Having trouble viewing the charts in this email? Please click the link at the bottom of the note to view in your browser.

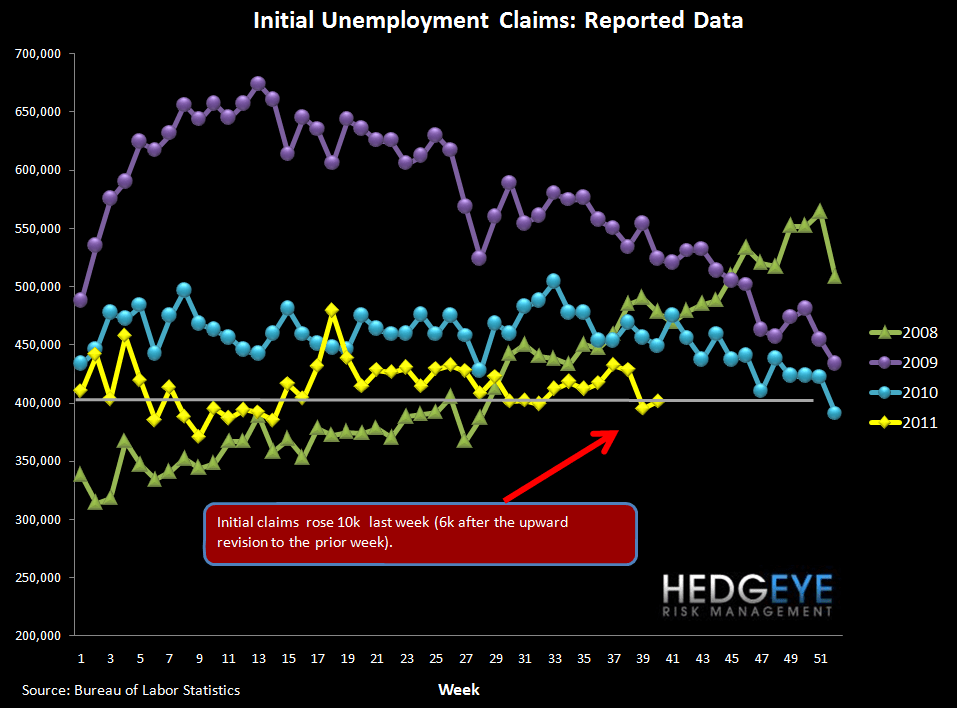

Initial Claims Give Back Some of the Gains

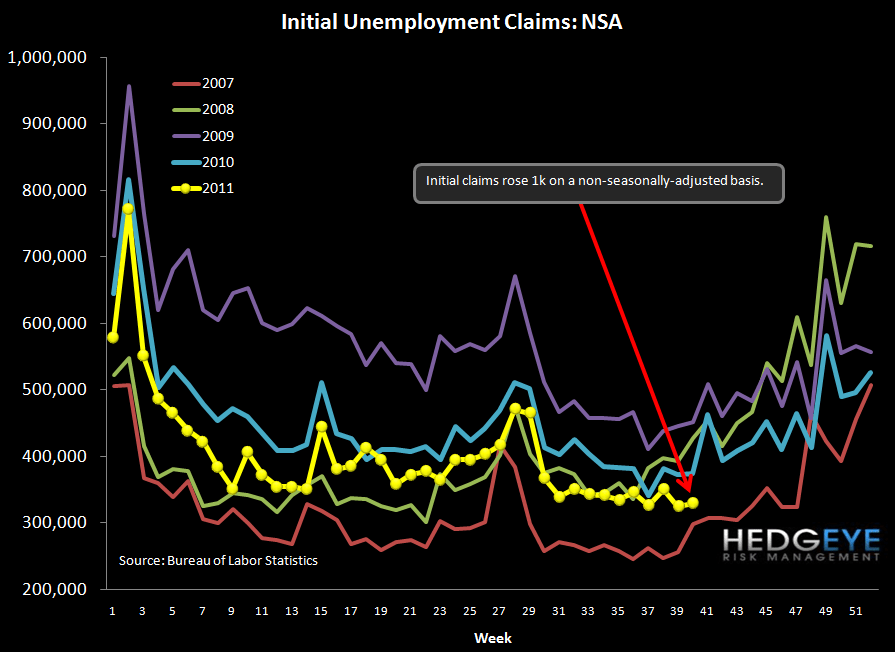

Initial claims rose 10k last week to 401k (+6k net of the upward revision to the prior week). This is a partial retracement of the prior week's 32k decline. Quarter-end generally involves significant seasonality, and the Department of Labor noted last week that technical factors related to seasonal adjustment fueled the decline.

