Positions: Short Italy (EWI)

Some things change, others stay the same. As the European sovereign debt and banking contagion crisis chugs along, the underlying current remains that despite Germany’s pledge to back the EFSF, the fund is undercapitalized to deal with the bailout/default needs of Italy or Spain, and Trichet and the ECB remain unwilling to let the Bank take on more risk via larger sovereign bond purchases.

As the powder keg of indecision on go-forward policy from Eurocrats heightens, so too does volatility across European capital markets. We’re positioning to get short a number of European economies at the right price. Currently we’re short Italy in the Hedgeye Virtual Portfolio via the etf EWI, but numerous indices are broken across immediate and intermediate TRADE and TREND durations, an explicit bearish set-up in our models. [For more on our thesis on Italy see our note titled “Shorting Italy (EWI)” on 9/30].

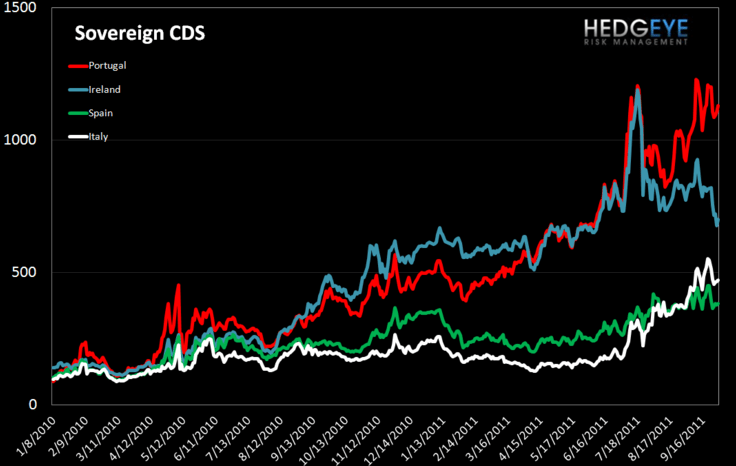

From a risk perspective, we continue to take our cues from government bond yields and cds spreads. As we’ve noted in previous work, the 6% yield on 10 year government bonds has been a historically significant level for the PIIGS, meaning that a violation of the line to the upside resulted in an expeditious upward run (see chart below). Italy, like Spain, has maintained a level below 6% since the ECB restarted the SMP on August 8th, and currently trades at 5.50%, whereas Spain is trading at 5.08%. However, should yields rise above the 6% level, we’d expect the ECB and European policy makers to act quickly to attach another band-aid to the Union’s fiscal imbalances.

European Sovereign CDS – European sovereign swaps were mostly tighter week over week, with only the German sovereign CDS spread widening. Irish sovereign CDS spreads tightened week over week by 15%. (Please note: Greek CDS is not shown in the chart because the data was not available. To gauge Greek credit risk, please refer to Greek bond yields below.)

We don’t have the crystal ball on the timing of the next bailout band-aid, however below we provide a calendar of catalyst around which an announcement could be made:

4th October: ECOFIN Council.

6th October: ECB Interest rate decision. Jean Claude Trichet’s last Meeting as President.

13th October: Eurogroup to decide on release of 6th tranche of Greece bailout funding.

13th October: Italian Bond Auction.

14th October: G20 Finance Ministers.

Mid-October: Possible Italian proposals on labor market and other structural reforms.

17th October: Possible Slovakian vote on EFSF.

17th/18th October: EU Summit.

27th October: Irish Presidential Election.

28th October: Italian Bond Auction.

Late-October: Expected publication of European Commission report on Eurobonds.

1st November: Mario Draghi replaces Jean Claude Trichet as ECB President.

4th November: G20 Heads of State.

8th November: ECOFIN.

20th November: Spanish Elections.

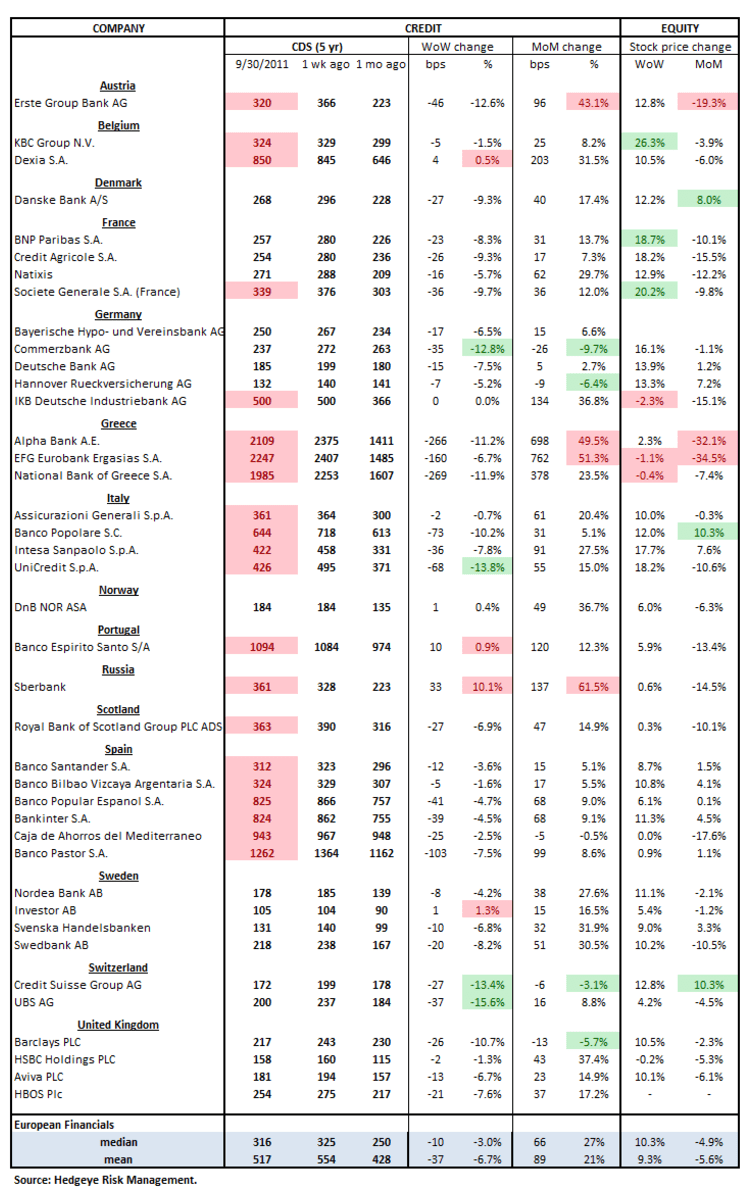

Finally, below we present the European Financials CDS Monitor from our Financials team. Bank swaps mostly tightened in Europe last week. Swaps tightened for 34 of the 40 reference entities, widened for 5, and was unchanged for 1. The average tightening was 6.7%, or 37 basis points, and the median tightening was 3.0%.

Matthew Hedrick

Senior Analyst