Given that Darden preannounced its fiscal first quarter earnings earlier in the month, there were few surprises in yesterday's EPS release and nothing new to get me really excited to be long the stock. There are, however, a lot of things to think about, not only as it relates to DRI but also the consumer environment in general.

To me, DRI is the epitome of what is wrong with having exposure “Middle America” and the average consumer. In the current environment, in the restaurant space, if a company/concept in not “on trend” with a unique customer appeal there is going to be traffic and spending related issues. The easiest path to attracting more consumers for casual dining companies is through ever-better value offerings. The Olive Garden is set to begin advertising a half Panini sandwich, unlimited soup and/or salad for $6.95 in what is clearly a move to take some traffic from Chili’s.

My belief is that the average concept serving an aging consumer is consistent with a fundamentally-weak economy. Here, again, is my thesis for the consumer: no job growth, declining real income, Bernanke-inspired price volatility, declining stock prices, falling house prices, sticky gasoline prices, and zero confidence equals declining consumption.

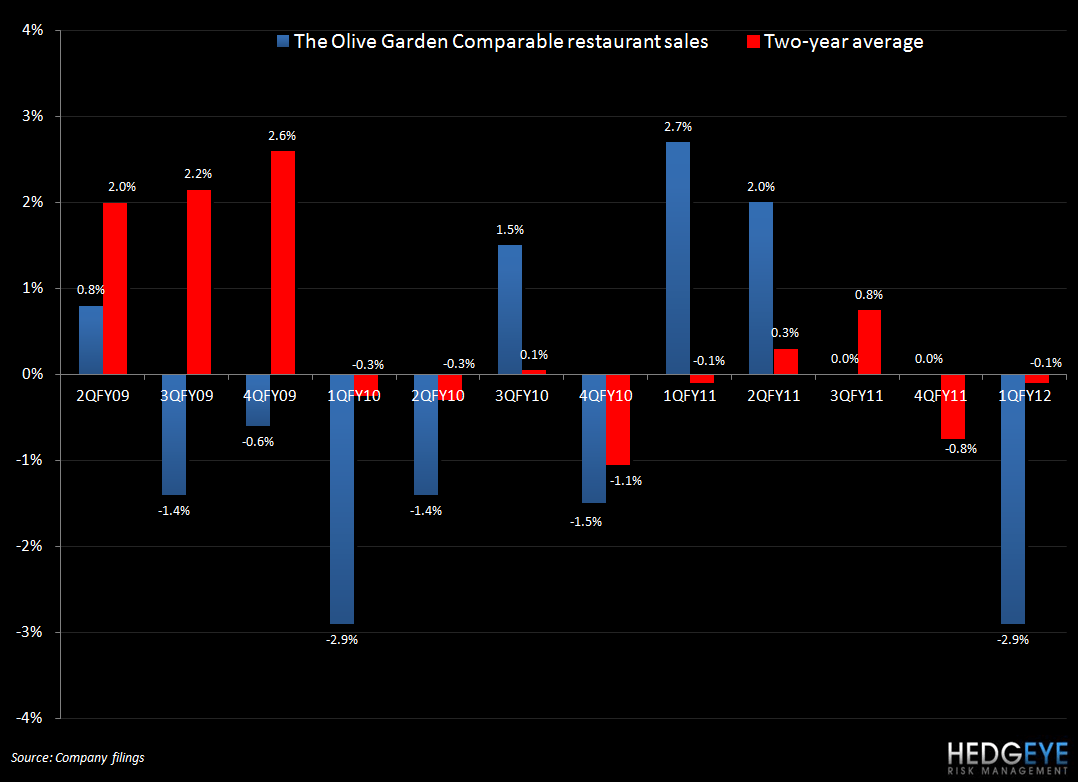

The Olive Garden is the poster child for some of these issues. The concept is generally very healthy, with very strong average unit volumes, but they are struggling to generate incremental traffic. There are some Olive Garden-specific issues. For instance, their asset base is weak with half of the units needing a major remodel; the fix is 6-12 months away and the advertising is somewhat stale and not driving new consumers to the concept.

Naturally, the company’s first response to immediately prop up sales is to offer lower prices to increase the value perception of the brand. To me that is a reaction or a defensive move not a proactive step in trying to bring in new or lapsed users.

