DNKN has been the best performing QSR name over the past week, rising 10%. It probably will not surprise you to learn that a multi-day DNKN franchise convention was wrapped up yesterday in Boston.

We are hearing that the franchisees will now be selling Keurig coffee machines in their stores later in the fall. The retail price will be $119.00, allowing the franchisee to make about $40 for every machine sold.

Importantly, current same-store sales trends are estimated to be running at around 3-5% for 3Q11. My guess is that this will be a somewhat disappointing quarter as its represent little improvement in two-year trends from the 3.8% posted last quarter.

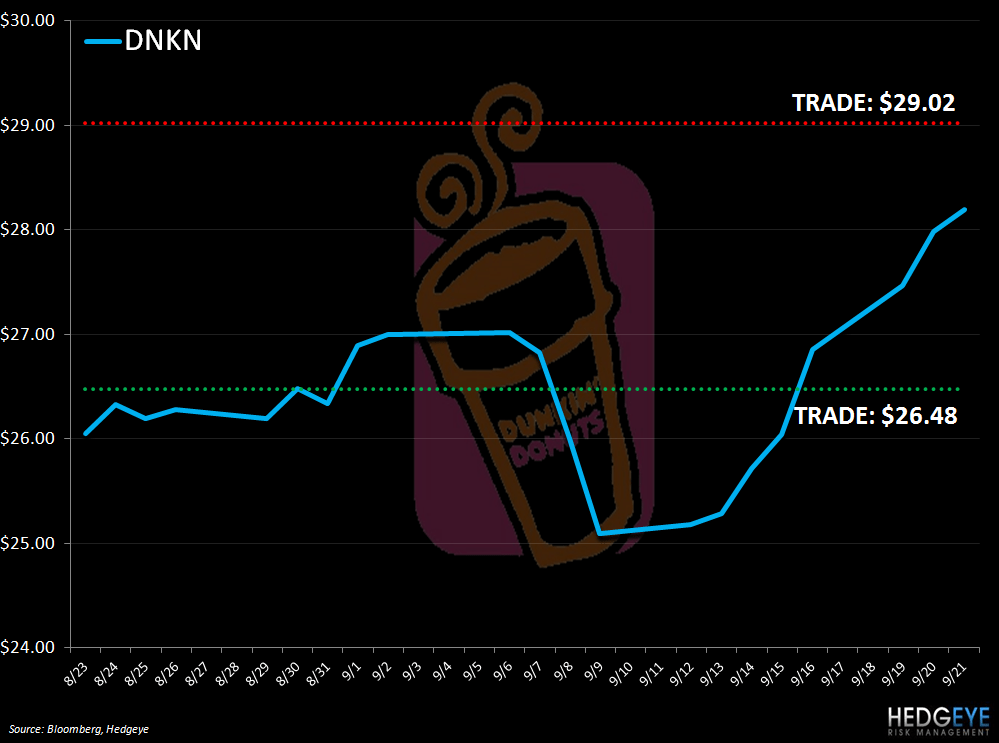

Keith re-shorted DNKN again today in the Hedgeye Virtual Portfolio. The hoopla around the franchise convention is over and SSS are not accelerating significantly, especially given the rollout of K-Cups in the stores.

Howard Penney

Managing Director

Rory Green

Analyst