The most recent supply and demand data points on corn do not augur well for consumer budgets going forward.

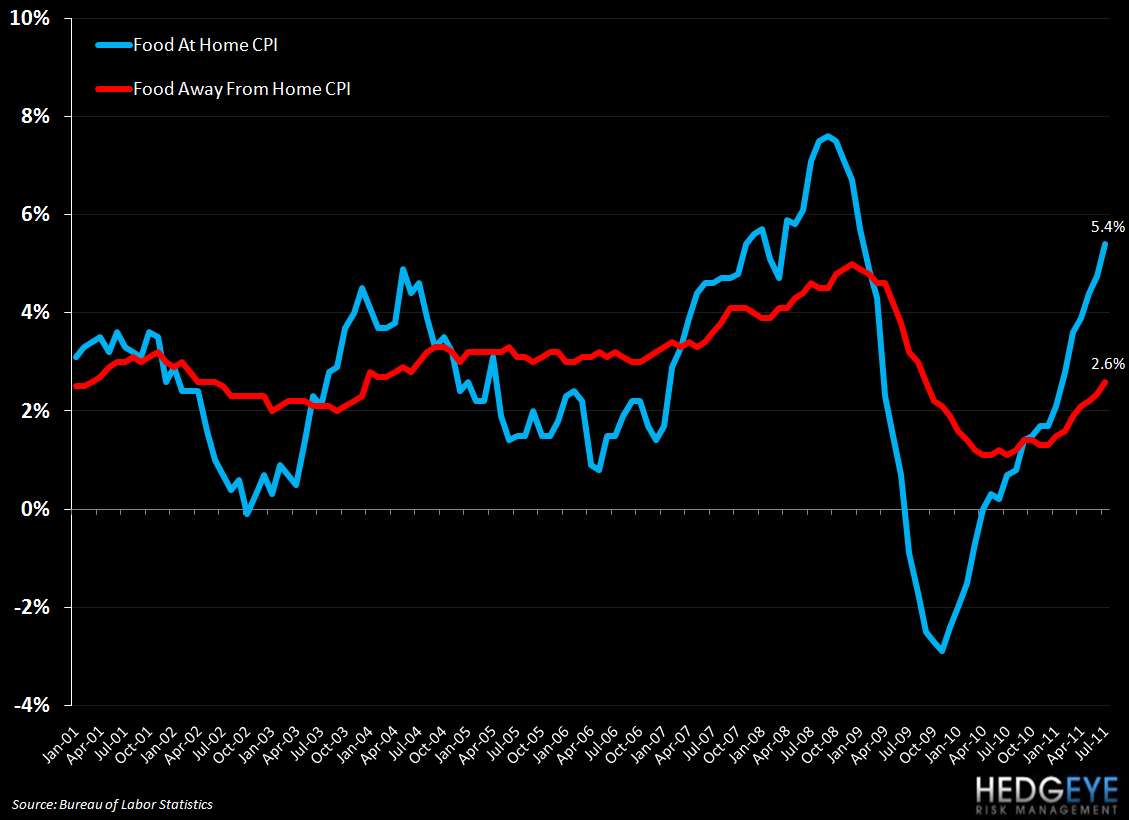

Inflation in the grocery aisle has been outstripping price increases at restaurants. This trend has been holding for some time and the most recent CPI data, for July, highlighted that. See the chart, below, that we are republishing from our 8/19/11 post, “CPI: GROCERY BILLS STILL OUT-INFLATING RESTAURANT CHECKS”. It will be interesting to learn whether or not the August data shows a continuation of this trend. August Consumer Price Index data is due to be released by the Bureau of Labor Statistics later this morning.

A report published by the USDA (link here) yesterday saw the official U.S. corn yield forecast for 2011/12 drop 4.9 bushels per acre this month to 148.1 bushels. The drop in U.S. production is expected to lead the U.S. to produce less than 50% of world corn trade for the first time in 30 years. Increased foreign coarse grain production will partly offset the U.S. drop but, overall, the price prospects for corn are higher following this report. The net 2011/12 market year ending stocks of corn are expected to dwindle to 672 million bushels versus 920 million at the end of 2010/11 and 1,708 million at the end of 2009/10.

This is supportive of continued high protein prices for consumers. Government forecasts now call for 3.5% to 4.5% grocery food inflation for 2011 which would be among the four largest annual increases over the past two decades.

Howard Penney

Managing Director

Rory Green

Analyst