THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP - September 28, 2011

EMBRACE UNCERTANITY!

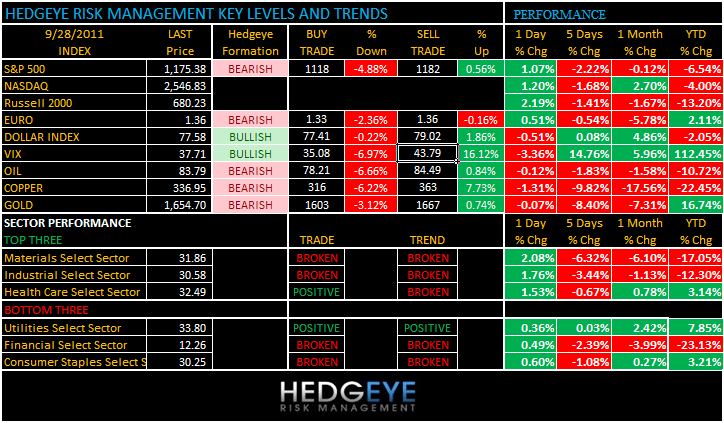

Yesterday was a really close confirmation of another immediate-term TRADE breakout (within a bearish TREND and TAIL) of the SP500. As we look at today’s set up for the S&P 500, the range is 64 points or -4.88% downside to 1118 and 0.56% upside to 1182.

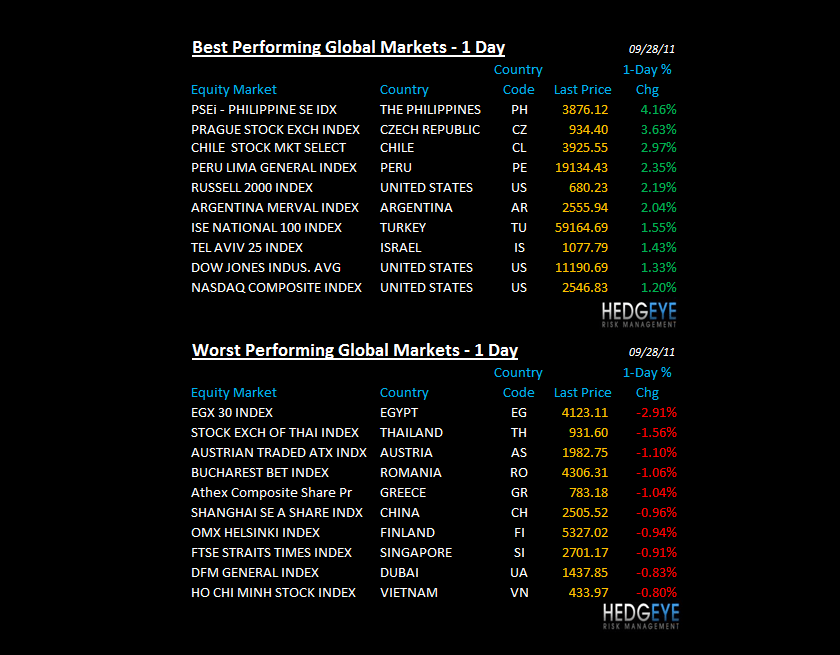

SECTOR AND GLOBAL PERFORMANCE

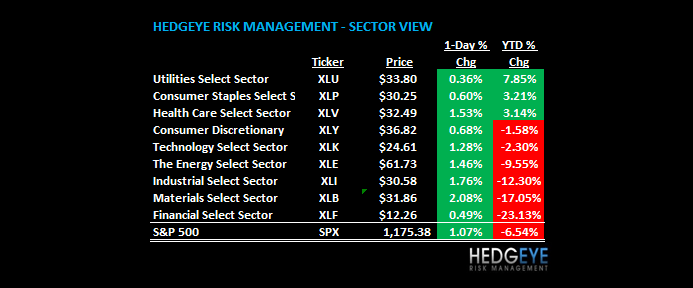

TRADE, TREND, and TAIL lines for the SP500 remain broken as long as 1182 SPX does. Only 1 Sector of 9 is bullish TRADE and TREND - (Utilities XLU). Of the 8 of 9 Sectors that remain bearish TREND, Financials (XLF) still look the worst followed by Basic Materials (XLB) and Consumer Staples (XLP).

The Consumer Staples risk continues to evolve as the US Dollar’s strength does; FX risk is a trivial headwind for EPS. If 1182 (SPX) is overcome and the Greeks and Italians jump over the moon, everything should be fine into month-end.

