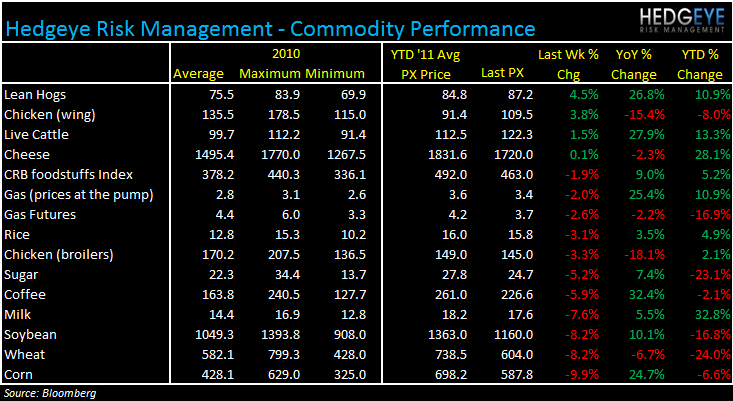

Ongoing concerns surrounding economic growth coupled with the strengthening dollar are pressuring commodity prices. Week-over-week, most of the commodities we track declined significantly.

STOCK TAKEAWAYS

Declining grain prices are bullish for restaurant industry margins and bearish for protein prices. This is a positive for food processors such as TSN and SAFM in particular, particularly as beef prices continue higher. Rising beef prices are a concern for WEN, TXRH and many others in the restaurant industry.

Coffee prices have continued to drop sharply, making it less likely that additional price raises from coffee retailers such as SBUX, DNKN, PEET, GMCR, CBOU and THI are imminent. As we said last week, we expect high retail prices to take some time to adjust, given the need to clear inventory purchased at elevated prices.

Chicken wing prices continue to gain, which is a concern for BWLD. See our note (10/4) for more detail on our short BWLD thesis. We believe coming margin pressure could be expedited and exacerbated by soft sales in the fourth quarter. Furthermore, from a sentiment perspective, the Street is more bullish (60% Buys) on the stock than it has been in some time.

Dairy prices have been moving sideways over the past couple of weeks, and cheese prices remain down year-over-year. This is a positive for CAKE, DPZ YUM and PZZA, especially considering the level cheese prices were at just a few weeks ago.

SUMMARY

Lean hogs, chicken wings, live cattle and cheese were the only commodity prices in our monitor that gained versus last week. The declines in our weekly monitor were again larger than the advances. Rice, chicken broilers, sugar, coffee, milk, soybean, wheat and corn all saw sizeable declines. As we have been writing of late, declining commodity costs are generally a positive for restaurants but it is worth noting that much of the softness in commodity demand is related to softening economic conditions and this implicitly means a drop in demand for consumer goods and services.

Gasoline prices continue to toe the 2008 line, declining as the dollar continues to strengthen and economic concerns mount.

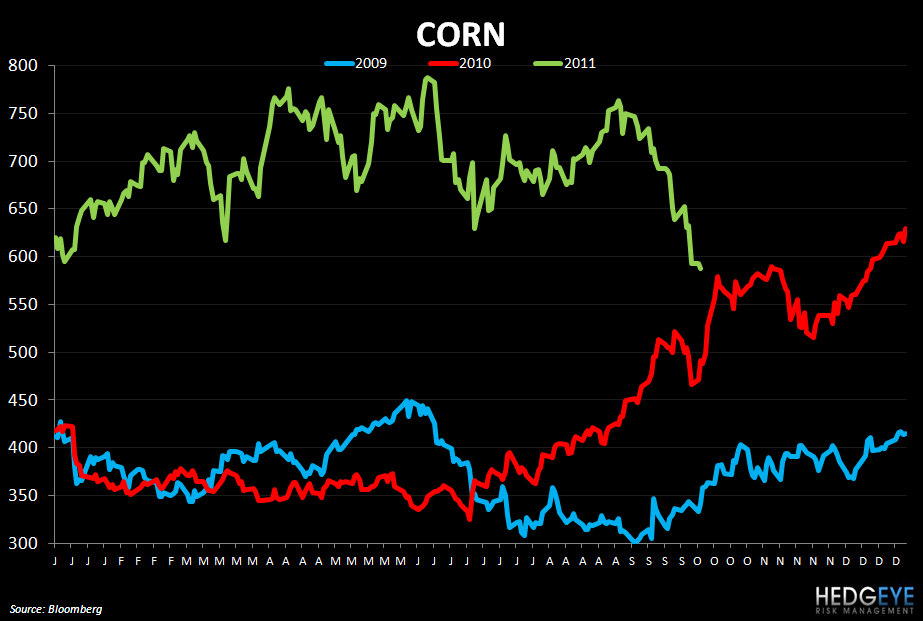

CORN

Corn has been declining sharply as demand has been slowing and stockpiles rising. This is a positive for protein producers that can enjoy much needed relief as feed prices decline. The U.S. Grain Council, according to Bloomberg, has said that China – the world’s second-largest corn consumer – won’t have enough supplies to meet rising demand even as farmers there harvest a record crop. Despite this, and concerns about a smaller U.S. crop, demand concerns seem to be catching the eye of investors as grain prices drop high-single digits week-over-week.

