THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP - September 29, 2011

With the Hedgeye 1182 TRADE line of support becoming resistance (again) for the S&P500, We have very little appetite to take on month-end markup or EuroPig rumor risk. Don’t forget that the average drawdown in the S&P500 in the first 6 days of the new month since April = -4.5%.

As we look at today’s set up for the S&P 500, the range is 64 points or -3.31% downside to 1113 and 1.73% upside to 1171.

SECTOR AND GLOBAL PERFORMANCE

We moved to 2/9 sectors positive on TRADE and 1/9 on TREND. XLU remains the only sector positive on both durations.

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -2079 (-4017)

- VOLUME: NYSE 1049.03 (-11.85%)

- VIX: 41.08 +8.94% YTD PERFORMANCE: +131.44%

- SPX PUT/CALL RATIO: 2.45 from 1.82 (+34.39%)

CREDIT/ECONOMIC MARKET LOOK:

Another one of the super secret surprises that the gods of Chaos Theory have imposed on Monsieur Bernank’s lap = rising rates at the short-end of the US Treasury curve with a brand new TRADE line breakout above the Hedgeye 0.20% line for 2-year yields. Long-end of the curve (yields) remain broken across durations, but rising real-rates on the short-end is not good for Gold (on the margin)

- TED SPREAD: 36.35

- 3-MONTH T-BILL YIELD: 0.02% +0.01%

- 10-Year: 2.03 from 2.00

- YIELD CURVE: 1.76 from 1.65

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30 a.m.: GDP 2Q, T, est. 1.2%, prior 1.0%

- 8:30 a.m.: Personal consumption 2Q, T, est. 0.4%, prior 0.4%

- 8:30 a.m.: Jobless claims, est. 420k, prior 423k

- 8:30 a.m.: Fed’s Plosser speaks on economy in Radnor, Penn.

- 8:30 a.m.: Net export sales, commods

- 9:45 a.m.: Bloomberg consumer comfort, est. -51.0

- 10 a.m.: Pending home sales, est. M/m -2.0%

- 10 a.m.: Business Roundtable releases 3Q economic survey

- 10 a.m.: Freddie Mac Mortgage

- 10:30 a.m.: EIA natural gas storage

- 11 a.m.: Kansas City Fed. Manufacturing, est. 3

- 1 p.m.: Fed’s Lockhart speaks in Atlanta

- 1 p.m.: U.S. to sell $29b in 7-yr notes

WHAT TO WATCH:

- Germany to vote on euro rescue fund, sets stage for next steps

- Microsoft is said to add Comcast, Verizon pay TV to Xbox Live

- Basel III to hurt European companies more than U.S., S&P says

- House meets in pro-forma session, expected to pass short- term continuing resolution, which funds government through Oct. 4 by unanimous consent

- Italian, Spanish and French market regulator extend short selling ban on financial stocks

COMMODITY/GROWTH EXPECTATION

COMMODITIES: free falling Copper prices now make headline "news", should be immediate-term oversold at $3.06/lb

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- Rare Earths Fall as Toyota Develops Alternatives: Commodities

- Shell Fighting Fire at Singapore Refinery After Blaze Surges

- LME Says ‘Expressions of Interest’ Exceed 10, Board to Meet

- Saudi Crude for Fuel Oil Nearing 22-Month High: Energy Markets

- Copper, Industrial Metals Decline as European Risk Hurts Demand

- Commodities Rebound, Paring Worst Quarter Since 2008 on Germany

- Oil Fluctuates as It Heads for Biggest Quarterly Drop Since 2008

- Crude Oil Climbs Ahead of German Vote on European Bailout Fund

- Yancoal Studying More Than $1 Billion in Australian M&A

- Alumina Gains on Speculation Company May Be Takeover Target

- Singapore Middle Distillates May Rise After Shell Refinery Fire

- Denmark Creates Rescue Fund for Crisis-Hit Farming Industry

- Freeport McMoRan’s Peru Copper Miners to Strike Over Wages

- Copper Falls 5.9% to $6,824.75 a Ton in London

- Palm Oil Declines on Concern Global Slowdown May Hurt Demand

- China Seen Needing ‘Huge Effort’ to Meet Increasing Corn Demand

- Commodities Head for Biggest Quarterly Drop Since 2008 on Debt

- World Slump Seen Triggered by European Breakdown in Global Pollt

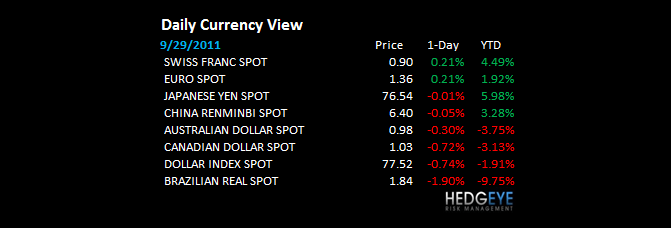

CURRENCIES

EUROPEAN MARKETS

EUROPE: hope reigns into the Bundestag vote with Germany hanging tough above my immediate-term TRADE line of support (5439 DAX)

- Eurozone Sep Economic Sentiment 95.0 vs consensus 96.0 and prior revised 98.4 from 98.3

- Eurozone Sep Consumer Sentiment (19.1) vs consensus (18.9) and prior (16.5)

- Eurozone Sep Business Climate (0.06) vs consensus (0.11) and prior revised 0.06 from 0.07

DAX – bullish TRADE, bearish TREND setup continues to hold up for the Germans in the immediate-term as my 5348 TRADE line of support continues to hold. The refreshed range (immediate-term) for DAX = 5, so the squeezage from here is defined at +2% left on the upside. Rock solid unemployment report of 6.9% in Germany this morn for September (vs 7.0% AUG) notwithstanding.

ASIAN MARKETS

Surprisingly strong session for Asian Equities last night! That doesn’t mean that China/HK/KOSPI/Japan/etc aren’t crashing anymore; it just means that bear markets bounce: Nikkei +1%, KOSPI +2.7%, India +0.9%.

MIDDLE EAST

Howard Penney

Managing Director