TODAY’S S&P 500 SET-UP - September 15, 2011

As we look at today’s set up for the S&P 500, the range is 38 points or -1.40% downside to 1172 and 1.79% upside to 1210.

SECTOR AND GLOBAL PERFORMANCE

A 3 day rally finally gives us a bullish immediate-term TRADE signal for both the SP500 and 7 of 9 S&P Sectors. It’s been a long drought, but all droughts end with a fresh squeeze of water. The SP500’s TRADE line of support is now 1172. We have been getting longer because of a heightening probability of establishing higher-YTD-lows for the SP500 and that’s still what the model is signaling (if 1172 were to break, I still have significant support at 1141 vs the YTD closing low of 1119).

The 2 of 9 Sectors that remain bearish on our immediate-term TRADE duration are Financials (XLF) and Industrials (XLI) which are down -21% and -10.1% for the YTD, respectively. We are short Industrials (XLI) and long Utilities (XLU) which remains the top performing sector in the SP500 at +7.0% YTD.

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: +1430 (-139)

- VOLUME: NYSE 1085.46 (+1.37%)

- VIX: 34.60 -6.26% YTD PERFORMANCE: +94.93%

- SPX PUT/CALL RATIO: 1.49 from 1.71 -12.57%

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 34.91

- 3-MONTH T-BILL YIELD: 0.01%

- 10-Year: 2.03 from 2.00

- YIELD CURVE: 1.84 from 1.79

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30 a.m.: Consumer price index, est. 0.2%, prior 0.5%

- 8:30 a.m.: Empire manufacturing, est. (-4.00), prior (-7.72)

- 8:30 a.m.: Jobless claims, est. 411k, prior 414k

- 8:45 a.m.: Fed’s Bernanke gives brief remarks at risk conference (text, no questions)

- 9:15 a.m.: Industrial production, est. 0.0%, prior 0.9%

- 9:15 a.m.: Capacity utilization, est. 77.5%, prior 77.5%

- 9:45 a.m.: Bloomberg consumer comfort, est. (-49.0), prior (-49.3)

- 10 a.m.: Philadelphia Fed, est. (-15.0), prior (-30.7)

- 10 a.m.: Freddie Mac mortgage rates

- 1:45 p.m.: Fed’s Tarullo speaks at systemic risk conference

WHAT TO WATCH:

- UBS said it may post 3Q loss after $2b loss from unauthorized trading

- Groupon now said to be aiming for IPO as early as next month: NYT

- Texas Gov. Rick Perry is preferred presidential choice of 26% of Republicans, Republican-leaning independents: Bloomberg poll

- European stocks climbed for 3rd day as assurance from Germany and France that Greece will remain a member of the euro outweighed a $2b trading loss at UBS.

COMMODITY/GROWTH EXPECTATION

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- Gold-Backed Dollar Signals $10,000 Metal Price: Chart of the Day

- Goldman Sticks With Oil, Copper Forecasts as Risks Climb

- Oil Rises a Second Day in London on European Support for Greece

- Ralcorp Costing Investors $1 Billion Opposing ConAgra: Real M&A

- China to Install First Gold Vending Machine, ND Daily Says

- Copper Gains From One-Month Low on Easing Debt Concern, Strikes

- Freeport Weighs Grasberg Strike Impact on Output, Shipments

- SocGen Goes ‘Underweight’ on Commodities ‘in Danger Zone’

