Last week, commodities continue to be pressured by a combination of the strengthening dollar and mounting concerns about economic growth.

STOCK TAKEAWAYS

- Declining grain prices (corn in particular) are bullish for restaurant industry margins as it is bearish for protein prices. In particular, this is a positive for TSN and SAFM

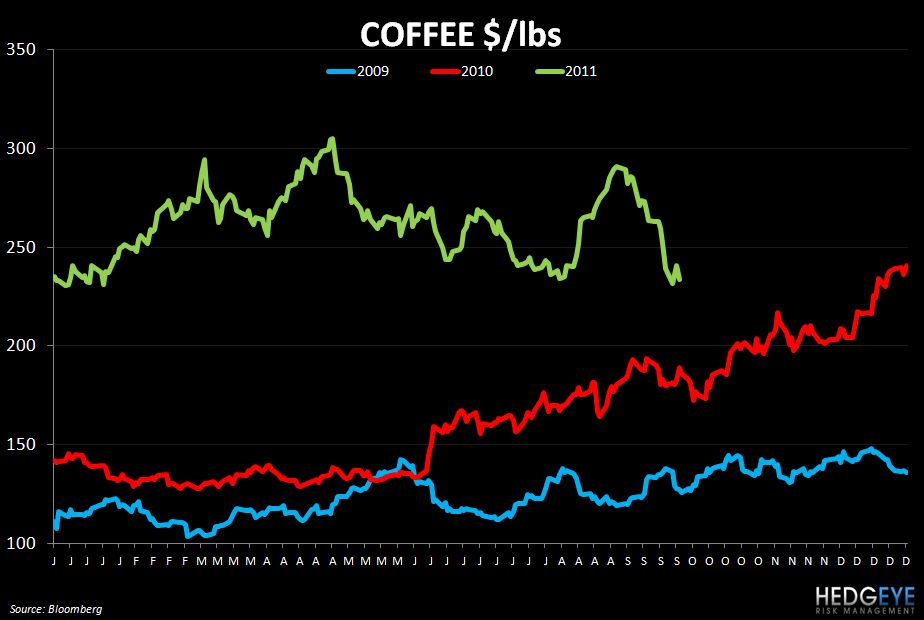

- Coffee prices have declined dramatically over the last month, perhaps indicating that further price hikes from the coffee concepts – SBUX, DNKN, PEET, GMCR, CBOU and THI – are unlikely. Higher retail prices may remain, however, as inventory acquired at high prices is worked through.

- Chicken Wing prices are heading sharply higher, which is a concern for BWLD at a time when economic growth is a concern and the company is stepping up expansion into new markets.

- Dairy prices moved marginally higher but, on a year-over-year basis, cheese prices remain down which is a positive for CAKE, DPZ YUM and PZZA, especially considering the level cheese prices were at just a few weeks ago.

SUMMARY

Chicken wings, beef and dairy were the only items in our commodity monitor that saw price gains versus last week. The declines in our weekly monitors were far larger than the advances; as the table below shows, grains, coffee, and chicken broilers all saw significant losses in price week-over-week. In theory, this is a good thing for restaurant companies especially given the price increases that Starbucks and others have had to implement to protect margin. The reality remains, however, that much of the softness in commodities at the moment is due to concerns over the global economy. If these fears are justified, the implied softness in the sales environment would effectively offset any benefit from lower input costs.