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 1938 (+537)

- VOLUME: NYSE 1190.10 (+2.83%)

- VIX: 37.71 -3.36% YTD PERFORMANCE: +112.45%

- SPX PUT/CALL RATIO: 1.82 from 1.86 (-2.02%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 35.51

- 3-MONTH T-BILL YIELD: 0.01% -0.01%

- 10-Year: 2.00 from 1.91

- YIELD CURVE: 1.75 from 1.66

MACRO DATA POINTS (Bloomberg Estimates):

- 7 a.m.: MBA Mortgage, est. -0.2%

- 8:30 a.m.: Durable goods, est. -0.2%

- 10:30 a.m.: DoE inventories

- 1 p.m.: U.S. to sell $35b 5-yr notes

- 5 p.m.: Fed’s Bernanke speaks in Cleveland. Prepared text, Q&A

WHAT TO WATCH:

- Amazon.com hosts press event, said to announce new tablet device. Watch for details on who may sell it, parts suppliers, pricing

- President Obama’s $447b jobs plans would help avoid return to recession: Bloomberg economist survey

- Boston Fed President Rosengren called for more govt efforts to help homeowners refinance mortgages

- President Obama participates in an “Open for Questions” roundtable at White House, 11:25 a.m.; delivers annual back- to-school speech at Benjamin Banneker High School in Washington, 1:30 pm

- N.J. Gov. Chris Christie said he plans to sit out the 2012 presidential race

- U.S. nuclear regulators meet for a second day to consider Southern’s request to build two reactors at its Vogtle plant near Augusta, Georgia

COMMODITY/GROWTH EXPECTATION

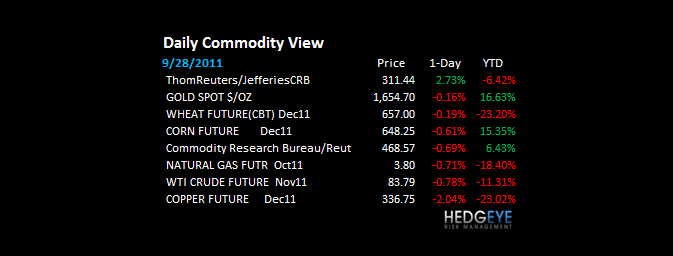

COPPER – Dr Copper can teach us a lot, if we are willing to re-learn; you’d think that a 1-day short squeeze in everything commodities would see more than a day of follow through – not so much; Copper down another 2% this morning and crashing.

GOLD: we sold it yesterday, keeping Friday's trade a trade; immediate-term downside to $1603 $GLD

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- LME Takeover Bids Mean Most at Stake for Goldman Sachs, UBS

- Coffee Falls in Rout as Starbucks Cup Costs $1.50: Commodities

- Chaoda Faces Second Hong Kong Market Misconduct Hearing Today

- Gold May Gain in London on Physical Purchases, Europe Concern

- Oil Falls, Heading for Quarterly Decline on Europe Debt Crisis

- Russian Oil to Fall as Tax Spurs Urals Exports: Energy Markets

- BP May Quadruple Indonesian Gas Plant as Part of Asian Drive

- Commodities Drop, Deepening Quarterly Decline, on European Risk

- Wrong Reasons Hurt Corn, Says UN, as Morgan Stanley Bullish

- Russia Expands Ports to Regain Wheat Export Advantage: Freight

- Commodities Rise Most in Four Months as European Concerns Ebb

- Spot Gold, Gold Futures Resume Decline on Europe Crisis Efforts

- Oil Surges Most in Four Months on European Debt-Crisis Efforts

- Dairy Has Greater Resilience in Slowdown, New Fonterra CEO Says

- Ship Owner Losses Persist on Glut as Mine Profits Boom: Freight

- Gold Climbs Most in Seven Weeks as Commodities, Equities Rally

- Aluminum Product Shipments by Japan Drop for Third Month

- Billionaire Ross Says Ship Deals to Accelerate After Slump

- Typhoon Nesat Kills 20 in Philippines, to Hurt Rice Harvest

CURRENCIES

FX: Euro/USD has a wall of resistance between here (1.36) and its broken TAIL line of 1.39

EUROPEAN MARKETS

Thanks for the timing on this - “BOE's Financial Policy Committee says Britain's banks face "materially" increased risks from the euro zone debt crisis; recommended that banks should take any opportunity they had to strengthen their levels of capital and liquidity”

EUROPE: sketchy situation developing with DAX recovering my TRADE line of support and CAC and MIB failing at it.

GREECE: lots of rumors; no market support for them - Greek stock market hitting fresh YTD lows here this morning (down -55% since FEB)

FINLAND: important market to watch today in Global Macro as they vote on Euro-TARP bazooka; early read through not good - Finland down -1.5%

FRANCE: no GDP growth in Q2 (reported at 0.0% q/q). No way for these politicians got their forecasts right if they are this wrong on growth.

ASIAN MARKETS

ASIA: Hang Seng (which we're short) down -26% since the April highs; Korea crashing obviously as well (down -23% since May)

ASIA: very bearish follow through from European and American hope rally yesterday with China, KOSPI, and HK all down in response.

MIDDLE EAST

Howard Penney

Managing Director