Below is a selection of comments from management teams pertaining to grain prices from recent earnings calls.

PNRA (7/27/11): “Just to note on the cost of wheat, in 2011 overall, the per-bushel cost will be about the same as 2010 due to our laddering purchasing strategy.”

“We are going to take price in the fourth quarter. This price will offset dollar for dollar the per-bushel inflation of wheat of approximately $3 a quarter that we're going to see in the fourth quarter of this year and then across next year”

“We do continue to expect significant inflationary pressures in 2012, 4% to 5% food inflation, $10 million of unfavorability on wheat costs, which means that we don't expect operating margin much better than flat to full-year 2011 in 2012.”

HEDGEYE: Weak global demand and a stronger dollar are currently trumping the adverse impact on supply due to weather and fires in the U.S. Slowing demand may also mean lower sales for PNRA, so it remains to be seen if margins improve from this effect, even if high wheat costs come down.

DPZ (7/26/11): “We're fairly locked in on our chicken, locked in on our wheat into – partway into next year.”

PZZA (8/4/11): “We're actually covered through Q1 from a contract standpoint. So from a supply chain disruption or even significant price impact we don't anticipate anything between now and the end of the year.”

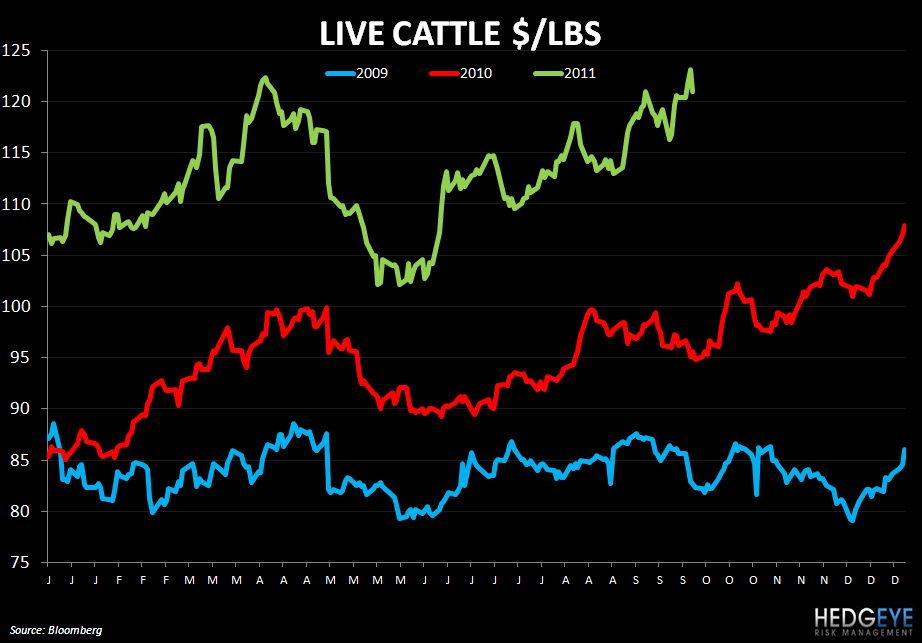

BEEF

Beef prices continue higher despite the free-fall in corn prices over the last week. Feedlot inventories shrinking and demand for meat increasing globally are two factors being cited for the continuing strength in beef prices. The U.S. cattle herd totaled 100 million heads on July 1st, the lowest for that date since at least 1973, according to the Department of Agriculture. Strong demand for U.S. beef overseas is spurring the price gains that are illustrated on the chart below.

Below is a selection of comments from management teams pertaining to beef prices from recent earnings calls.

RRGB (8/11/11): “We're still buying ground beef on the spot market… If you recall, we said 5% to 6% commodity inflation on the last call and we dropped that to 5 to 5.5. Again, that's mainly ground beef driving that.”

HEDGEYE: Live cattle prices are up 22% YoY and, we believe, will continue to be a negative for RRGB’s P&L going forward.

WEN (8/11/11): “That's one of the reasons why as we've talked about our margin guidance, we do not expect to see much relief on beef cost this year.”

CHICKEN WINGS

Chicken wing prices continue to go higher, signaling a likely end to the massive headwind BWLD has enjoyed from a margin perspective over the last couple of years. We believe that this change is coming at a difficult time for the company as sales trends have been softer in 4Q in recent years and consumer confidence is waning.

Howard Penney

Managing Director

Rory Green

Analyst