were disappointing.