This note was originally published at 8am on September 13, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“To be great is to be misunderstood.”

-Ralph Waldo Emerson

Great short sellers in this game have one thing in common – they know when to cover.

I was taught how to sell short by doing. That’s not to say I’m the greatest short seller since the Count of Monte Cristo either. That’s simply to say that since 1999 I have had a lot of reps.

Like in any other profession, the more you do of something the more you have an opportunity to make mistakes. It’s your mistakes that make you evolve as a Risk Manager – that’s if you choose to let them teach you.

There have been plenty of opportunities for people in this game to evolve since 2008. Evidently, some have chosen not to. According to S&P data, only 167 of over 19,000 “recommendations” by Old Wall Street’s analysts this year have been “sell.” Professionally embarrassing.

We don’t want to embarrass the competition inasmuch as we want to challenge them. We wake up early every morning with fire in our bellies and a passion to be the change we want to see in this business.

Obviously on Washington’s Wall Street there hasn’t been a lot of that going on for the last 9 months – that’s why we do what we do. We want America to start winning again. Every losing streak ends with a win. It’s time to embrace winners.

Back to Short Covering…

I’ve written 2 intraday notes in Q3 of 2011 titled “Short Covering Opportunity” (one on August 8th and one yesterday). Yesterday’s call to cover shorts generated as much questioning and feedback as any time I think I have ever made a call to cover shorts since the thralls of early 2009. This is an important sentiment indicator.

Sentiment is one of the hardest things in this game to quantify. I was on multiple client calls yesterday where, ultimately, what very astute investors wanted to know was what I was “hearing” from other clients. My answer to that question is that there is no answer that is of quantifiable relevance. What any of us are “feeling” or “hearing” about markets subjects our performance to Great Misunderstandings.

As I wrote in yesterday’s Early Look, stock market fund “outflows” and “sentiment” will be the final stage for the 2011 Equities bears to navigate. What I meant by that is those who have been too bullish in 2011 will have redemptions (outflows) and forced to sell at immediate-term bottoms. All the while, quantifiable sentiment indicators will show signals of immediate-term TRADE capitulation.

Here are 3 of those:

- II Sentiment Survey Spread (Bulls Minus Bears) = dropped to almost a dead heat in the last week (39% Bulls, 38% Bears) and could easily move to the bearish side (more institutional investors admitting they are bearish at the bottom than bullish – it’s called career risk management into year-end) this week and next.

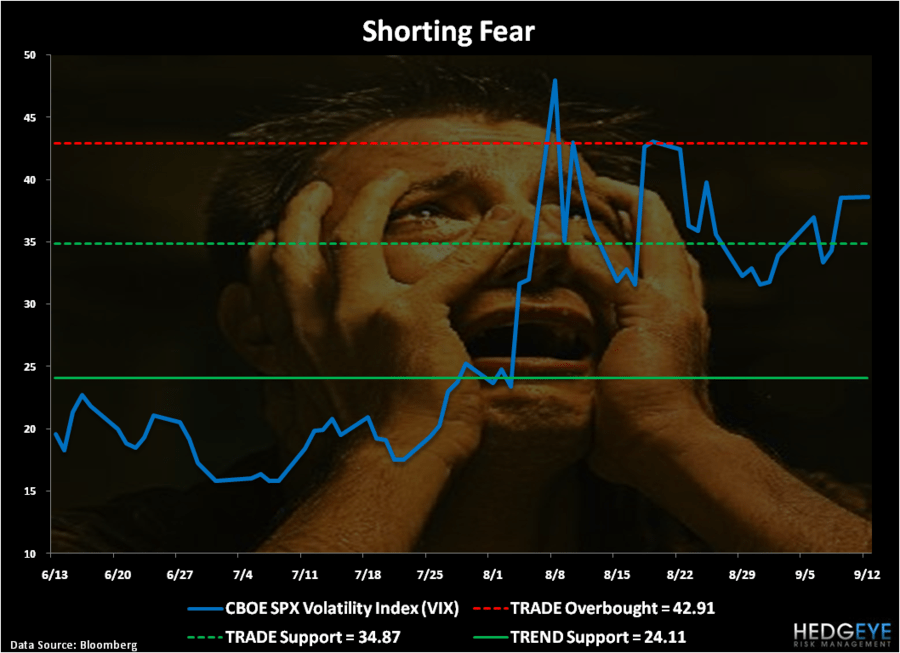

- Volatility (VIX) = immediate-term TRADE overbought yesterday at 43 and is now making a lower-high versus the August 8th Short Covering Opportunity high of VIX 48. Unless you think 2008 starts happening this week (it could!), lower-highs are what they are (bearish on the margin for volatility) and I shorted fear yesterday via a short position in the VXX.

- US Stocks vs US Treasury Bonds = flagged one of their widest performance chasing divergences of the year yesterday (stocks down, bonds up) and, critically, both the UST 10-year yield hit my immediate-term downside target of 1.87% intraday at the same time that the US stock market (SP500) tested lower-lows (then stocks recovered to close at a significantly higher-low).

“Significant” is as significant does. If you are using the wrong models and/or sources to help you navigate this beast of Keynesian Economics gone bad, we’d agree that most bulge bracket sell-side desks aren’t going to be helpful at this stage of the game (unless they are making calls to fade their economist/strategist calls as they “cut estimates” at the bottom).

Remember, bottoms are processes, not points. So you need a rigorous and repeatable Global Macro risk management model that has worked in both 2008 and 2011 to know when to cover. Making the turns “off the lows” matters.

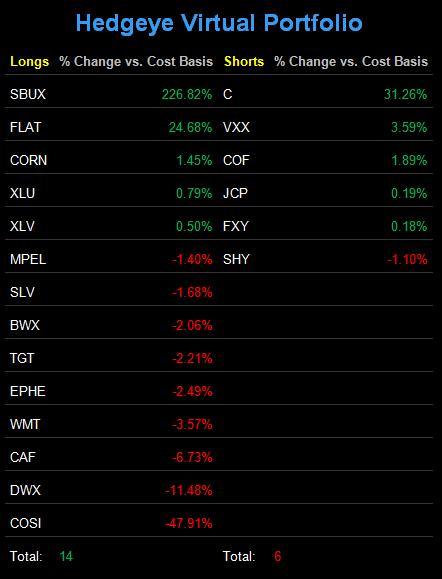

Lastly, after you take advantage of Short Covering Opportunities, you need to quickly, but patiently, get yourself back into position on defense. There are no rules against re-shorting things that you covered lower. Neither are there any Keynesian laws (yet) that prevent you from thinking quickly as you patiently pick your spots.

In Steven Pressfield’s “Gates Of Fire – An Epic Novel of The Battle of Thermopylae” (I read it on the beach last week to get me fired up for Q4’s Global Macro battle), Pressfield explains the “role of an officer” in Spartan war as follows:

“He was just a man doing his job. A job whose primary attribute was self-restraint and self-composure, not for his own sake, but for those whom he led by his example.” (“Gates Of Fire, page 112)

To be great in this globally interconnected game takes passion, patience, and time. The greatest of misunderstandings is how quickly we need to evolve the risk management process before it becomes our Waterloo.

My immediate-term support and resistance ranges for Gold, Oil, Germany’s DAX, and the SP500 are now $1801-1849, $86.03-90.51, 4890-5314, and 1141-1174, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer