TODAY’S S&P 500 SET-UP - October 4, 2011

This Correlation Crash is now readily evident to anyone who didn’t think it could happen. As we look at today’s set up for the S&P 500, the range is 50 points or -1.75% downside to 1080 and 2.80% upside to 1130. Good news is that yesterday, US stocks finally moved into immediate-term TRADE oversold territory – so today Keith is makeing the 3rd major Short Covering Opportunity call he’s made since the 1st one on August the 8th.

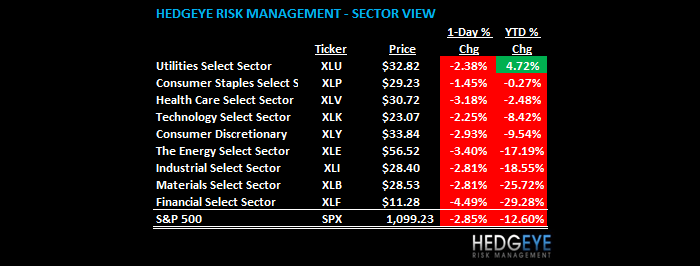

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -2498 (-662)

- VOLUME: NYSE 1403.71 (+6.08%)

- VIX: 45.45 +5.80% YTD PERFORMANCE: +156.06%

- SPX PUT/CALL RATIO: 2.29 from 1.49 (+53.14%)

CREDIT/ECONOMIC MARKET LOOK:

YIELD SPREAD – it will be fascinating to hear Bernanke testify today that this is working; the TWIST is compressing the Yield Spread to a fresh YTD low this morning (153bps wide) and only perpetuating the pain on the front lines of this fear that the banks cash earnings are under siege – in this case, the fear is well placed. I remain long the US Treasury Flattener (FLAT)

- TED SPREAD: 37.25

- 3-MONTH T-BILL YIELD: 0.02%

- 10-Year: 1.80 from 1.92

- YIELD CURVE: 1.56 from 1.67

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45 a.m./8:55 a.m.: ICSC/Redbook weekly retail sales

- 9 a.m.: Fed Gov. Raskin speaks on foreclosures

- 10 a.m.: Fed Chairman Bernanke to testify on economic outlook before Joint Economic committee of Congress

- 10 a.m.: Factory orders, est. 0.0%, prior 2.4%

- 11 a.m.: U.S. Fed to purchase $4.25b-$5b notes/bonds

- 11:30 a.m.: U.S. to sell $30b 4-wk bills

- 4:30 p.m.: API inventories

- President Obama speaks on American Jobs Act in Mesquite, Texas, before heading to campaign event in St. Louis

- 10 a.m.: House meets to consider Senate amended continuing resolution, which provides FY12 funding through Nov. 18

WHAT TO WATCH:

- Apple’s next iPhone may be showcase for improved voice controls, hinting at improved speech technology. Event at 1 p.m.

- Belgium, France say they will act to prop up Dexia if necessary

- Europe faces rising risk of double-dip recession, S&P says

- Fed Chairman Bernanke testifies on economic outlook before Joint Economic Committee of Congress, 10 a.m.

- U.S. regulators said to consider if as many as 4.5m foreclosure cases will be examined to determine if compensation is due: WSJ

- General Maritime (GMR) is in talks with lenders, creditors on potential restructuring

- Kinetic Concepts (KCI) unnamed bidder withdrew offer; co. expects to be taken private by Apax Partners for $68.50/shr

- McGraw Hill (MHP) sells nine-station broadcasting group to E.W. Scripps (SSP) for $212m in cash

COMMODITY/GROWTH EXPECTATION

COMMODITIES: crash in copper and oil continue; both immediate-term TRADE oversold (finally) at $2.95/lb and $76.09/barrel respectively

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- Goldman Cuts GDP Estimates; Sees German, French Recessions

- Mordashov Expands Steel Output as Mittal Retrenches: Commodities

- Commodities to Rally 20% on Emerging Markets, Goldman Says

- Ivanhoe, Rio Reject Mongolian Bid to Change Oyu Tolgoi Deal

- Oil Drops a Third Day as Goldman Cuts Forecast for Brent Crude

- Gold Rallies for Fourth Day as Europe Crisis Spurs Haven Demand

- BHP, Rio Bond Risk Soars to 2-Year High on Slowdown Concerns

- Copper Falls for Fifth Day as European Crisis May Curb Demand

- Record U.S. Gasoline Cargoes Drive 17% Gain in Tankers: Freight

- Commodities to Extend Decline, Says Sarin: Technical Analysis

- Oil Falls to Eight-Week Low on U.S. Supplies, Libyan Production

- Copper Drops in London Before U.S. Factory Orders: LME Preview

- Platinum-Gold Ratio Drops to Lowest Level Since at Least 1987

- Sugar Production in India Delayed by Cane-Pricing Dispute

- CME Group Increases Margins on Copper, Platinum Futures

- Oil Speculation Rules Probed by Levin Panel as CFTC Nears Vote

- Palm Oil Drops for Second Day on European Debt Crisis Concern

- Gold Gains for Fourth Day as Europe Debt Concern Spurs Demand

- Uranium Prices Rise as Fukushima Volatility Persists, Ux Saysd

CURRENCIES

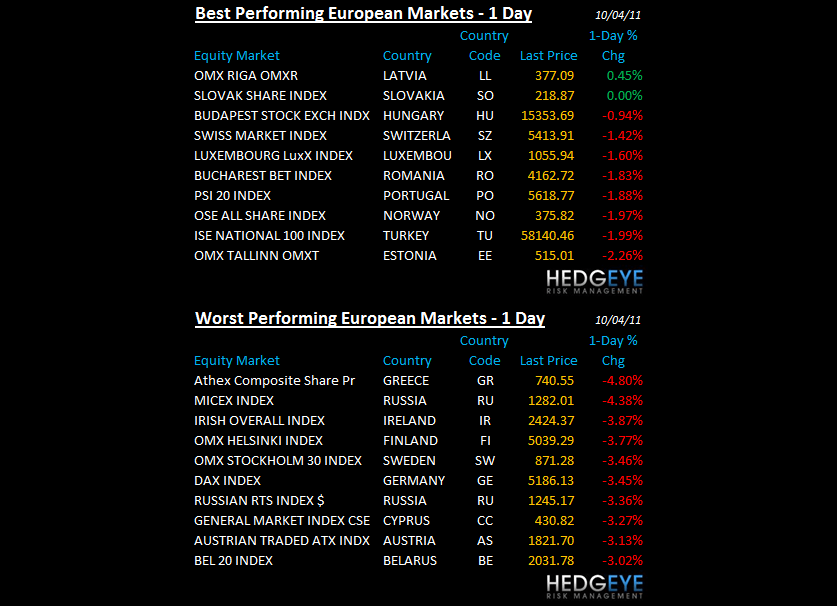

EUROPEAN MARKETS

EUROPE: crash continues after DAX broke the line we signaled as critical support yesterday (5439); Italy (which we're short) = -38% since Feb.

DAX: the only line left (Germany’s TRADE line of support at 5439) is now gone and Ackerman (Deutsche Bank) is telling the world what we all know (the money-center banks of the world are going to miss badly and be forced to guide down)

ASIAN MARKETS

ASIA – crashing equities and currencies continue to be led by Hong Kong (down another -3.4% overnight; down -33% since

US Equities peaked in April!); KOSPI crash continued at down -3.6% (down -23% since May); Singapore -3%; Thailand -2.7%, etc.

MIDDLE EAST

Howard Penney

Managing Director