This note was originally published at 8am on September 30, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“The readiness is all.”

-William Shakespeare

You have to give it to William Shakespeare, he had a way with words. Just as Canadian hockey players have a way with understatement. When it comes to the daily global macro market grind, Shakespeare’s quote above about says it all. You are either ready; or you are not ready. It is really that simple.

I’ve recently been reading, “How Markets Fail”, by John Cassidy. I wouldn’t say I agree with all of Cassidy’s observations in the book, but he does offer some interesting anecdotes regarding markets and prevailing wisdom. Near the end of the book, Cassidy takes a break from analyzing markets and describes the origin and construction of the Millennium Bridge in London.

As background, in 1996, the London Borough of Soutwark, the Royal Institute of British Architects, and the Financial Times newspaper held a competition to build a new footbridge from the Tate Modern Art Gallery to St. Paul’s Cathedral, which, of course, would cross the Thames. The winning bid ultimately came from sculptor Sir Anthony Caro, architect Sir Norman Foster, and the engineering firm of Ove Arup.

The winning entry was a spectacular design “with steel balustrades projecting out at obtuse angles from a narrow aluminum roadway.” The designers insisted that the unique looking bridge could support at least five thousand pedestrians. So, on June 10, 2000, just in time for the Millennial, the bridge was opened up by Queen Elizabeth II with much fanfare and thousands of pedestrians started to walk across the bridge.

The bridge began to immediately sway causing pedestrians to cling to the sides of the bridge and created what has been described as a sea sick feeling amongst those who traversed it. Two days later, London authorities quickly shut the bridge down for an indefinite period, concerned about the stability of the bridge and safety of pedestrians utilizing it.

After studying the issue, the engineers at Ove Arup concluded that the issue was with the pedestrians and not due to the actual design of the bridge. In part, the engineers were correct. The bridge had been designed to gently swing to and fro, but what the designers didn’t account for was that pedestrians would exaggerate these movements in unison as they walked across the bridge. Arguably, the engineers’ design was not ready.

The natural movement of walking produces a slight sideways force. Thus as hundreds, even thousands of pedestrians walked across the bridge, they unwittingly created a unified sideways force that amplified the movement of the bridge. In effect, the natural wobble of the bridge became self-reinforcing and fed on itself. The savvy engineers at Ove Arup even came up for a name for this action, called “synchronous lateral excitation”.

In preparing you for the market action in the coming quarter, one of our Q4 themes will be related to this idea of “synchronous lateral excitation”. In global markets, currently, this concept is increasingly related to heightening correlations across asset classes. In some instances, this heightened correlation applies to even seemingly unrelated asset classes. Simply put, investors are increasingly acting in unison, which is amplifying price movements across markets and amplifying future risk. We’ve termed this, the “Correlation Risk” in previous notes.

Interestingly, though, even as cross-asset correlations are heightening globally, there are seemingly outlier markets that remain less correlated. According to recent report from Bloomberg:

“The 30-day correlation coefficient between the S&P 500 Financials Index and the banking group in the Stoxx Europe 600 Index has averaged 0.65 in 2011, according to data compiled by Bloomberg. The figure for European banks and Japan's Topix Banks Index is 0.25.”

Yes, you read that correctly. Japanese banks are becoming a global safe haven. Were you ready for that?

