TODAY’S S&P 500 SET-UP - September 19, 2011

As we look at today’s set up for the S&P 500, the range is 41 points or -2.71% downside to 1183 and 0.66% upside to 1224.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: +53 (+1586)

- VOLUME: NYSE 1813.53 (+88%)

- VIX: 30.98 -3.1% YTD PERFORMANCE: +74.54%

- SPX PUT/CALL RATIO: 1.87 from 1.28 (+46.1%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 35.13

- 3-MONTH T-BILL YIELD: 0.01%

- 10-Year: 2.08 from 2.08

- YIELD CURVE: 1.90 from 1.88

MACRO DATA POINTS (Bloomberg Estimates):

- IMF/World Bank annual meetings this week

- FOMC begins two-day meeting tomorrow

- 10 a.m.: NAHB Housing Market, est. 15, prior 15

- 11:30 a.m.: U.S. to sell $29b 3-mo., $27b 6-mo. bills

WHAT TO WATCH:

- EU, IMF inspectors to hold call today with Greek Finance Minister to judge whether Greece is eligible for next aid payment due next month

- Greek PM George Papandreou canceled U.S. visit that was to begin today

- AT&T said to approach smaller rivals including MetroPCS, Leap Wireless to sell spectrum, subscribers in bid to save $39b takeover of T-Mobile USA

- Conagra has said it will withdraw Ralcorp takeover offer unless talks start by today; Ralcorp said not willing to begin them

- President Obama said to call for $1.5t in tax increases mostly targeting the wealthy over the next decade as part of a plan to cut the U.S federal deficit by $3t

- GM, UAW reach tentative agreement on 4-yr contract, including $5k bonus for workers; Ford, Chrysler next

- UTX said to be exploring possible bid for Goodrich

- Boeing postponed next week’s inaugural delivery of the 747-8 freighter after Cargolux Airlines declined to accept the planes

- Facebook said to unveil a media platform that will allow people to easily share their favorite music, television shows and movies, NYT says

- EIA releasing world energy supply and demand projection through 2035

- Netflix plans to separate its DVD-by-mail service from movie streaming, rename it Quikster

- UBS said Oswald Gruebel will remain as CEO, boosted estimate of trading loss to $2.3b

- Siemens drops plan to cooperate with Russia’s Rosatom in field of reactors

- "Lion King 3D’’ tops N. Amer. box office; “Modern Family” wins 5 Emmys

- Google Wallet may be introduced today, TechCrunch says

- No IPOs expected to price today

COMMODITY/GROWTH EXPECTATION

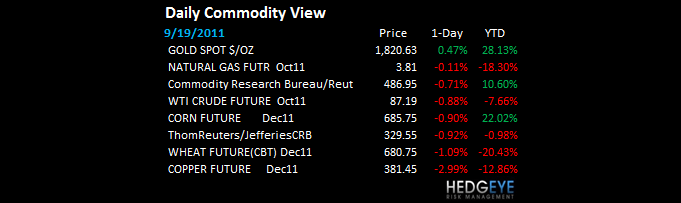

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- Copper Falls to Nine-Month Low in London on Europe Debts, China

- Hedge Fund Boxer Hall Says Gold to Extend Gains: Commodities

- Crude Drops to One-Week Low on Signals Oil-Demand Growth Slowing

- Commodities Fall as Copper Touches Nine-Month Low; Gold Gains

- Wheat Drops to Lowest Price Since July as Rain Falls in Texas

- Gold May Gain in New York as European Debt Concerns Boost Demand

- Freeport Indonesia Resumes Mining as Grasberg Workers Return

- Hedge Funds Raise Oil Wagers Most Since March: Energy Markets

- LNG Surges as Japan Vies With China, Exxon’s Shipments Grow

- Zinc May Fall After Failing to Top Average: Technical Analysis

- Funds Cut Bullish Commodity Wagers on ‘Contraction’ Concern

- Wheat Exports From India May Be Capped 500,000 Tons, Group Says

- Corn, Soybeans May Fall on Higher U.S. Yields, Economic Woes

- Teck’s Lindsay Favors Coal Mine Expansion as Industry M&A Booms

- Coffee Falls as European Stockpiles Are High; White Sugar Slides

- Shipper Navios Outperforms Parent on Soy Trade: Argentina Credit

- World Corn Growers Top U.S. Farms on Exports: Chart of the Day

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

Howard Penney

Managing Director