TODAY’S S&P 500 SET-UP - October 4, 2011

Yesterday’s “Short Covering Opportunity” call was Keith’s third in the last two months (August 8th and September 12th were the other 2 time stamps).

As we look at today’s set up for the S&P 500, the range is 45 points or -2.49% downside to 1096 and 1.52% upside to 1141.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 633 (-2498)

- VOLUME: NYSE 1662.1 (+18.4% )

- VIX: 40.82 -10.2% YTD PERFORMANCE: +129.97%

- SPX PUT/CALL RATIO: 2.00 from 1.97 (+1.5%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 38.09

- 3-MONTH T-BILL YIELD: 0.00%

- 10-Year: 1.85 from 1.82

- YIELD CURVE: 1.60 from 1.57

MACRO DATA POINTS (Bloomberg Estimates):

- 7 a.m.: MBA Mortgage Applications, prior 9.3%

- 7:30 a.m.: Challenger job cuts, prior 47.0%

- 8:15 a.m.: ADP employer, est. 73k, prior 91k

- 10 a.m.: ISM Non-manufacturing, est. 52.8, prior 53.3

- 10:30 a.m.: DoE inventories

- 11 a.m.: U.S. to purchase $1b-$1.5b TIPS

WHAT TO WATCH:

- Bank of New York Mellon sued by U.S., New York for allegedly defrauding clients in FX trades

- Dexia shares rise as Belgium pledges to create a “bad bank” for assets, speculation that European policy makers mulling additional measures for region banks

- Italy downgraded three notches by Moody’s; ratings agency says more downgrades in euro-region possible

- Hewlett-Packard to decide whether to spin off its PC unit by end of month, CEO Meg Whitman said

- EMI bids, due this week, said likely to come in lower than expected, people familiar tell Bloomberg

- U.S. Trade Representative holds public meeting on China’s compliance with World Trade Organization commitments

- Cisco CEO John Chambers, Oracle CEO Larry Ellison speak at Oracle Openworld

- Bill Ackman said he may sell shares in a hedge fund to secure more permanent capital for investments as soon as next year.

- Kinetic Concepts said to host lender meeting today to discuss refinancing

COMMODITY/GROWTH EXPECTATION

GOLD – Hedgeye made a short call in Gold yesterday (before the down move) as Gold failed at the intermediate-term

TREND line of resistance ($1672); first support = $1573 and the long-term TAIL of support is all the way down at $1491; KM expects Gold to come under increasing selling pressure as 2yr UST rates hold the TRADE line of 0.21% support.

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- Commodities Climb From 10-Month Low as Bernanke May Buoy Growth

- OPEC Risks Bear Market as Libyan Output Recovers: Energy Markets

- Copper Rout Unlikely to Halt Chile $67 Billion Bet: Commodities

- Indonesia May Sell More Palm Oil to China, Hurting Prices

- Gold Declines in London as Dollar’s Rally Cuts Investor Demand

- Corn Gains on Speculation 26% Slump May Attract China Purchases

- Sugar Advances as Lower Prices May Spur Buying; Coffee Climbs

- Copper Rises on Speculation Officials Are Set to Stoke Recovery

- Commodities to Rally in ’12, Says Credit Suisse Joining Goldman

- Silver Rebound May Stall at $33.15 an Ounce: Technical Analysis

- Australian Grain Regions May Get Crop-Boosting Rain This Week

- Chile’s Richest Family Risks Golden Touch With Shipping: Freight

- Komatsu Risk at 2-Year High on Yen, Economic Slump: Japan Credit

- Oil Rises From Lowest in a Year on Supply Drop, Stimulus Hopes

- Palm Oil Drops to 1-Year Low as Malaysian Reserves Set to Climb

- Rubber May Extend Drop to Lowest Since 2009: Technical Analysis

CURRENCIES

EUROPEAN MARKETS

The Russian stock market crash matters; the RTSI is flagging a negative divergence vs the rally in Europe DAX to lower highs; Russia = down -1.6% this morn and down, get this, -43% since April when the down Dollar/up inflation trade stopped! Get the USD right; you’ll get a lot more right.

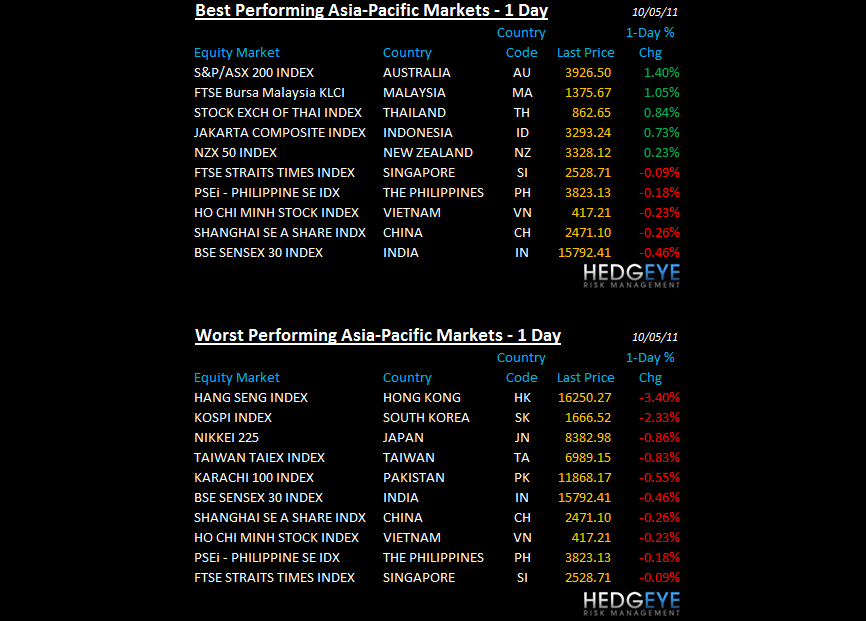

ASIAN MARKETS

MIDDLE EAST

Howard Penney

Managing Director