THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP - September 27, 2011

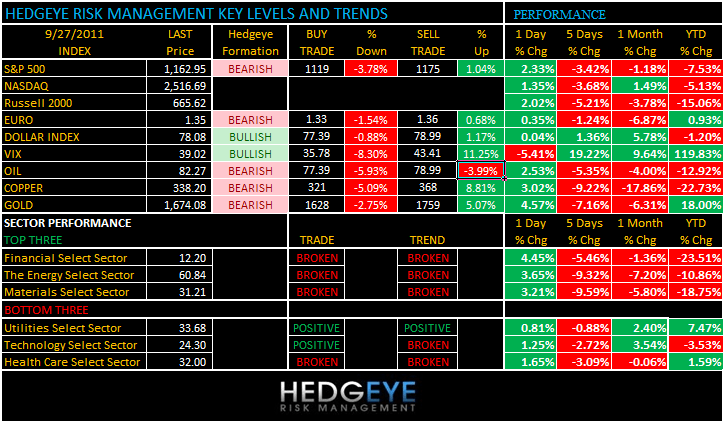

Another short squeeze into month-end; fancy that. As we look at today’s set up for the S&P 500, the range is 56 points or -3.78% downside to 1119 and 1.04% upside to 1175.

SECTOR AND GLOBAL PERFORMANCE

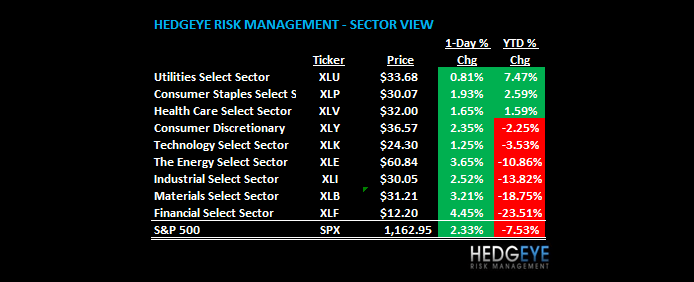

Some central planners would hope that a day like yesterday would solve all of the world’s problems. Hope, unfortunately, is not a risk management process. The Top 3 Sectors in the US equity market today were the 3 that still look the worse from their closing prices (Financials, Basic Materials, and Energy).

In the end, Strong Dollar = Strong America, because it Deflates The Inflation. And you are starting to see that in the daily divergences with Consumer Discretionary and Technology looking 2nd and 3rd best, respectively, next to Utilities (the only Sector that’s bullish TRADE and TREND).

The other 6 of 9 Sectors remain bearish on both TRADE and TREND durations. We shorted Consumer Staples (XLP) yesterday as it broke last week and the international companies in the ETF are going to face FX headwinds in the coming quarters if we continue to be right on the Strong Dollar position (USD).

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 1401 (+601)

- VOLUME: NYSE 1157.38 (-5.89%)

- VIX: 39.02 -5.41% YTD PERFORMANCE: +119.83%

- SPX PUT/CALL RATIO: 1.86 from 1.31 (+41.91%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 35.77

- 3-MONTH T-BILL YIELD: 0.02% +0.01%

- 10-Year: 1.91 from 1.84

- YIELD CURVE: 1.66 from 1.61

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45 a.m./8:55 a.m.: Weekly retail sales from ICSC/Redbook

- 9 a.m.: S&P Case-Shiller, July, est. M/m 0.1%, prior -0.06%

- 10 a.m.: Consumer Confidence, Sept., est. 46.0, prior 44.5

- 10 a.m.: Richmond Fed Manufact. Index, Sept., est. -11, prior -10

- 11:30 a.m.: U.S. to sell 4-week bills

- 12:30 p.m.: Fed’s Lockhart speaks on economy in Jacksonville, Fla.

