Buffalo Wild Wings remains one of our favorite names on the short side.

As detailed in the Hedgeye Restaurants Alpha, which describes our three best long and short ideas, there are several factors turning against BWLD as we move through the last few months of 2011 and into 2012.

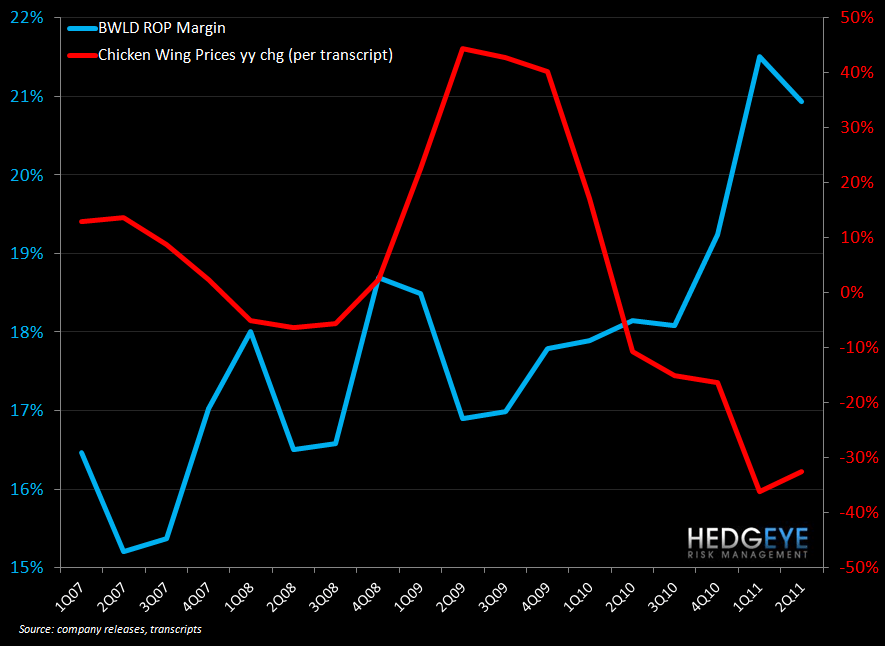

Firstly, the fourth quarter traditionally tends to be a seasonally difficult period for the concept from a traffic perspective. While the company is planning on implementing marketing initiatives around the football season in the back half of the year, we believe that a softening macro environment could impact BWLD’s fourth quarter comp. The company has been successfully taking price even as wing prices have gone lower and lower; whether or not further price increases can be taken without stymieing traffic growth is the key question going forward.

Connected to this issue of price is the fact that the relationship between restaurant operating margins and wing prices has, we believe, reached an inflection point. Wing prices have begun to climb and the substantial tailwind that the company has enjoyed is dissipating. Protecting margins from this point will require even more aggressive pricing than before and could prove difficult in this macro environment.

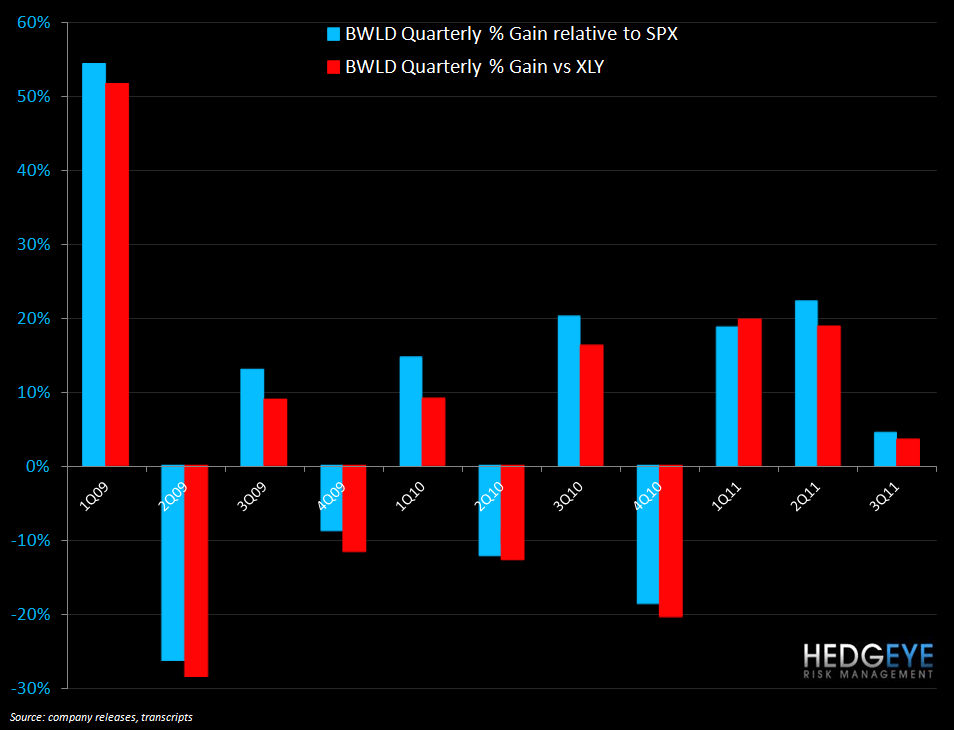

Our conviction remains strong on this name. Given the strong outperformance versus the S&P 500 and the XLY consumer discretionary ETF over the past three quarters, we would expect the reversal in the commodity tailwind and (possible) top-line issues to have a sizeable impact on BWLD’s stock price.

In conclusion, the valuation and sentiment set ups for BWLD are only supportive of our bearish stance. In terms of valuation, BWLD trades at the third highest EV/EBITDA multiple of casual dining. Some of the premium it enjoys is undoubtedly due to its growth profile and expansion into new markets. We believe that growth is good but it does come at a price and contributed to the company’s EPS miss in 2Q. From a sentiment perspective, as the second chart below shows, the street has not been as bullish as it is now in quite some time.

Howard Penney

Managing Director

Rory Green

Analyst