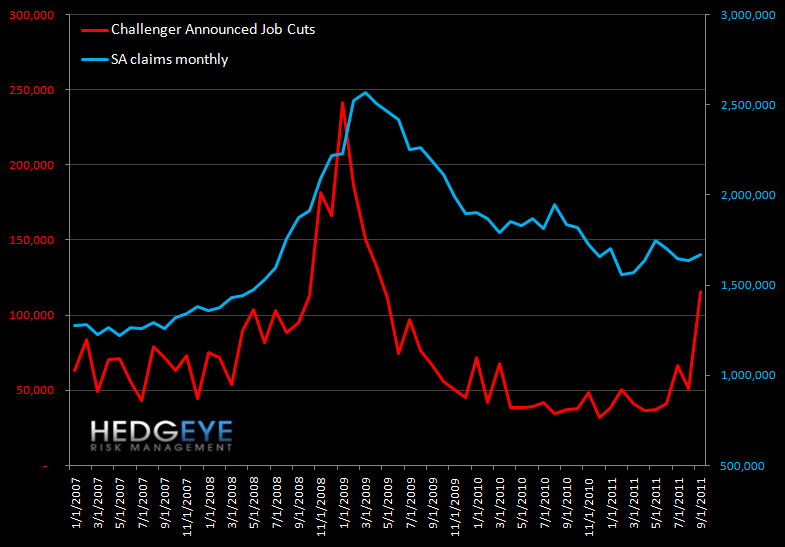

Challenger announced job cuts, out earlier this week, paint a very negative picture for initial claims going forward. Job cuts rose to 115,730, up 211% YoY. These job cuts will flow through initial claims over the coming months.

Bigger picture, monetary stimulus has had a tight correlation to improving initial claims. The lack of further easing from the Fed means that this tailwind is now gone. With further fiscal stimulus also off the table, we expect that initial claims will reflect growing weakness.

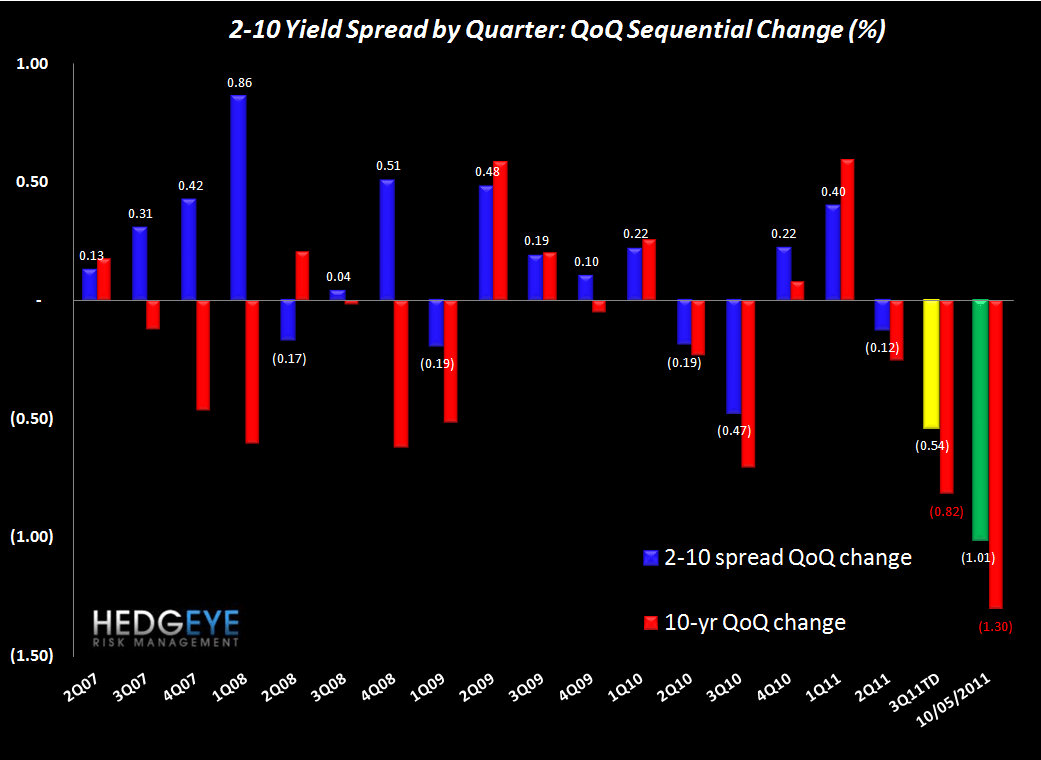

2-10 Spread Remains a Headwind

The current rate environment remains very difficult for bank margins. The 2-10 spread tightened 11 bps in the last week to 162 bps.

Subsector Performance

The table below shows the performance of financial subsectors over various durations.

Joshua Steiner, CFA

Allison Kaptur

Having trouble viewing the charts in this email? Please click the link below to view in your browser.