- Australia Wheat Exports Seen Trailing Government Forecast

- Rio Tinto to Invest Further $833 Million in Pilbara Expansion

- China’s Refined Copper Use May Reach 8.5 Million Tons in 2015

- Palm Oil Retreats as Global Cooking-Oil Supplies Set to Climb

- Libya to Resume Oil Exports Within Four Days, Official Says

- Record Texas Drought Burns Cotton Farmers as White Gold Withers

CURRENCIES

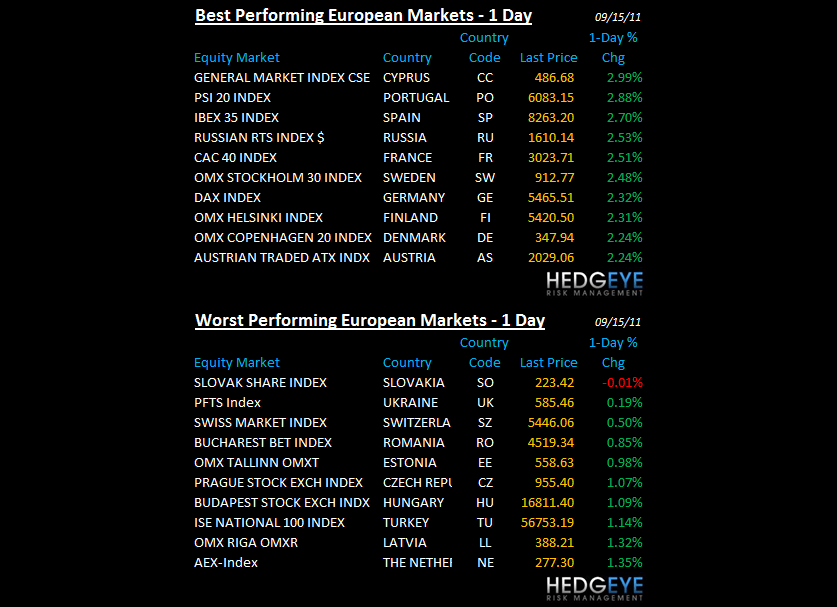

EUROPEAN MARKETS

- European stocks climbed for 3rd day as assurance from Germany and France that Greece will remain a member of the euro outweighed a $2b trading loss at UBS.

- EUROPE: Germany has sufficiently ripped the shorts a new one ... But the DAX trade line of resistance remains above last price at 5569

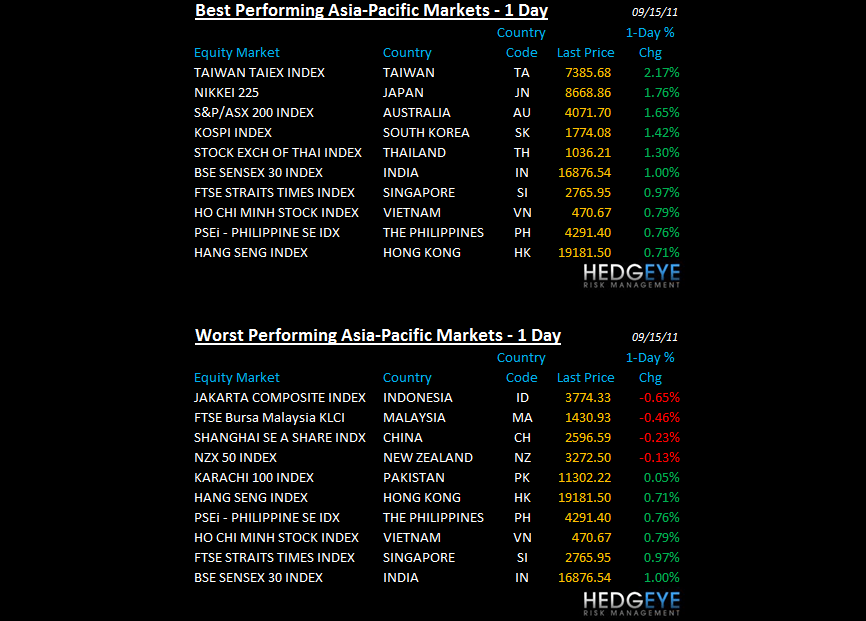

ASIAN MARKETS

- ASIA: much better morning for Asian equities than yesterday with both Japan and Korea coming off their lows

MIDDLE EAST

Howard Penney

Managing Director