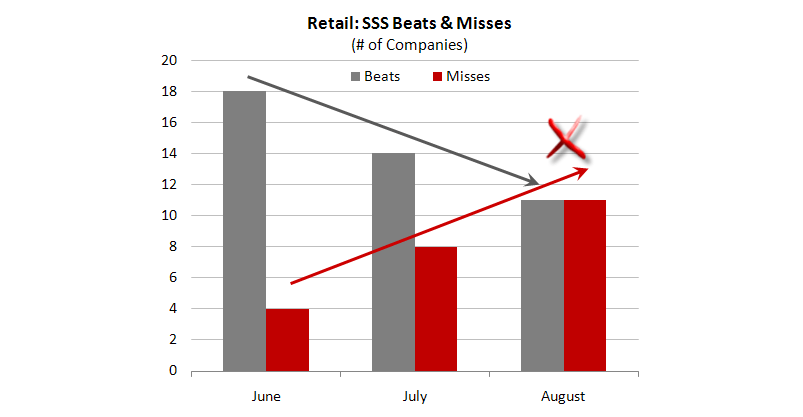

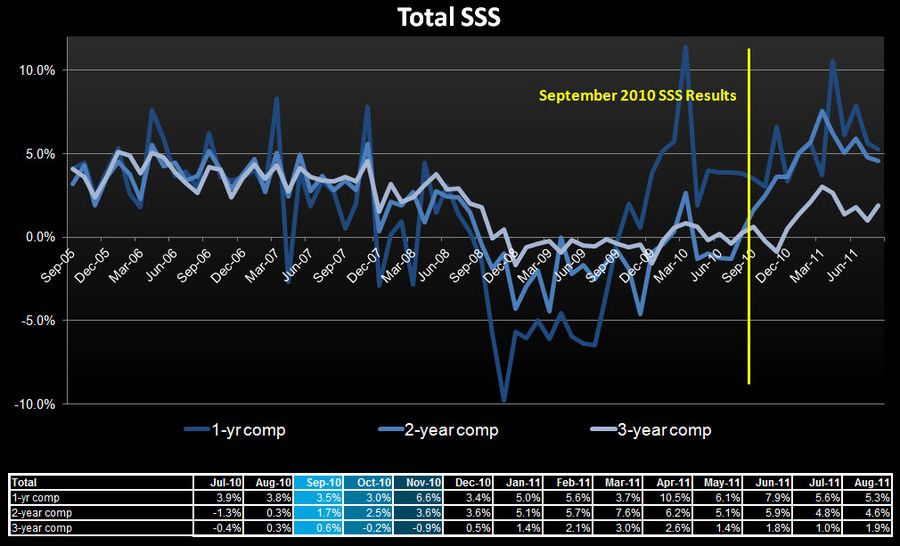

With companies set to report September sales on Thursday, retailers have greater visibility into not only Q3 results with two months now in the books, but also how they are tracking into year-end. If retailers are looking at the same Macro setup we are and the number of companies that have beat versus missed on the sales line over the last three months is any indication, we expect to see the first phase of pre-announcements from retailers later this week.

The key BTS August selling season was choppy at best and our sense is that many retailers, especially on the discretionary side, underestimated the percent of sales that were lost forever instead of pushed into September due to Irene. To date, there hasn’t been much from retailers suggesting slower than expected sales with perhaps the sole exception of KSS at a competitor’s conference earlier in the month. Since then, the Macro setup hasn’t changed and in fact, current economic pressures have mounted even further.

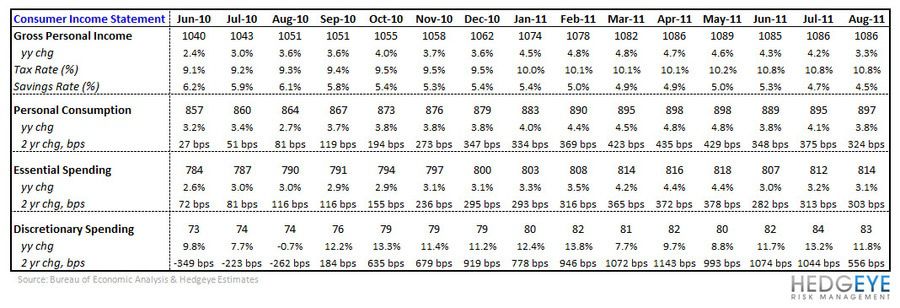

Let’s review the setup from a Macro level:

- Gross Personal Income was running up +3.6% and about to increase to over 4% compared to +3.3% today. (negative point)

- The two main levers that account for the delta between Gross Income and Personal Consumption have offset each other for the most part.

- The consolidated personal tax rate is now at 10.8% vs. 9.4% this time last year. (negative point)

- The personal savings rate is back down to +4.5% compared to +5.8%.

- In looking at ‘Essential Spending’ (food, energy, healthcare), the growth we’ve seen from June last year at (+2.6%) to May (+4.4%) has come in to +3.1%. (positive point)

- The balance of spending goes into the ‘Discretionary Spending’ line, which is considerably more volatile. This stood at +12.2% this time last year compared to +11.8% in August.

- In addition, consumer confidence is at 45.4 compared to 48.6 last year and unemployment is looking increasingly likely to weaken further before getting better near-term.

- Based on our read out of POS data (NPD & SportScan), sales in September picked up later in the month in the department store channel, but remain uninspiring. In addition, weekly ICSC retail sales continued to decelerate throughout the month.

We think that sales day and likelihood of pre-announcement activity is going to reveal a key crack as it relates to the margin weakness and unsustainable earnings expectations in retail. The tailwind in consumer income growth is shifting and relief in the form of lower taxes unlikely. A further reduction in the personal savings rate is one of the few levers left for the consumer to pull, but would in turn place the consumer on even shakier ground heading into the 1H of F12.

Shorts: JCP, UA, HBI, SHLD

Longs: LIZ, NKE, RL, TGT