TODAY’S S&P 500 SET-UP - October 4, 2011

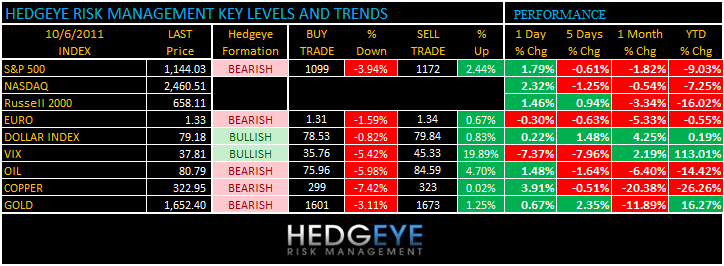

As we look at today’s set up for the S&P 500, the range is 73 points or -3.94% downside to 1099 and 2.44% upside to 1172.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 1427 (633)

- VOLUME: NYSE 1194.51 (-28%)

- VIX: 37.81 -7.4% YTD PERFORMANCE: +113.01%

- SPX PUT/CALL RATIO: 1.76 from 2.00 (-12%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 38.36

- 3-MONTH T-BILL YIELD: 0.00%

- 10-Year: 1.90 from 1.89

- YIELD CURVE: 1.64 from 1.63

MACRO DATA POINTS (Bloomberg Estimates):

- 8 a.m.: RBC Consumer Outlook Index,

- 8:30 a.m.: Initial Jobless Claims, est. 410k

- 9:45 a.m.: Bloomberg Consumer Comfort, est. -52.0

- 10:30 a.m.: EIA natural gas

- 11 a.m.: Fed’s Fisher speaks in Fort Worth, Texas

- 11:30 a.m.: U.S. to sell $10b 5-day cash mgmt bills

- U.S. announces 3-yr, 10-yr, 30-yr auction sizes

WHAT TO WATCH:

- Former Apple CEO Steve Jobs passed away; Apple lower in European trading

- Retailers report monthly sales; Retail Metrics sees 4.9% gain on delayed back-to-school shopping

- BOE and ECB are both expected to leave their key interest rates unchanged; Jean Trichet presides over his final meeting

- EC President Jose Barroso said the commission is proposing coordinated action to recapitalize banks

- Microsoft said to be nowhere close to making a bid for Yahoo!

- Geithner to tell House Financial Services Committee Europe debt crisis poses risk to global growth

- HTC reports record profit on emerging markets demand

- No IPOs expected to price today

COMMODITY/GROWTH EXPECTATION

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- World Food Prices Fell for Third Month on Slumping Grains

- Hermes Fund Sees Biggest Rebound in Gold, Grains: Commodities

- Copper Advances as European Officials May Contain Debt Crisis

- Farmland Seen Returning Up to 12% by U.S. Pensions Manager

- Oil Rises a Second Day After U.S. Stockpile Drop, Jobs Increase

- Corn Gains for Second Day as Informa Cuts Forecast for U.S. Crop

- Gold Gains a Second Day as Europe Debt Woes Spur Investor Demand

- Sugar Climbs as Lower Price May Spur Demand; Coffee Advances

- Coffee Crop in Vietnam Region to Jump 10% as Quality Gains

- Thailand’s Rice-Buying Plan Will Spur Economy, Yingluck Says

- Oil’s Best See No Reversing Worst Run Since 2008: Energy Markets

- New Hope Proves Exception to Coal Deals Returning Dust: Real M&A

- Coal Price Signals Opportunity in Stock Plunge: Chart of the Day

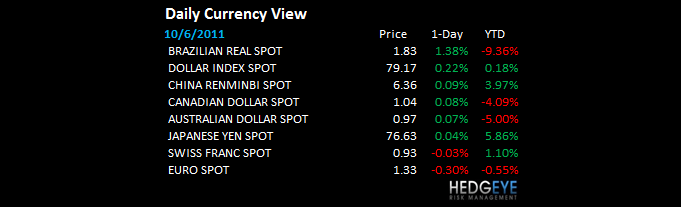

CURRENCIES

EUROPEAN MARKETS

DAX – this move higher in German stocks is much more consequential than anything being squeezed in Asia or the US; the immediate-term TRADE line for the DAX that KM has been flagging = 5439; watch that line closely because it gives you plenty of information on what rumor is coming down the pike next. KM would not short Germany if that line holds.

EURO – interestingly, but not surprisingly, the Euro is up this morning on Barosso’s Bazooka comments (read them); problem there is timing (there is no timing!) and it will be very interesting to see if the Euro can get above a short-term line of 1.34 resistance if the Dutch vote down an expansion of the bazooka later on today.

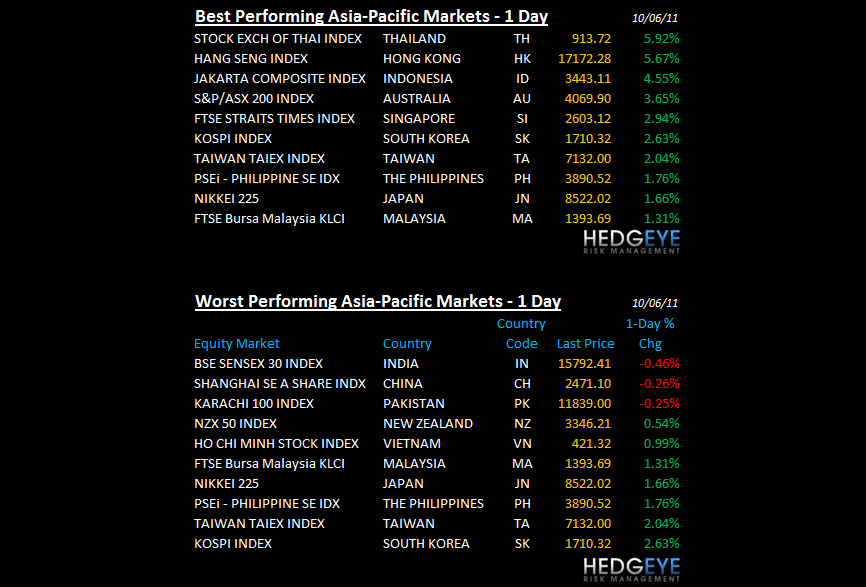

ASIAN MARKETS

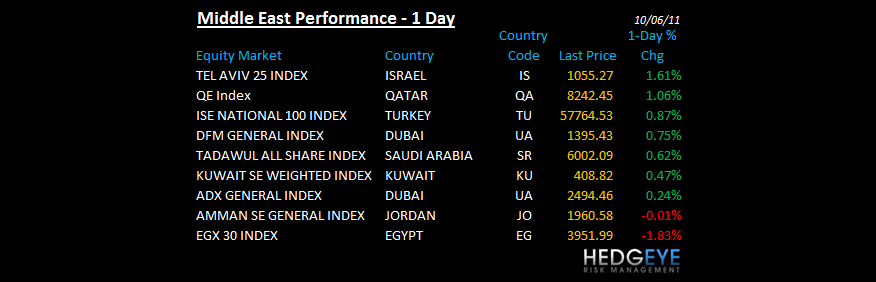

MIDDLE EAST

Howard Penney

Managing Director