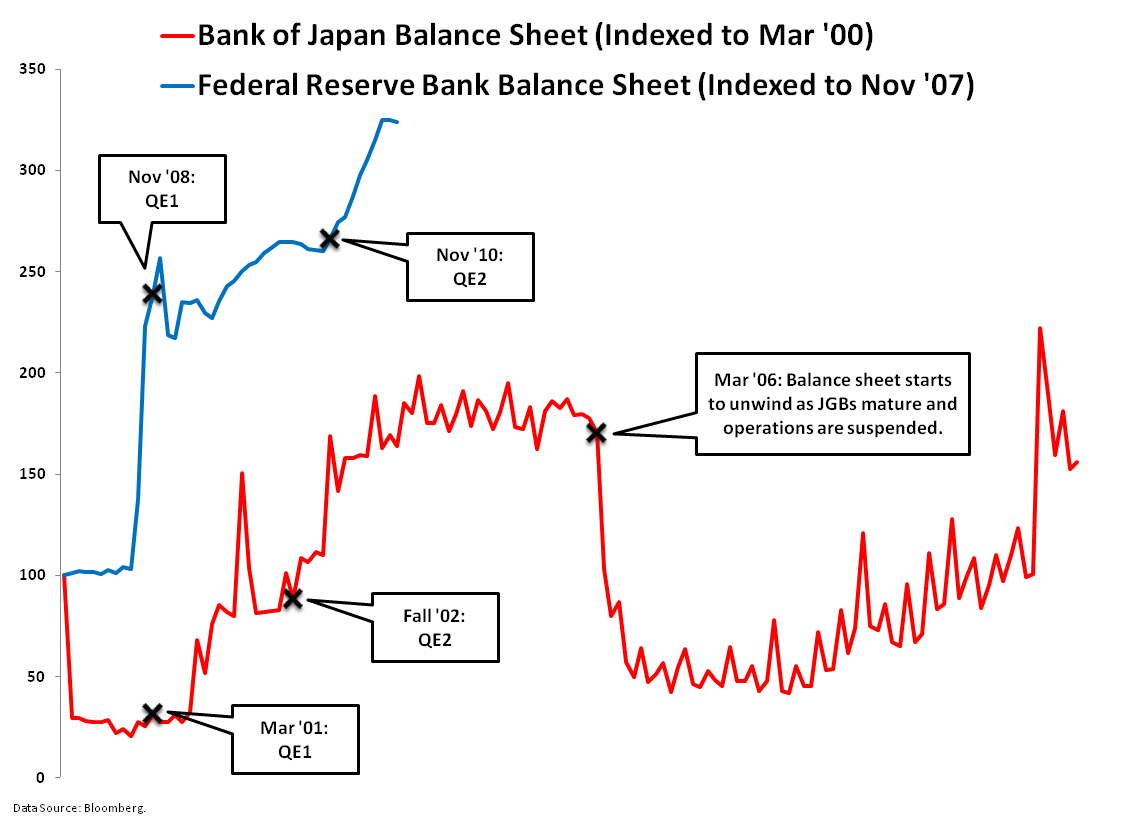

My colleague, and Hedgeye Asian analyst, Darius Dale recently updated his thoughts on Japan in a presentation. A key takeaway is that in the last three years U.S. policy makers have been much more Japanese than the Japanese in terms of monetary policy. In fact, not only did Chairman Bernanke and his associates cut rates more aggressively from the outset of the financial crisis, they have also leaned more heavily on the balance sheet of the central bank than their Japanese counterparts.

Interestingly, and related to the topic of global banking risk, this morning credit default swaps on Morgan Stanley reached a new cycle high of 455 basis points from 275 basis points at the end of August. In effect, Morgan Stanley is now seen to be as risky a credit as the Italian banks. Are you ready for that?

Part of increasing correlation between global markets is and has been the advent of increasing economic globalization and integration. In 2011, it is truly a global economy. This morning, the Chinese HSBC manufacturing PMI came in at 49.9, which is sub 50 for the third straight month. The immediate reaction to this tepid manufacturing number from China can be seen in European equities off 1.5 – 3.0% across the board. The German Dax is leading the way to the downside as a German lawmaker spoke out against an expanded EFSF.

The Hedgeye team has certainly tried to do our best to alert our subscribers as to the dismal outlook for equities this year and this quarter. To that point, with the last trading day for Q3 2011 today, the SP500 is down -12.1% quarter-to-date. Based on the performance of the SP500 and some broad hedge fund return numbers we have seen, there is another risk to be ready for: fund redemptions. Redemptions are never fun to talk about, but they are an unfortunate reality in this business that can impact asset prices.

Hopefully this note isn’t too somber heading into the weekend, but as Shakespeare also said:

“Better three hours too soon than a minute too late.”

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research