Reebok’s Toning settlement should be taken into context. While it never appeared to us to be a sustainable biz, it did shift share around a bit. The trend has been self-correcting for 11-months now. So we’re not concerned about it ‘going away.’ In fact, a simple look at Nike’s US order book tells us where these toning dollars are going.

Reebok’s $25mm settlement with the FTC over unsubstantiated claims on the technology behind its shoes this morning is raising questions over the ‘category’s’ sustainability. The stocks are not moving meaningfully on this, nor should they. But here’s some context to the extent that people get loud (as CNBC did – saying that there’s $1Bn at risk) on the issue. Consider the following:

- The toning trend started with Skechers Shape-Ups in early 2009. Within 6-months Reebok joined the party with its Easy Tone shoes and hefty advertising budget, which ultimately drove accelerating demand by the Fall of ’09. From late ’09 to early ’10 there were several marginal players entering the fray (Ryka, Puma, etc.), but this was really a two horse race from beginning to end with market share for SKX and Reebok at roughly 60/40 respectively. Nike stayed out of it entirely, referring to it as a gimmick. We are in print, and on TV, in saying that “selling shoes to a person who wants a shoe to get them in shape while they walk to and from the couch to the refrigerator to get bon bons and beer is hardly a sustainable model.”

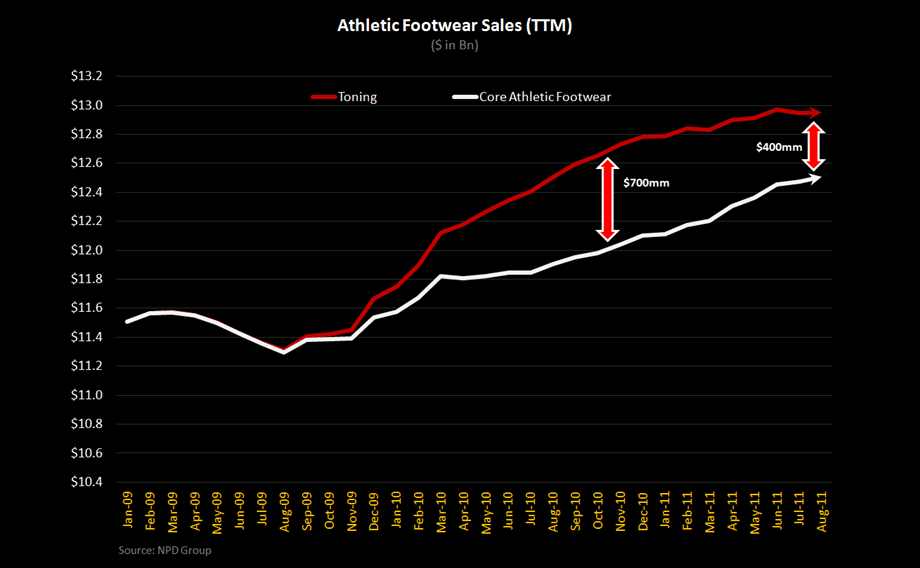

- At its peak in mid-2010, we estimated toning to be just over a $1Bn category domestically and roughly $500mm internationally, at retail.

- At that time, the toning category was contributing up to 4%-6% to overall footwear sales growth in the athletic specialty channel. This benefit was fleeting. By October 2010, the category was a drag on consolidated growth in the industry as demand slowed abruptly. Meanwhile, the industry excluding toning was growing at a rate from mid-single-digit to low-double-digit.

- With Skechers and Reebok left severely over-inventoried heading into the shift in demand, the discounting began. With prices for toning shoes still now at roughly half of where they sold at the peak, the category has contracted to a what is now a ~$500mm category domestically – similar in size to categories like occupational and cold weather casual boots.

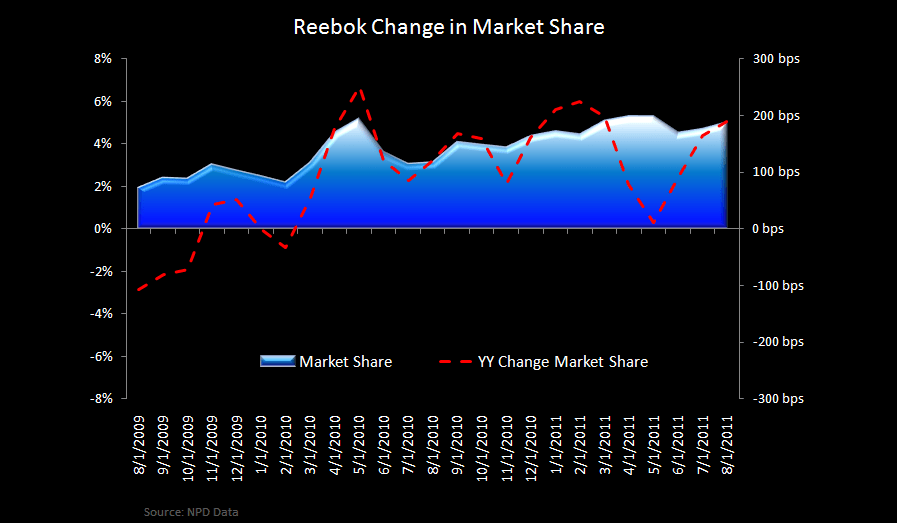

- What is perhaps the most notable callout throughout what can now be dubbed as the ‘toning fad’ is Reebok’s ability to leverage the trend to regain relevance. Take a look at the two charts below illustrating both Reebok and Skechers’ market share gains both during, but more importantly following the toning cycle. SKX gained 4 points of share in the industry only to give it all back to ‘real’ innovation leaders like Nike and Adidas. Reebok on the other hand gained 2-3 points of share initially and has continued to take share as it rolled its success directly into its latest ZigTech offering.

- Keep in mind that Skechers started from a larger base (6% share of the industry) with its stable brown shoe and growing kids business while Reebok represented an inconsequential 2% of the industry. For what it’s worth, they both now have about a 6% share.

At this point, there’s definitely a risk that Skechers is forced to pay a similar settlement to the FTC for its own advertising claims. Is it going to move the needle for the company, no.

From an industry perspective, we are a month away from the point when comping toning growth is an afterthought. In fact, over the last two quarters, footwear and sporting goods retailers alike have noted that the benefit of the latest lightweight running category has more than offset the impact of lost toning sales. The industry has moved on, so should we.

Casey Flavin

Director