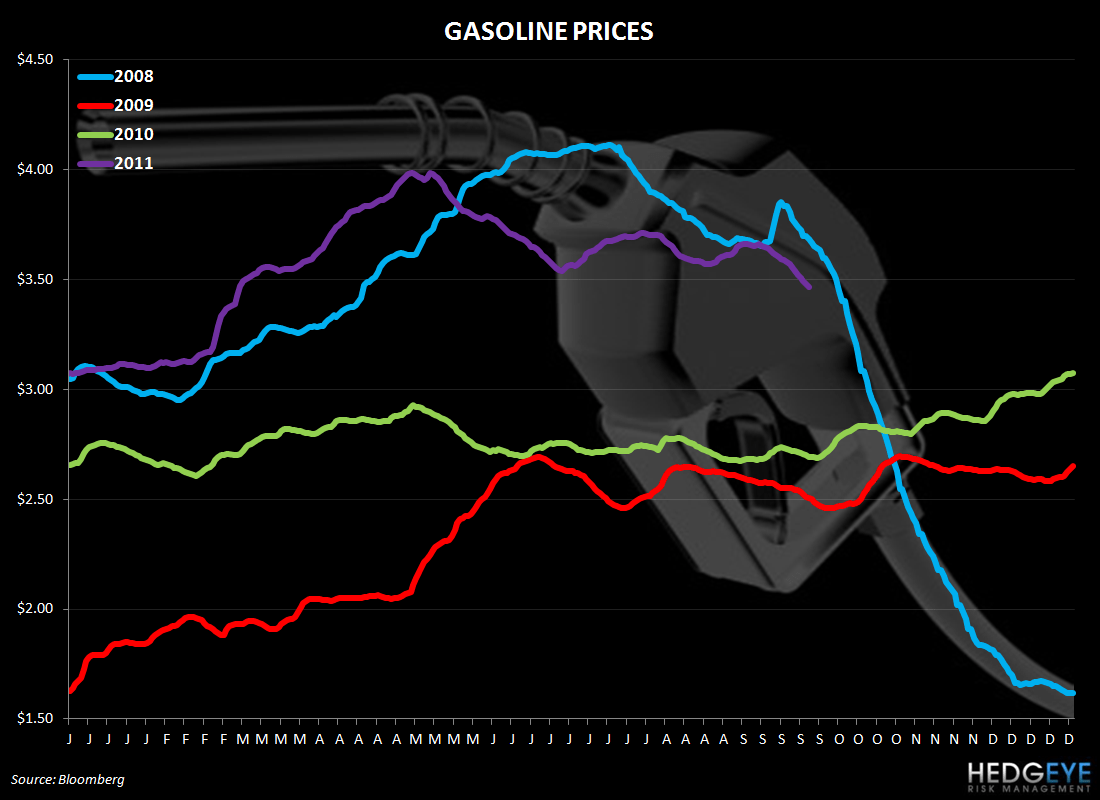

Last week, commodities continue to be pressured by a combination of the strengthening dollar and mounting concerns about economic growth. Brent crude declined almost 6% over the last week as gasoline prices also dropped week-over-week, which is generally a positive for restaurants on the margin. That said, the chart below shows that gasoline prices plummeted in 2008 as the recession struck. Commodities are again sinking lower here in 2011 as the European sovereign-debt crisis threatens to derail the global economy.

CORN

Corn dropped 8% versus last week. This is a positive data point for the restaurant industry as a whole, not only companies with direct exposure to corn costs. As corn costs come down, that offers some relief to protein producers that can take advantage of the resulting decline in feed prices. Despite smaller supply from the U.S., demand concerns are acute enough to lead prices lower.

Below is a selection of comments from management teams pertaining to grain prices from recent earnings calls.

PNRA (7/27/11): “Just to note on the cost of wheat, in 2011 overall, the per-bushel cost will be about the same as 2010 due to our laddering purchasing strategy.”

“We are going to take price in the fourth quarter. This price will offset dollar for dollar the per-bushel inflation of wheat of approximately $3 a quarter that we're going to see in the fourth quarter of this year and then across next year”

“We do continue to expect significant inflationary pressures in 2012, 4% to 5% food inflation, $10 million of unfavorability on wheat costs, which means that we don't expect operating margin much better than flat to full-year 2011 in 2012.”

HEDGEYE: Weak global demand and a stronger dollar are currently trumping the adverse impact on supply due to weather and fires in the U.S. Slowing demand may also mean lower sales for PNRA, so it remains to be seen if margins improve from this effect, even if high wheat costs come down.

DPZ (7/26/11): “We're fairly locked in on our chicken, locked in on our wheat into – partway into next year.”

PZZA (8/4/11): “We're actually covered through Q1 from a contract standpoint. So from a supply chain disruption or even significant price impact we don't anticipate anything between now and the end of the year.”

COFFEE

Coffee prices declined -7.3% as the dollar gained 1% over the same period. Kraft Foods and J.M. Smucker have already cut prices as coffee prices slump but the supply and demand dynamic point to possible continuing softness in price. According to Bloomberg, farmers from Vietman to Brazil are expected to supply a record robusta crop in the marketing year that begins next month. SBUX had bought most of its coffee needs for the year ending September 2012 earlier this year, according to management commentary on its most recent earnings call in July. This could mean that retail prices take some time to adjust as inventory is processed.

Below is a selection of comments from management teams pertaining to coffee prices from recent earnings calls.

PEET (8/2/11): “As we indicated, in our first quarter call, we had to buy a small amount of our calendar 2011 coffee beans at significantly higher prices and this coffee will roll into our P&L during the third and fourth quarter.”

“Higher priced coffee resulted in gross margins this quarter being 290 basis points below prior year. In our first quarter conference call, we indicated that in addition to the overall higher price coffee market, we had to buy a small amount of coffee this year at significantly higher prices. And as a result, we expected our coffee cost to be 40% higher in fiscal 2011.”

HEDGEYE: Peet’s is a company with a very competent management team that manages coffee costs extremely well. Its higher-end, loyal customer base makes the price elasticity of demand more inelastic than for other coffee concepts’ products.

SBUX (7/28/11): “As I mentioned earlier, are absolutely a headwind for us in the full business and that's most acutely impactful on margins in CPG as it's a much more coffee intensive cost structure, as you know. I can tell you that the decline as I spoke about it earlier from about 30% operating margin in CPG this year down to the target 25% next year is really all explained by commodities. Absent commodity inflation we'd be at or improving our margin in the coming year.”

“As we had anticipated, in recent weeks, coffee prices have retreated significantly from a high of more than $3 per pound just a couple of months ago to levels now near $2.40 per pound. As prices have been falling we continue locking up our needs for fiscal '12 and now have virtually the full year price protected.”

HEDGEYE: Starbucks is aligning itself with the right partners to gain more control of its coffee costs to provide investors with more certainty going forward and to protect its margins as global coffee demand continues to rise.

GMCR (7/27/2011): “However, what we've said is that should coffee prices or other material costs spike, we will certainly consider price increases as necessary. We certainly hope that we do not have to cover one again next year. But our objective long-term is attempting to maintain our gross margin as we would see input costs come along.”

HEDGEYE: GMCR hedges out 6-9 months in advance. Strength in the dollar has helped bring coffee prices lower but whether or not dollar strength will continue or not will be a significant factor in future price action in coffee. Growing demand, globally, is bullish for coffee prices over the long term.

CHICKEN WINGS

Chicken wings gained 4.3% after last week’s 7.2% gain in another down week for commodities. This is definitely a concern for BWLD at a time when the top-line environment is becoming more difficult and the company is expanding its footprint into new markets.

Howard Penney

Managing Director

Rory Green

Analyst