- 1 p.m.: U.S. to sell $35b 2-yr notes

- 1:20 p.m.: Fed’s Fisher speaks in Dallas, Texas

- 4:30 p.m.: API inventories

WHAT TO WATCH:

- Treasury Secretary Geithner predicts European governments will step up response to debt crisis after chiding from counterparts around the world, in comments on ABC last night

- Goldman Sachs said to consider deepening cost-cutting, may lead to additional job losses: NYT

- Google+ U.S. visits up 13-fold last week after site opened to the general public: Experian Hitwise

- Oracle may make more deals to buy industry-specific software makers, CEO says

- Liberty Media wants to buy Spain’s Telecable, Expansion reported; other bidders said to include CVC Capital, Ono, Carlyle Group

- Blackstone tops list of most active private-equity firms, with deals valued at $20.3b, according to data compiled by Bloomberg, followed by Avista Capital at $14.2b

- Oneok Partners (OKS) sees net income $740m-$800m in 2012, up from forecast 2011 earnings of $630m-$660m

- Priceline.com (PCLN) appointed former Microsoft executive Darren Huston as CEO of its Booking.com unit

- Watson Pharmaceuticals (WPI) introduced generic version of Warner Chilcott’s (WCRX) Femcon female contraception tablets

COMMODITY/GROWTH EXPECTATION

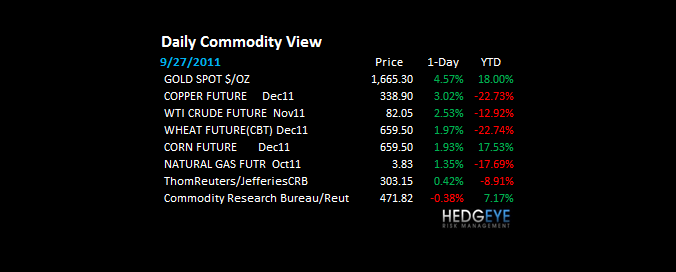

It felt like an investor in Gold yesterday (a trader who was underwater from his Friday Gold purchase), but I’m smart again today! With an +8% rally “off the lows” in Gold (a +22% move in Silver!) is just another day at Bernanke’s price stability casino. Copper and Oil both seeing their dead cat bounces this morning but TRADE lines of resistance for both are well established overhead at $84.98 and $3.68, respectively.

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- JPMorgan Differs With JPMorgan on Apple IPad Order Research

- VW Soups Up Golf for Twice the Price After Phaeton Flop: Cars

- Galvin Brothers Garner U.K. Chefs’ Award for City Restaurant

- Starbucks Sevenfold Gain Over S&P 500 Fuels Put Buying: Options

- Cavalli Chief Sees Luxury-Goods Slowdown as Debt Crisis Deepens

- Family Dollar Investors Bet on Sale as Shorts Flee: Real M&A

- Li & Fung Advances After Billionaire William Fung Buys Shares

- German Consumer Confidence Will Hold Steady in October, GfK Says

- Universal Entertainment to Invest $2.3 Billion in Manila Casino

- China Yurun Food Advances by Most in Three Weeks in Hong Kong

- Goodman Fielder to Raise A$259 Million With Entitlement Offer

- MillerCoors Claims New England Patriots Broke Sponsorship Deal

- Netflix Gets 57% Cheaper for Amazon-to-Google Acquirer: Real M&A

- Tesco Cutting Price Gap With Asda, Not Starting Price War: BofA

- Nestle Borrows at 4-Year Low as KitKat Maker Favored in Crisis

- Porsche at $213,000 Belies Singapore Slowdown: Chart of the Day

- Lego Prepares for Global Economic Decline, Borsen Reports

- Yurun Plunges Most in Six Years After Saying Profit May Fall

- Kodak Declines After Drawing $160 Million From Credit Line

- Clorox Drops After Carl Icahn Withdraws Slate of Directors

CURRENCIES

EUROPEAN MARKETS

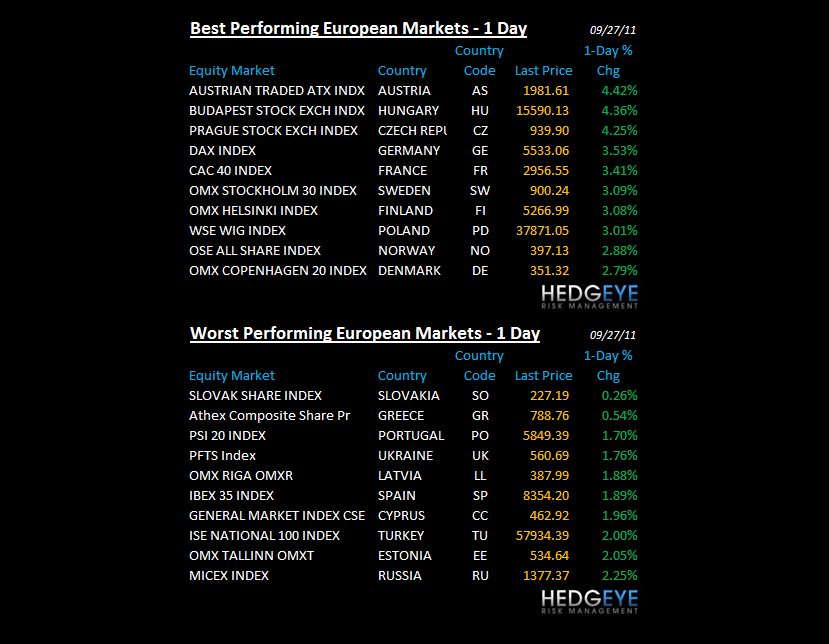

GERMANY – day 3 of a +6-7% short squeeze in German stocks from their YTD lows (after crashing -33% since May), but if the DAX can hold its head above 5441, it will have conquered its immediate-term TRADE line of resistance. That would be bullish (on the margin) and that’s why I don’t have any European shorts on right now (currency or equities). Wait and watch here as the CAC’s TRADE line is 3042; Greece up small.

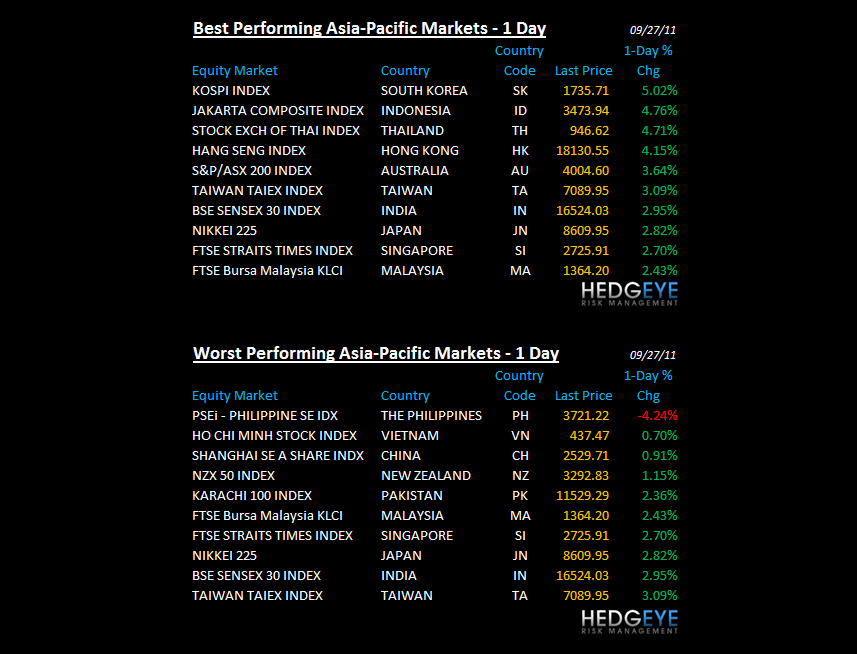

ASIAN MARKETS

ASIA – huge squeeze in the Asian equity markets that literally went down in a straight line last week (KOSPI +5%, Indonesia +4.8%, HK +4.2%, etc), but all of these markets remain in Bearish Formations with KOSPI and HK TRADE lines of resistance = 1799 and 19476, respectively.

MIDDLE EAST

Howard Penney

Managing Director