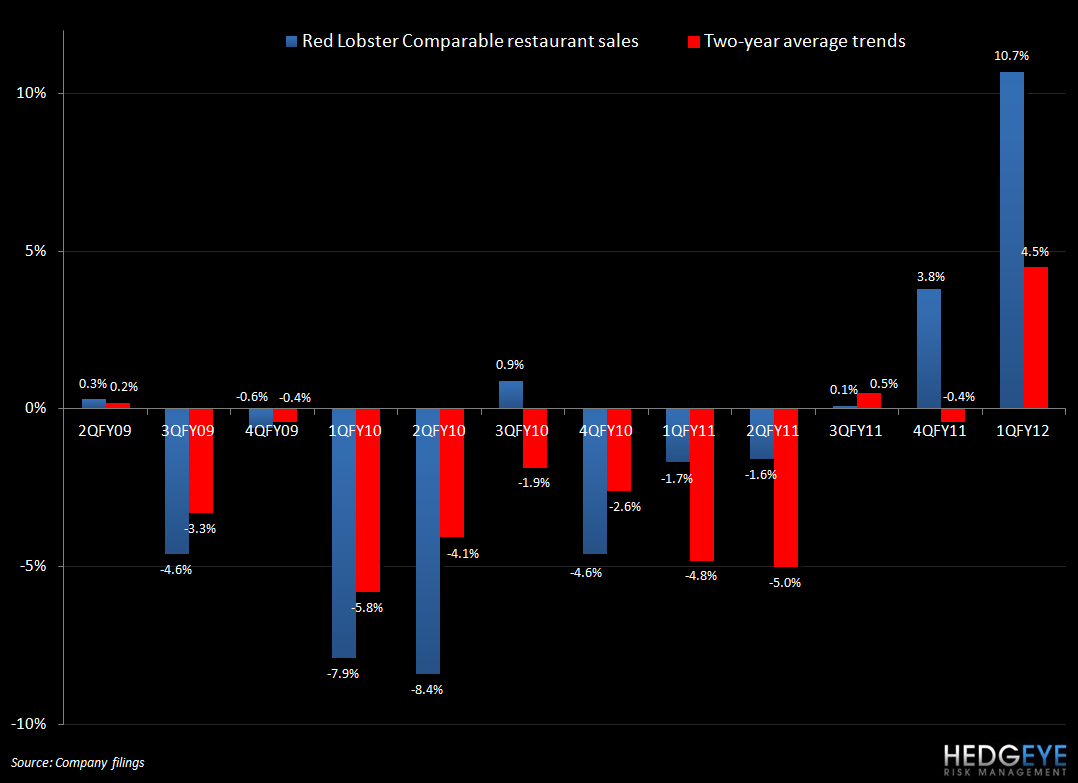

What I worry about most with DRI is the company resorting to too much discounting, as they have done in the past. I know it’s a different management team and Clarence Otis is Joe Lee’s apprentice but I think the $15 price point offer from Red Lobster this past quarter was disconcerting. I know management put their best foot forward with an acceptable rational for the promotion, but the memories of past Red Lobster discounting efforts are still fresh.

For 1Q12, sluggish same-store sales trends at the Olive Garden (reported -2.9%, with traffic down -2.2%), combined with higher commodity costs, resulted in lower year-over-year operating margins and earnings during the first quarter.

Higher than anticipated “check management” during the quarter (consumers, fatigued from macro pressures are purchasing fewer appetizers, drinks and desserts) put increased pressure on margins. Management attributed about one-third of the higher year-over-year food and beverage costs as percentage of sales to this increased “check management.”

DIFFCULT TO SWALLOW GUIDANCE

Darden maintained the fiscal FY12 guidance that it provided when the company preannounced first quarter earnings, including blended same-store sales growth of about 3% at Olive Garden, Red Lobster and LongHorn, operating margin growth and 12-15% earnings growth with “higher confidence at this point in the year in the low end of the range.”

Although these expectations are not out of reach, they rely on the fatigued consumer not being so fatigued. Most notably the company needs to see improved trends at Olive Garden, a moderating level of check management and more favorable commodity costs in the back half of the year. Not to mention the overall environment which relies on an economic recovery that Darden CEO Clarence Otis called “uneven and relatively anemic”.

Management would not provide any details about trends in September, outside of saying that they had “reason to be encouraged.” This was not enough to outweigh investors’ concerns, as evidenced by the stock’s performance yesterday.

If consumers are focused on affordability right now as management stated on its earnings call, and we continue to see a deceleration in overall consumer spending trends, I am not as confident as management that the current level of check management will moderate. As we have seen in the past, impacting many full-service concepts, customers tend to manage their checks lower in order to still dine out during tough economic times. This will likely continue to be a factor until we see steady improvement in the economy. Time will tell. As I wrote earlier, half of The Olive Garden’s store-base needs to be remodeled and that is not going to happen in 2012.

Another financial uncertainty for Darden stems from the company’s expectation for more neutral commodity costs during the second half of the year. Although trends will likely improve year-over-year as a result of easier comparisons, Darden’s guidance relies somewhat on declining costs from current levels. The company has contracted 80% of its commodity costs through the end of the calendar year but only 25% of its costs through the end of its fiscal year, which leaves the company’s income statement fairly exposed during the second half of the fiscal year.

Senior management made a bet that commodity prices will decline and it looks to be a smart move given the current trends.

CAN MANAGEMENT HIT THE 3% SSS TARGET IN 2012?

Turning the Olive Garden around is not going to be an easy and will take time. Management is focused on doing the right things such as improving the core menu and its advertising strategy and refreshing and remodeling its store base, but these steps all take time and trends could get worse before they get better.

The only immediate strategy to increase traffic is to offer lower priced menu options, or what management called “addressing affordability” in an effort to appeal to its customer base that includes a lot of people making less than $60K/year. Although lower prices could drive increased traffic, it will have a negative impact on margins and could permanently push Olive Garden’s average check lower. Given Olive Garden’s aging store base and cash-strapped customer base, I am not convinced the company will see any real improvement in same-store sales trends this year.

Relative to Darden’s full-year same-store sales guidance, if the company maintains the two-year average same-store sales growth trends at Red Lobster, Olive Garden and LongHorn that it achieved during the first quarter for the remainder of the year, it would imply same-store sales growth of about 2.7%, just shy of its 3% target.

So reaching this 3% guidance goal assumes an improvement at Olive Garden, as stated by management, but it also assumes continued momentum at Red Lobster and LongHorn. Given LongHorn’s consistently strong trends in the recent past, I would not be surprised to see the concept’s momentum continue at current levels.

Same-store sales trends at Red Lobster, however, improved nearly 500 bps on a two-year average basis during the quarter and I do not think this level of improvement is necessarily sustainable for the rest of the year. And, if Red Lobster cannot maintain +4.5% two-year average trends, Olive Garden’s performance will have to improve rather significantly on a two-year average basis to achieve 3% same-store sales growth.

Howard Penney

Managing Director

Rory Green

Analyst