FINL reported its Q2 numbers of $0.39 after the close coming in a penny above consensus and our estimate of $0.38E. Despite considerably higher than expected sales on comps of +11% vs. 8.5%E, earnings upside was muted by increased SG&A spend. While this report is likely to be overshadowed by yesterday’s significant market decline and Nike’s blowout earnings, here are a few key takeaways from the quarter ahead of this mornings’ call:

- Despite concerns that FINL sales caught the July/August malaise in its entirety based on the timing of its quarter compared to FL (quarter ended in July), comps came in well above expectations. Yes, FINL is still a small fish compared to FL (a name we like better), but this is an unquestionably positive read-through as it relates to continued strength in the athletic specialty channel.

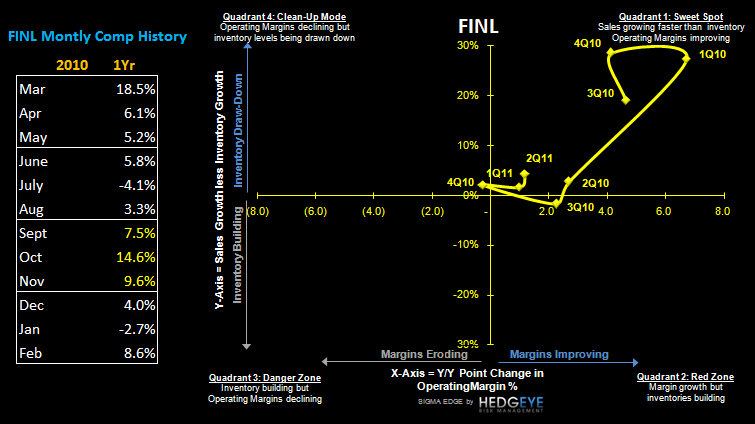

- In addition, inventories came in up +6% on 10% growth in sales and appear relatively clean. The strength in comps plus lean inventory levels are particularly bullish as it relates to the sustainability of Nike’s US futures, which came in +15% last night. It’s also worth noting that the company has kept the sales/inventory spread consistently positive and stable at +MSD since its ‘little hiccup’ this time last year.

- Gross margins up +195bps was solid but not surprising given the leverage in the model with higher merchandise margins likely augmenting occupancy leverage.

- FINL’s use of its balance sheet to drive shareholder value is another callout.

- The company acquired an 18 store specialty running chain (for $8.5mm) to grow the business – a move we think also bolsters FINL’s credibility as a leader in running.

- It also repurchased 2.1mm shares (~4% of total) while maintaining $5.40/share in cash and another ~4mm left on its authorization that the company can utilize to accelerate earnings growth.

- Lastly, the latest read on initial September month-to-date comps are bullish up +9%. While notably higher than +4% expectations in Q3, it’s important to keep in mind that October and November comps get a bit tougher (see chart below).

The call is @ 8:30am .

Casey Flavin

Director