TODAY’S S&P 500 SET-UP - October 3, 2011

Deflating The Inflation via a Strong Dollar remains our Global Macro call. Get the US Dollar right, you get a lot of other things right. As we look at today’s set up for the S&P 500, the range is 44 points or -1.63% downside to 1113 and 2.26% upside to 1157.

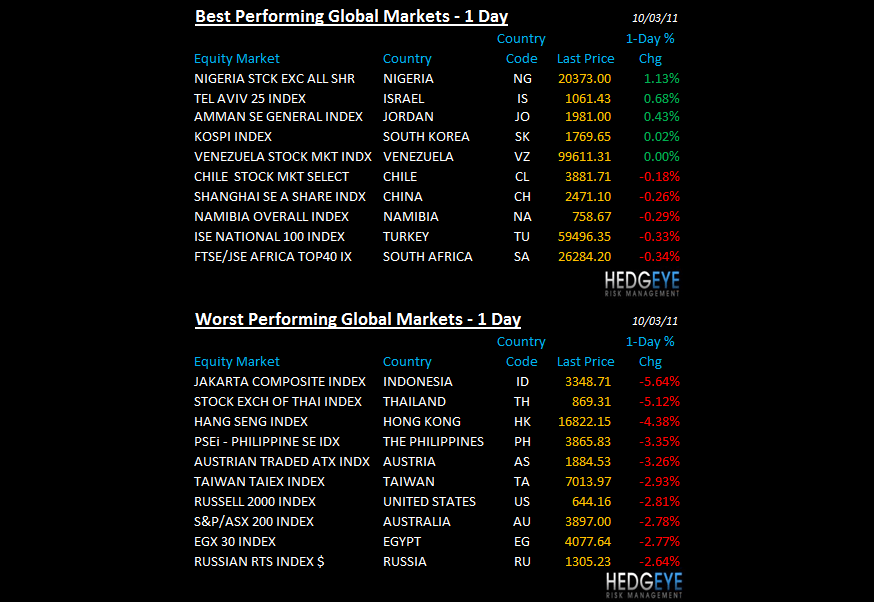

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -1836 (-3131)

- VOLUME: NYSE 1323.20 (+18.04%)

- VIX: 42.96 +10.61% YTD PERFORMANCE: +142.03%

- SPX PUT/CALL RATIO: 1.49 from 2.20 (-31.98%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 36.42

- 3-MONTH T-BILL YIELD: 0.02%

- 10-Year: 1.92 from 1.99

- YIELD CURVE: 1.67 from 1.72

MACRO DATA POINTS (Bloomberg Estimates):

- 7 a.m.: Fed’s Fisher speaks on CNBC

- 10 a.m.: Construction spending, est. (-0.2%), prior (-1.3%)

- 10 a.m.: ISM Manufacturing, est. 50.3, prior 50.6

- 11 a.m.: Fed to purchase $2.75b-$3.5b in notes/bonds

- 11 a.m.: Export inspections: corn, soybeans, wheat

- 11:30 a.m.: U.S. to sell $29b 3-mo. bills, $27b 6-mo. bills

- 1 p.m.: Fed’s Fisher speaks on Bloomberg Radio

- 6 p.m.: Fed’s Lacker speaks in Madison, Wis.

WHAT TO WATCH:

- European finance ministers meet in Luxembourg to consider how to shield banks from the debt crisis, boost region’s rescue fund

- Yahoo will hold 9 a.m. press conference; Alibaba Chairman Jack Ma said on Sept. 30 very interested in Yahoo, talks snagged over political issues

- Apple iPhone announcement tomorrow; watch for increasing speculation about iPhone 5 capability

- N.J. Gov. Chris Christie on brink of decision whether to seek Republican nomination for president

- Supreme Court’s term opens

- Congress returns from recess

- Anadarko (APC) won’t have to face personal-injury claims related to 2010 Gulf of Mexico spill, federal judge ruled

- Arch Coal (ACI) cut forecast for 2011 adjusted EPS

COMMODITY/GROWTH EXPECTATION

COMMODITIES – everyone and their brother knows Dr Copper is crashing now, and this is perpetuating weakness (down another -3.1% to start the wk making fresh lows at $3.05/lb). Every commodity in the Hedgeye model is now bearish TRADE and TREND, including Gold (TREND resistance $1680)

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- China Manufacturing Stability May Ease ‘Hard Landing’ Risks

- Raw-Material Bets Cut 26% in Biggest Rout Since ’08: Commodities

- Hedge Funds Cut Oil Bets Most in Seven Weeks: Energy Markets

- Shell Declares Force Majeure After Fire, Cancels Oil Supply

- Gold Rises for Third Day as Greek Debt May Spur Increased Demand

- Obama Said Poised to Submit Three Trade Accords to U.S. Congress

- Platinum-Gold Ratio Tumbles to Lowest Level Since at Least 1987

- Commodities Drop to 10-Month Low as European Industry Shrinking

- Copper Falls to 14-Month Low on Prospects for Demand to Weaken

- Crude Extends Declines in New York After Closing at One-Year Low

- European Goldfields Rises in London on $600 Million Qatari Loan

- Corn Extends Declines After Biggest Monthly Drop in Five Decades

- Oil Falls After Closing at One-Year Low as Europe Ministers Meet

- Petrobras Bonds Trailing Pemex on Higher Costs: Brazil Credit

- Palm Oil Tumbles to One-Year Low as Soybeans Drop on Stockpiles

- Copper Falls to 14-Month Low Before Manufacturing: LME Preview

- U.S. Mint American Eagle Silver Coin Sales Most Since January

- Freeport, Striking Peru Copper Miners to Resume Wage Talks Today

- U.A.E. Says World Oil Use Stable, No Risk of Plunging Demand

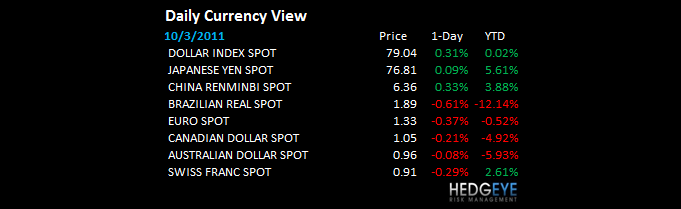

CURRENCIES

EUROPEAN MARKETS

GREECE – so they fibbed again… what does that matter in a globally interconnected game of risk where the entire construct of the EUR/USD pair continues to trade off of politics? Greece leads the headlines and Germany’s DAX broke my critical TRADE line of 5439 support again. Not good.

ASIAN MARKETS

ASIA – complete meltdown where markets were opened last night w/ Hong Kong leading the crashers on the downside (down -4.4% overnight; down 31% since April 8th); Thailand and Indonesia collapsed for -4.7% and -5.9% moves, respectively. Asian Growth Slowing.

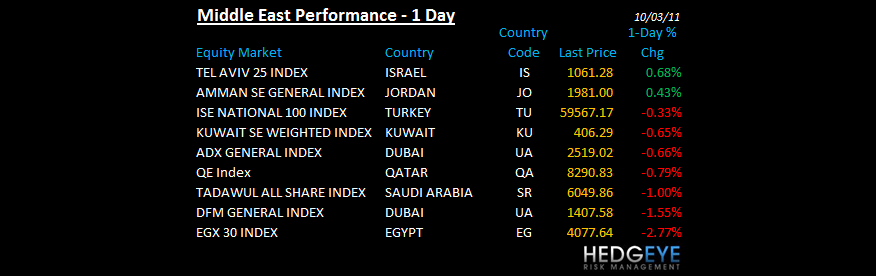

MIDDLE EAST

Howard Penney

Managing Director